移动平均,滤波,平滑等,这些概念其实都大同小异,其作用都是希望能把信号数值中的毛刺、噪点,给去掉抹平捋顺,留下真值。

这类的程序和工作做了不少,一直没有机会总结归纳整理下。趁着这次空挡的时间,写了一个算法调试工具,顺便写篇博客总结一下。

至于写了算法调试工具的目的,主要是为了提高效率。

我们一般调试算法的步骤是:

如果使用算法调试工具,那我们的流程就可以变成这样

按照之前的流程,可能要走很多遍,效率不高。

有了算法调试工具后,理想情况下,一次搞定。

当然这种效率的提高,也是因为前期工作的准备(算法调试工具的开发)。

目前市面上有很多类似的,且更好用的工具,不过自己还是想要结合自身所学,综合考虑,自己开发一个算法调试工具。如下,目前功能还不多,慢慢增加。

简单移动平均

原理

若依次得到一组原始测定值时,按顺序取一定数量的数据并算得其全部算术平均值,得到的数据就叫做移动平均值。

假设:

原始测定值为:

x

1

,

x

2

,

x

3

,

x

4...

,

x

n

x1,x2,x3,x4...,x_{n}

x1,x2,x3,x4...,xn

一定数量L 为:

3

3

3(移动平均的窗口长度)

则:

移动平均值:

x

1

+

x

2

+

x

3

3

,

x

2

+

x

3

+

x

4

3

,

x

3

+

x

4

+

x

5

3

,

x

4

+

x

5

+

x

6

3

.

.

.

.

.

.

\cfrac{x1+x2+x3}{3} , \cfrac{x2+x3+x4}{3},\cfrac{x3+x4+x5}{3},\cfrac{x4+x5+x6}{3}......

3x1+x2+x3,3x2+x3+x4,3x3+x4+x5,3x4+x5+x6......

代码(C#)

int len = (int)simpleLenUpDown.Value; //移动平均的窗口长度

simpleList.Clear();//移动平均值队列

List<double> bufferList = new List<double>();//移动平均窗口队列

for (int i = 0; i < len; i++)

{

if (i >= sourceList.Count)

break;

bufferList.Add(sourceList[i]);

simpleList.Add(sourceList[i]);

}

for (int i = len; i < sourceList.Count; i++)

{

simpleList.Add(bufferList.Average());

bufferList.RemoveAt(0);

bufferList.Add(sourceList[i]);//移动

}

//刷新结果

chartControl.BeginInit();

Series series = new Series(simpleStr, ViewType.Line);

series.Label.ResolveOverlappingMode = ResolveOverlappingMode.HideOverlapped;

for (int i = 0; i < simpleList.Count; i++)

{

SeriesPoint seriesPoint = new SeriesPoint(i, simpleList[i]);

series.Points.Add(seriesPoint);

}

chartControl.Series.Add(series);

series.ArgumentScaleType = ScaleType.Numerical;

chartControl.EndInit();

