Linear regression with multiple features

![]()

![]()

![]()

![]()

![]()

![]()

How does it work?

![]()

![]()

When should you use gradient descent and when should you use feature scaling?

New version of linear regression with multiple features

- Multiple variables = multiple features

- In original version we had

- X = house size, use this to predict

- y = house price

- If in a new scheme we have more variables (such as number of bedrooms, number floors, age of the home)

- x1, x2, x3, x4 are the four features

- x1 - size (feet squared)

- x2 - Number of bedrooms

- x3 - Number of floors

- x4 - Age of home (years)

- y is the output variable (price)

- x1, x2, x3, x4 are the four features

- More notation

- n

- number of features (n = 4)

- m

- number of examples (i.e. number of rows in a table)

- xi

- vector of the input for an example (so a vector of the four parameters for the ith input example)

- i is an index into the training set

- So

- x is an n-dimensional feature vector

- x3 is, for example, the 3rd house, and contains the four features associated with that house

- xji

- The value of feature j in the ith training example

- So

- x23 is, for example, the number of bedrooms in the third house

- n

- Now we have multiple features

-

- What is the form of our hypothesis?

- Previously our hypothesis took the form;

- hθ(x) = θ0 + θ1x

- Here we have two parameters (theta 1 and theta 2) determined by our cost function

- One variable x

- hθ(x) = θ0 + θ1x

- Now we have multiple features

- hθ(x) = θ0 + θ1x1 + θ2x2 + θ3x3 + θ4x4

- For example

- hθ(x) = 80 + 0.1x1 + 0.01x2 + 3x3 - 2x4

- An example of a hypothesis which is trying to predict the price of a house

- Parameters are still determined through a cost function

- hθ(x) = 80 + 0.1x1 + 0.01x2 + 3x3 - 2x4

- For convenience of notation, x0 = 1

- For every example i you have an additional 0th feature for each example

- So now your feature vector is n + 1 dimensional feature vector indexed from 0

- This is a column vector called x

- Each example has a column vector associated with it

- So let's say we have a new example called "X"

- Parameters are also in a 0 indexed n+1 dimensional vector

- This is also a column vector called θ

- This vector is the same for each example

- Considering this, hypothesis can be written

- hθ(x) = θ0x0 + θ1x1 + θ2x2 + θ3x3 + θ4x4

- If we do

- hθ(x) =θT X

- θT is an [1 x n+1] matrix

- In other words, because θ is a column vector, the transposition operation transforms it into a row vector

- So before

- θ was a matrix [n + 1 x 1]

- Now

- θT is a matrix [1 x n+1]

- Which means the inner dimensions of θT and X match, so they can be multiplied together as

- [1 x n+1] * [n+1 x 1]

- = hθ(x)

- So, in other words, the transpose of our parameter vector * an input example X gives you a predicted hypothesis which is [1 x 1] dimensions (i.e. a single value)

- This x0 = 1 lets us write this like this

- hθ(x) =θT X

- This is an example of multivariate linear regression

Gradient descent for multiple variables

- Fitting parameters for the hypothesis with gradient descent

- Parameters are θ0 to θn

- Instead of thinking about this as n separate values, think about the parameters as a single vector (θ)

- Where θ is n+1 dimensional

- Our cost function is

- Similarly, instead of thinking of J as a function of the n+1 numbers, J() is just a function of the parameter vector

- J(θ)

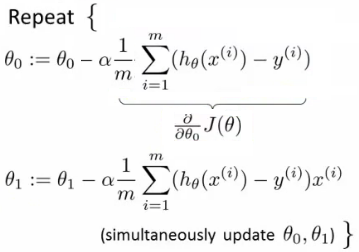

- Gradient descent

- Once again, this is

- θj = θj - learning rate (α) times the partial derivative of J(θ) with respect to θJ(...)

- We do this through a simultaneous update of every θj value

- Implementing this algorithm

- When n = 1

- Above, we have slightly different update rules for θ0 and θ1

- Actually they're the same, except the end has a previously undefined x0(i) as 1, so wasn't shown

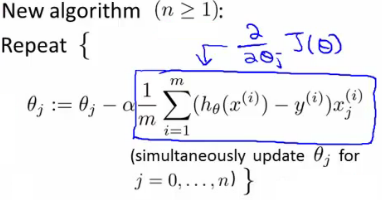

- We now have an almost identical rule for multivariate gradient descent

- What's going on here?

