源码如下:

require(quantmod)

s <-

structure(

c(

1300, 1301.349976, 1281.199951, 1316.900024, 1312.310059, 1278,

1304.439941, 1304.709961, 1313.900024, 1323.089966, 1314.98999, 1301.719971,

1291.630005, 1271.01001, 1281.199951, 1311.040039, 1288.329956, 1273,

1301.189941, 1287.030029, 1307.890015, 1317.030029, 1288.959961, 1299.699951,

372300, 453800, 347600, 376400, 488200, 567300,

1301.189941, 1287.030029, 1307.890015, 1317.030029, 1288.959961, 1299.699951,

0.0034153392307692, 0.00258192266643587, 0.0255230051909361, 0.00470038870619693, 0.00204214772387123, 0.0185602276995305,

-0.00643845769230766, -0.0233142248891853, 0, -0.0044498328599013, -0.0182731991083518, -0.00391236306729259,

0.000915339230769252, -0.0110039169048249, 0.02083208321946, 9.87204781157658e-05, -0.0177931258240853, 0.016979617370892,

4, 3, 1, 4, 3, 1

),

.indexCLASS = "Date",

.indexTZ = "UTC",

tclass = "Date",

tzone = "UTC",

src = "yahoo",

updated =

structure

(

1459599733.74441,

class = c("POSIXct", "POSIXt")),

class = c("xts", "zoo"),

index =

structure

(

c(1458777600, 1459123200, 1459209600, 1459296000, 1459382400, 1459468800),

tzone = "UTC",

tclass = "Date"),

.Dim = c(6L, 10L),

.Dimnames = list(NULL, c("PCLN.Open", "PCLN.High", "PCLN.Low", "PCLN.Close", "PCLN.Volume", "PCLN.Adjusted", "h", "l", "c", "cluster")))

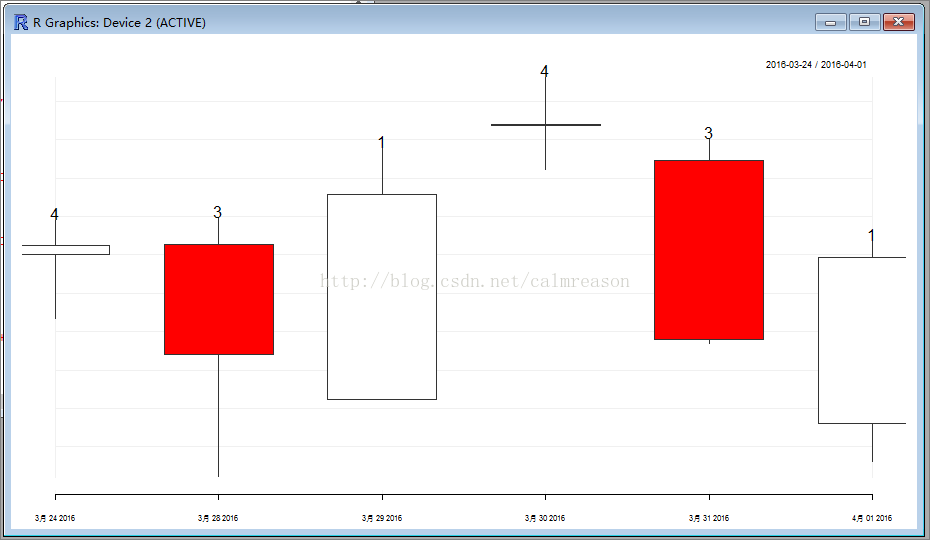

chart_Series(s)

text(x = s, y = s$cluster, label = as.character(s$cluster))

text(x = seq(nrow(s)), y = Hi(s)+1, label = as.character(s$cluster))

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言