ElasticNet 是一种使用L1和L2先验作为正则化矩阵的线性回归模型.这种组合用于只有很少的权重非零的稀疏模型,比如:class:Lasso, 但是又能保持:class:Ridge 的正则化属性.我们可以使用 l1_ratio 参数来调节L1和L2的凸组合(一类特殊的线性组合)。

当多个特征和另一个特征相关的时候弹性网络非常有用。Lasso 倾向于随机选择其中一个,而弹性网络更倾向于选择两个.

在实践中,Lasso 和 Ridge 之间权衡的一个优势是它允许在循环过程(Under rotate)中继承 Ridge 的稳定性.

弹性网络的目标函数是最小化:

minw12nsamples||Xw−y||22+αρ||w||1+α(1−ρ)2||w||22

ElasticNetCV 可以通过交叉验证来用来设置参数:

alpha (

α

),l1_ratio (

ρ

)

代码部分如下:

import numpy as np

from sklearn import linear_model

import warnings

warnings.filterwarnings('ignore')

###############################################################################

# Generate sample data

n_samples_train, n_samples_test, n_features = 75, 150, 500

np.random.seed(0)

coef = np.random.randn(n_features)

coef[50:] = 0.0 # only the top 10 features are impacting the model

X = np.random.randn(n_samples_train + n_samples_test, n_features)

y = np.dot(X, coef)

# Split train and test data

X_train, X_test = X[:n_samples_train], X[n_samples_train:]

y_train, y_test = y[:n_samples_train], y[n_samples_train:]

###############################################################################

# Compute train and test errors

alphas = np.logspace(-5, 1, 60)

enet = linear_model.ElasticNet(l1_ratio=0.7)

train_errors = list()

test_errors = list()

for alpha in alphas:

enet.set_params(alpha=alpha)

enet.fit(X_train, y_train)

train_errors.append(enet.score(X_train, y_train))

test_errors.append(enet.score(X_test, y_test))

i_alpha_optim = np.argmax(test_errors)

alpha_optim = alphas[i_alpha_optim]

print("Optimal regularization parameter : %s" % alpha_optim)

# Estimate the coef_ on full data with optimal regularization parameter

enet.set_params(alpha=alpha_optim)

coef_ = enet.fit(X, y).coef_

###############################################################################

# Plot results functions

import matplotlib.pyplot as plt

plt.subplot(2, 1, 1)

plt.semilogx(alphas, train_errors, label='Train')

plt.semilogx(alphas, test_errors, label='Test')

plt.vlines(alpha_optim, plt.ylim()[0], np.max(test_errors), color='k',

linewidth=3, label='Optimum on test')

plt.legend(loc='lower left')

plt.ylim([0, 1.2])

plt.xlabel('Regularization parameter')

plt.ylabel('Performance')

# Show estimated coef_ vs true coef

plt.subplot(2, 1, 2)

plt.plot(coef, label='True coef')

plt.plot(coef_, label='Estimated coef')

plt.legend()

plt.subplots_adjust(0.09, 0.04, 0.94, 0.94, 0.26, 0.26)