- We're doing this for each j (0 until n) as a simultaneous update (like when n = 1)

- So, we re-set θj to

- θj minus the learning rate (α) times the partial derivative of of the θ vector with respect to θj

- In non-calculus words, this means that we do

- Learning rate

- Times 1/m (makes the maths easier)

- Times the sum of

- The hypothesis taking in the variable vector, minus the actual value, times the j-th value in that variable vector for EACH example

- It's important to remember that

- These algorithm are highly similar

Gradient Decent in practice: 1 Feature Scaling

- Having covered the theory, we now move on to learn about some of the practical tricks

- Feature scaling

-

- If you have a problem with multiple features

- You should make sure those features have a similar scale

- Means gradient descent will converge more quickly

- e.g.

- x1 = size (0 - 2000 feet)

- x2 = number of bedrooms (1-5)

- Means the contours generated if we plot θ1 vs. θ2 give a very tall and thin shape due to the huge range difference

- Running gradient descent on this kind of cost function can take a long time to find the global minimum

- Pathological input to gradient descent

- So we need to rescale this input so it's more effective

- So, if you define each value from x1 and x2 by dividing by the max for each feature

- Contours become more like circles (as scaled between 0 and 1)

- May want to get everything into -1 to +1 range (approximately)

- Want to avoid large ranges, small ranges or very different ranges from one another

- Rule a thumb regarding acceptable ranges

- -3 to +3 is generally fine - any bigger bad

- -1/3 to +1/3 is ok - any smaller bad

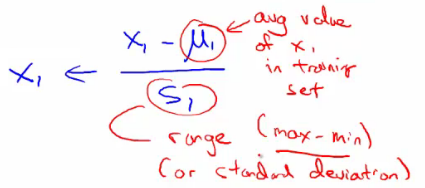

- Can do mean normalization

-

- Take a feature xi

-

- Replace it by (xi - mean)/max

- So your values all have an average of about 0

- Instead of max can also use standard deviation

Learning Rate α

- Focus on the learning rate (α)

- Topics

- Update rule

- Debugging

- How to chose α

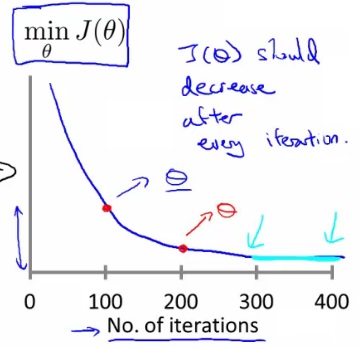

- Plot min J(θ) vs. no of iterations

- (i.e. plotting J(θ) over the course of gradient descent

- If gradient descent is working then J(θ) should decrease after every iteration

- Can also show if you're not making huge gains after a certain number

- Can apply heuristics to reduce number of iterations if need be

- If, for example, after 1000 iterations you reduce the parameters by nearly nothing you could chose to only run 1000 iterations in the future

- Make sure you don't accidentally hard-code thresholds like this in and then forget about why they're their though!

- Number of iterations varies a lot

- 30 iterations

- 3000 iterations

- 3000 000 iterations

- Very hard to tel in advance how many iterations will be needed

- Can often make a guess based a plot like this after the first 100 or so iterations

- Automatic convergence tests

- Check if J(θ) changes by a small threshold or less

- Choosing this threshold is hard

- So often easier to check for a straight line

- Why? - Because we're seeing the straightness in the context of the whole algorithm

- Could you design an automatic checker which calculates a threshold based on the systems preceding progress?

- Check if J(θ) changes by a small threshold or less

- Checking its working

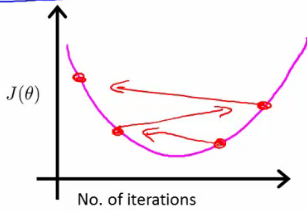

- If you plot J(θ) vs iterations and see the value is increasing - means you probably need a smaller α

- Cause is because your minimizing a function which looks like this

- If you plot J(θ) vs iterations and see the value is increasing - means you probably need a smaller α

- But you overshoot, so reduce learning rate so you actually reach the minimum (green line)

- So, use a smaller α

- Number of iterations varies a lot

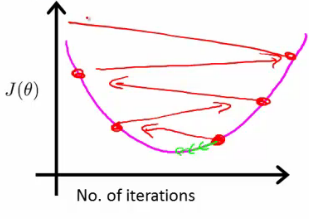

- Another problem might be if J(θ) looks like a series of waves

- Here again, you need a smaller α

- However

- If α is small enough, J(θ) will decrease on every iteration

- BUT, if α is too small then rate is too slow

- A less steep incline is indicative of a slow convergence, because we're decreasing by less on each iteration than a steeper slope

- Typically

-

- Try a range of alpha values

- Plot J(θ) vs number of iterations for each version of alpha

- Go for roughly threefold increases

-

- 0.001, 0.003, 0.01, 0.03. 0.1, 0.3

Features and polynomial regression

- Choice of features and how you can get different learning algorithms by choosing appropriate features

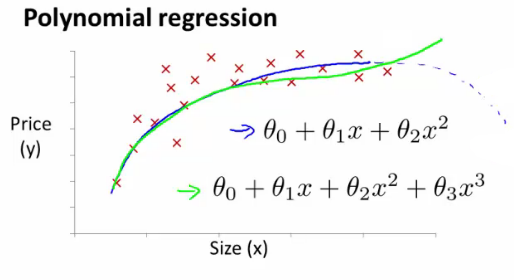

- Polynomial regression for non-linear function

- Example

- House price prediction

- Two features

- Frontage - width of the plot of land along road (x1)

- Depth - depth away from road (x2)

- Two features

- You don't have to use just two features

- Can create new features

- Might decide that an important feature is the land area

- So, create a new feature = frontage * depth (x3)

- h(x) = θ0 + θ1x3

- Area is a better indicator

- Often, by defining new features you may get a better model

- House price prediction

- Polynomial regression

-

- May fit the data better

- θ0 + θ1x + θ2x2 e.g. here we have a quadratic function

- For housing data could use a quadratic function

-

- But may not fit the data so well - inflection point means housing prices decrease when size gets really big

- So instead must use a cubic function

- How do we fit the model to this data

- To map our old linear hypothesis and cost functions to these polynomial descriptions the easy thing to do is set

- x1 = x

- x2 = x2

- x3 = x3

- By selecting the features like this and applying the linear regression algorithms you can do polynomial linear regression

- Remember, feature scaling becomes even more important here

- To map our old linear hypothesis and cost functions to these polynomial descriptions the easy thing to do is set

- Instead of a conventional polynomial you could do variable ^(1/something) - i.e. square root, cubed root etc

- Lots of features - later look at developing an algorithm to chose the best features

Normal equation

- For some linear regression problems the normal equation provides a better solution

- So far we've been using gradient descent

- Iterative algorithm which takes steps to converse

- Normal equation solves θ analytically

- Solve for the optimum value of theta

- Has some advantages and disadvantages

How does it work?

- Simplified cost function

- J(θ) = aθ2 + bθ + c

- θ is just a real number, not a vector

- Cost function is a quadratic function

- How do you minimize this?

- Do

- Take derivative of J(θ) with respect to θ

- Set that derivative equal to 0

- Allows you to solve for the value of θ which minimizes J(θ)

- Do

- J(θ) = aθ2 + bθ + c

- In our more complex problems;

-

- Here θ is an n+1 dimensional vector of real numbers

- Cost function is a function of the vector value

- How do we minimize this function

- Take the partial derivative of J(θ) with respect θj and set to 0 for every j

- Do that and solve for θ0 to θn

- This would give the values of θ which minimize J(θ)

- How do we minimize this function

- If you work through the calculus and the solution, the derivation is pretty complex