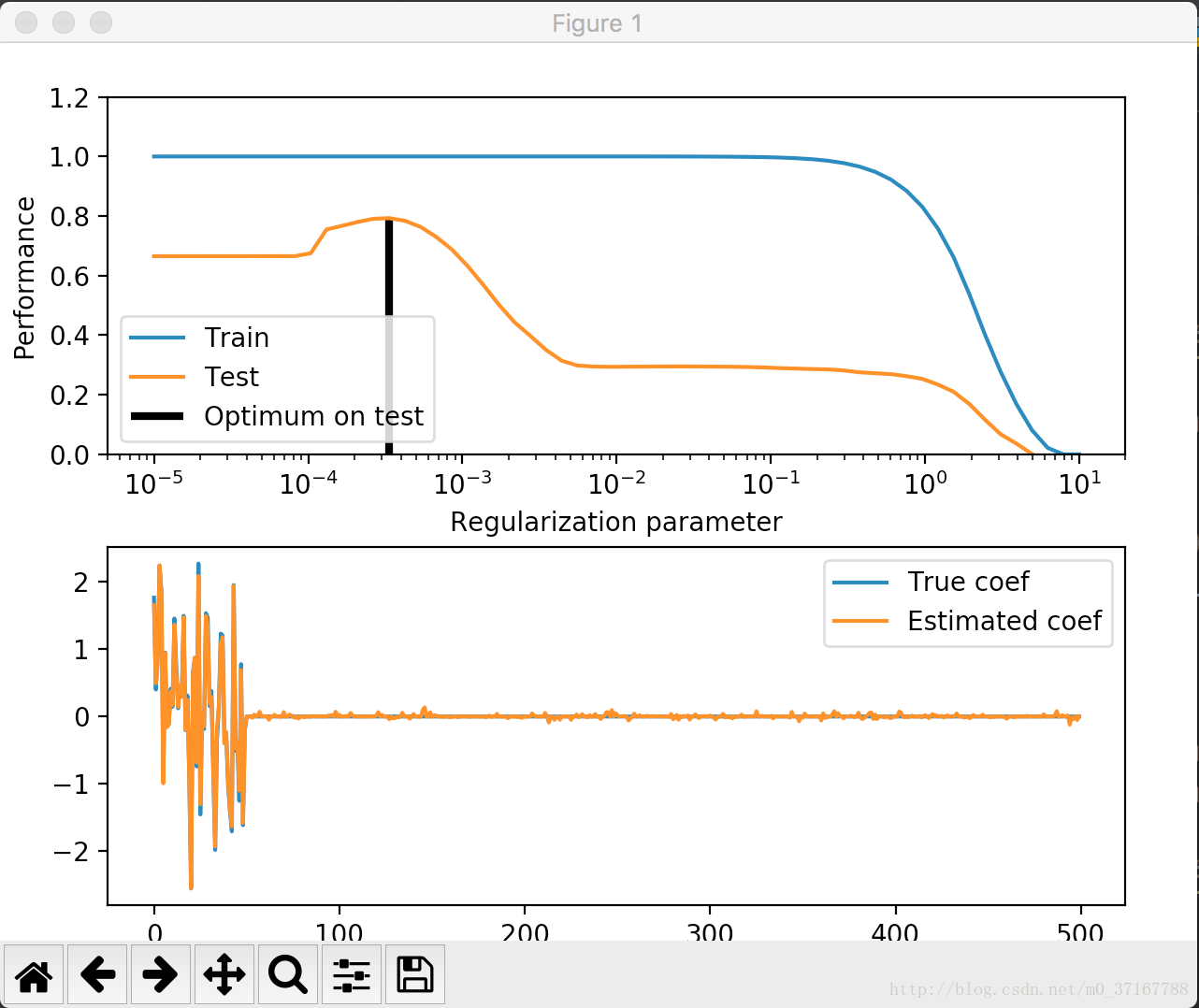

plt.show() 结果如下图所示:

控制台结果如下:

elastic net的大部分函数也会与之前的大体相似,所以这里仅仅介绍一些比较经常用的到的或者特殊的参数或函数:

参数:

l1_ratio:在0到1之间,代表在l1惩罚和l2惩罚之间,如果l1_ratio=1,则为lasso,是调节模型性能的一个重要指标。

eps:Length of the path. eps=1e-3 means that alpha_min / alpha_max = 1e-3

n_alphas:正则项alpha的个数

alphas:alpha值的列表

返回值:

alphas:返回模型中的alphas值。

coefs:返回模型系数。shape=(n_feature,n_alphas)

函数:

score(X,y,sample_weight):

评价模型性能的标准,值越接近1,模型效果越好。

798

798

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言