-

- Not going to go through here

- Instead, what do you need to know to implement this process

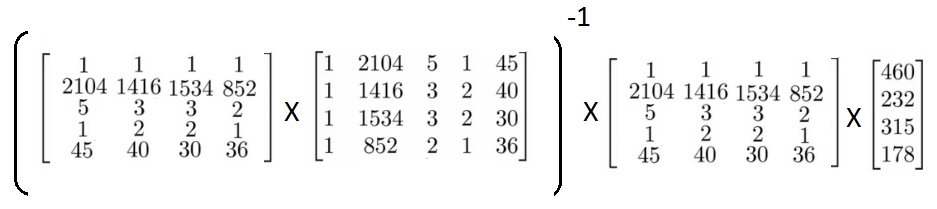

Example of normal equation

- Here

-

- m = 4

- n = 4

- To implement the normal equation

- Take examples

- Add an extra column (x0 feature)

- Construct a matrix (X - the design matrix) which contains all the training data features in an [m x n+1] matrix

- Do something similar for y

- Construct a column vector y vector [m x 1] matrix

- Using the following equation (X transpose * X) inverse times X transpose y

- If you compute this, you get the value of theta which minimize the cost function

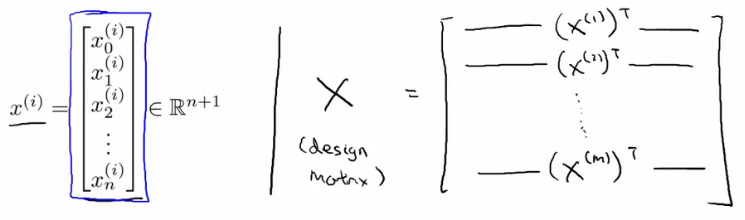

- Have m training examples and n features

-

- The design matrix (X)

-

- Each training example is a n+1 dimensional feature column vector

- X is constructed by taking each training example, determining its transpose (i.e. column -> row) and using it for a row in the design A

- This creates an [m x (n+1)] matrix

- Vector y

-

- Used by taking all the y values into a column vector

- What is this equation?!

-

- (XT * X)-1

-

- What is this --> the inverse of the matrix (XT * X)

- i.e. A = XT X

- A-1 = (XT X)-1

- What is this --> the inverse of the matrix (XT * X)

- In octave and MATLAB you could do;

pinv(X'*x)*x'*y

-

- X' is the notation for X transpose

- pinv is a function for the inverse of a matrix

-

- In a previous lecture discussed feature scaling

- If you're using the normal equation then no need for feature scaling

-

- Gradient descent

- Need to chose learning rate

- Needs many iterations - could make it slower

- Works well even when n is massive (millions)

- Better suited to big data

- What is a big n though

- 100 or even a 1000 is still (relativity) small

- If n is 10 000 then look at using gradient descent

- Normal equation

-

- No need to chose a learning rate

- No need to iterate, check for convergence etc.

- Normal equation needs to compute (XT X)-1

- This is the inverse of an n x n matrix

- With most implementations computing a matrix inverse grows by O(n3 )

- So not great

- Slow of n is large

-

- Can be much slower

- Gradient descent

Normal equation and non-invertibility

- Advanced concept

- Often asked about, but quite advanced, perhaps optional material

- Phenomenon worth understanding, but not probably necessary

- When computing (XT X)-1 * XT * y)

- What if (XT X) is non-invertible (singular/degenerate)

- Only some matrices are invertible

- This should be quite a rare problem

- Octave can invert matrices using

- pinv (pseudo inverse)

- This gets the right value even if (XT X) is non-invertible

- inv (inverse)

- pinv (pseudo inverse)

- Octave can invert matrices using

- What does it mean for (XT X) to be non-invertible

- Normally two common causes

- Redundant features in learning model

- e.g.

- x1 = size in feet

- x2 = size in meters squared

- e.g.

- Too many features

- e.g. m <= n (m is much larger than n)

- m = 10

- n = 100

- Trying to fit 101 parameters from 10 training examples

- Sometimes work, but not always a good idea

- Not enough data

- Later look at why this may be too little data

- To solve this we

- Delete features

- Use regularization (let's you use lots of features for a small training set)

- e.g. m <= n (m is much larger than n)

- Redundant features in learning model

- Normally two common causes

- If you find (XT X) to be non-invertible

- Look at features --> are features linearly dependent?

- So just delete one, will solve problem

- Look at features --> are features linearly dependent?

- What if (XT X) is non-invertible (singular/degenerate)

6912

6912

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言