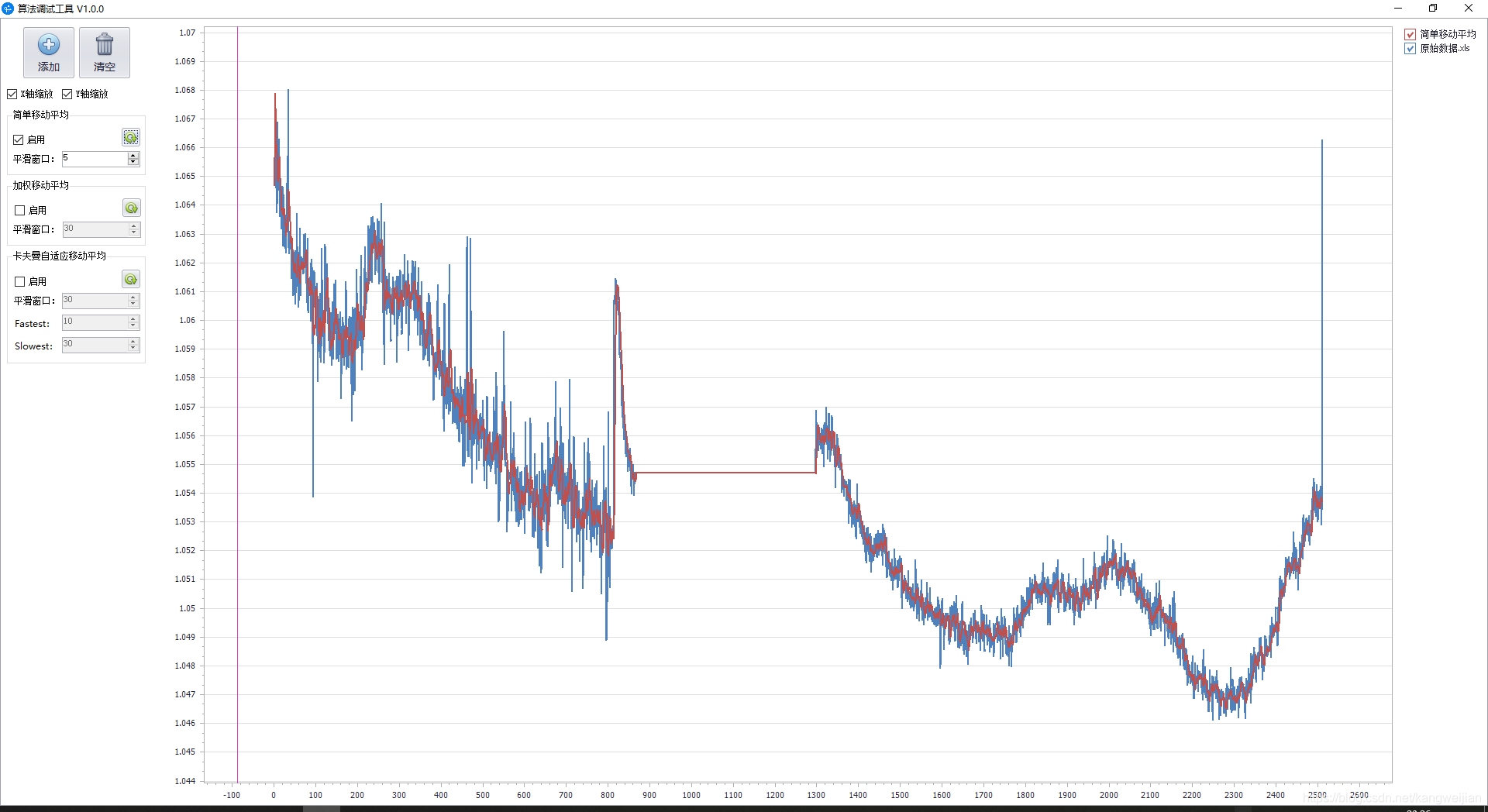

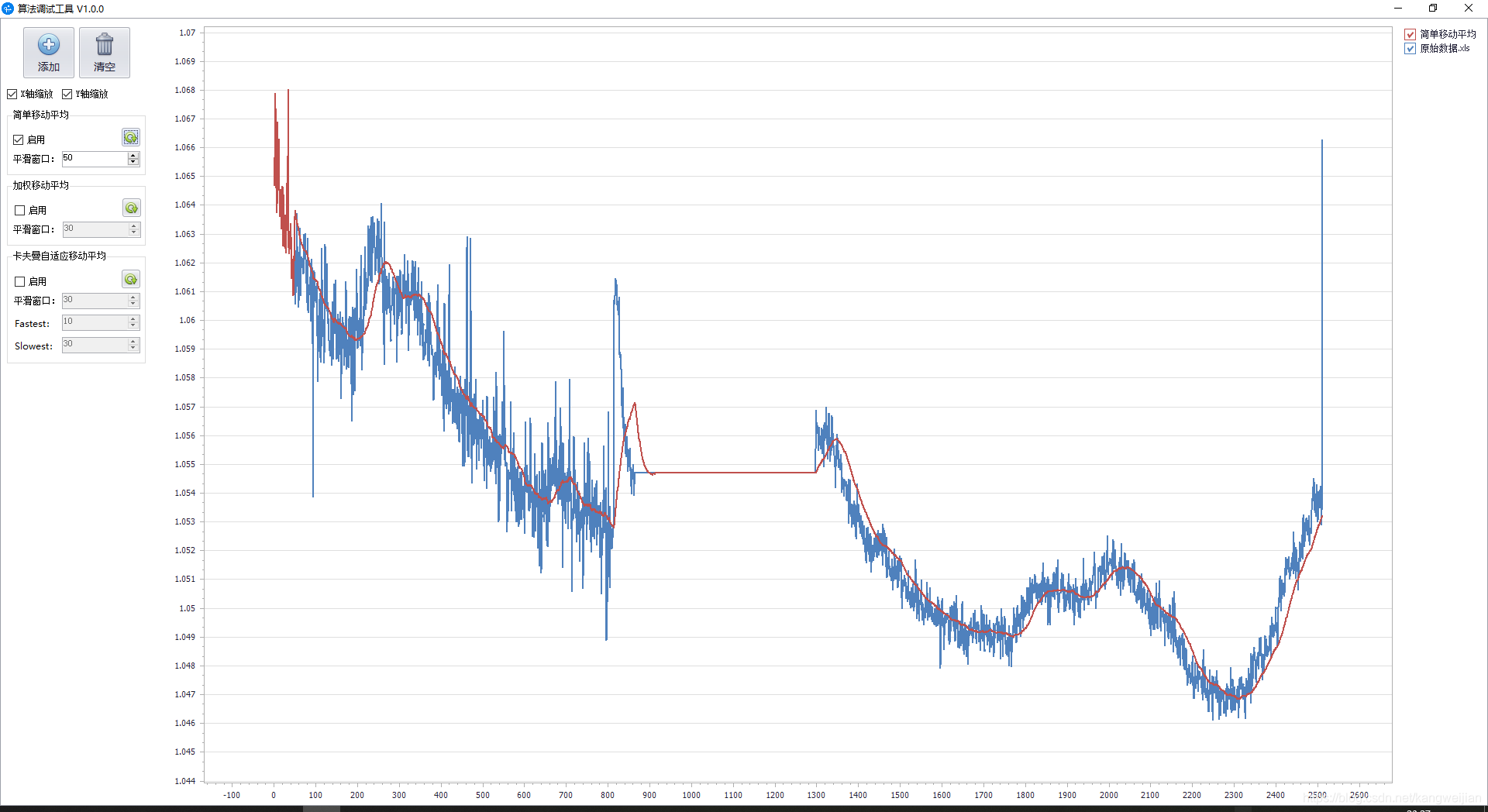

效果图

移动平均的窗口长度L=5

移动平均的窗口长度L=50

分析

两张效果图已经很明细了,窗口L如果太小,则平滑效果不好。

窗口L如果太大,则会有明显的迟滞效应。

所以这种简单移动平均的应用很有局限性,需要你小心的调整这个窗口L的大小。

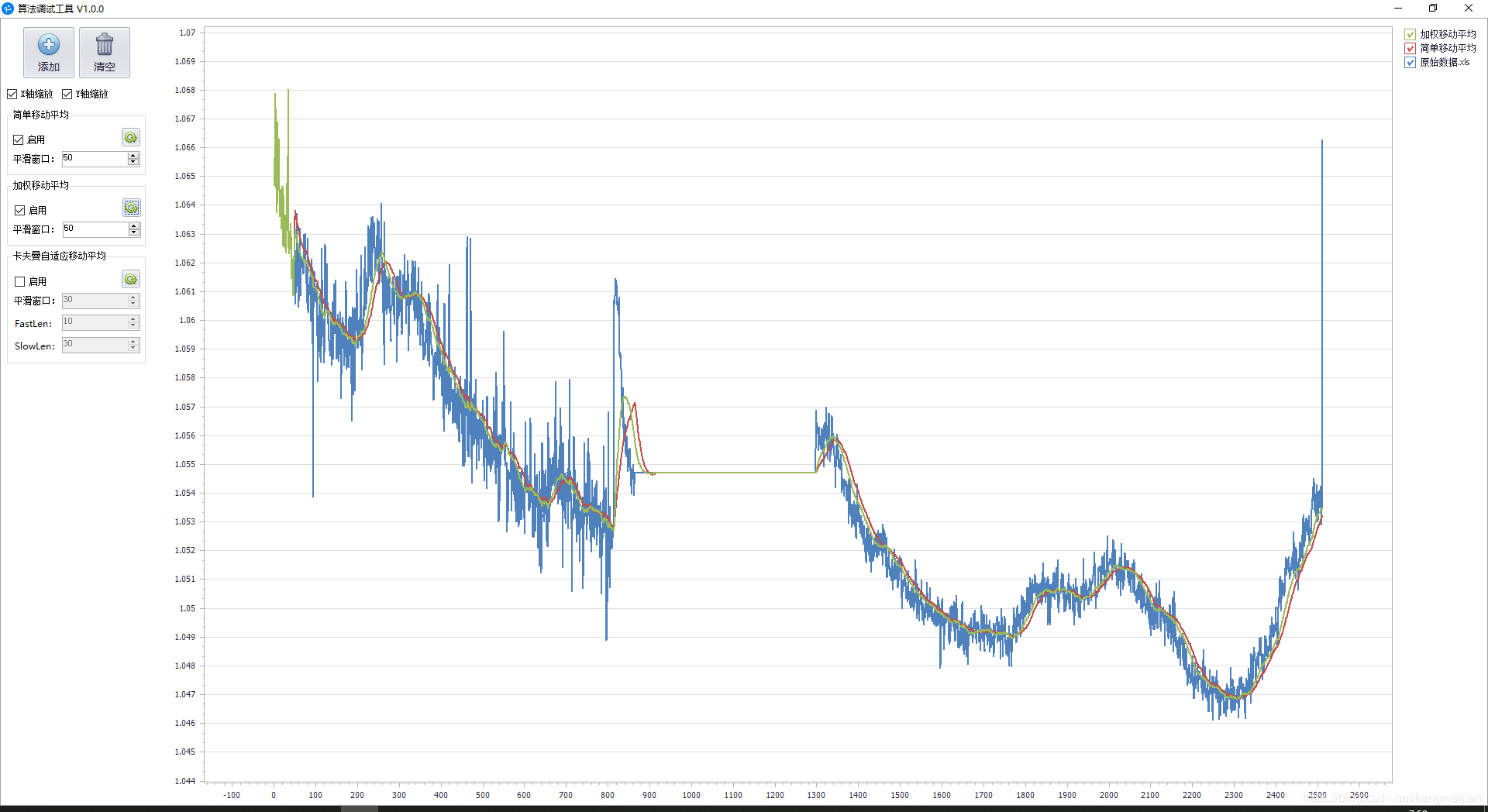

加权移动平均

原理

主要方法是,通过给较近的数值分配较高的权重,给较远的数值分配较低的权重。

主要目的是,在有不错的平滑效果情况下,尽量的减少其迟滞效应,更能反映当前的真值和未来的预测值。

权重分配的方法有很多,用的比较多的是线性法和指数法。以下以线性加权移动平均为例。

假设:

原始测定值为:

x

1

,

x

2

,

x

3

,

x

4...

,

x

n

x1,x2,x3,x4...,x_{n}

x1,x2,x3,x4...,xn

一定数量L 为:

3

3

3(移动平均的窗口长度)

则:

线性加权移动平均值:

1

×

x

1

+

2

×

x

2

+

3

×

x

3

3

,

1

×

x

2

+

2

×

x

3

+

3

×

x

4

3

,

1

×

x

3

+

2

×

x

4

+

3

×

x

5

3

,

1

×

x

4

+

2

×

x

5

+

3

×

x

6

3

.

.

.

.

.

.

\cfrac{1 \times x1+ 2 \times x2+3 \times x3}{3} , \cfrac{1 \times x2+2 \times x3+3 \times x4}{3},\cfrac{1 \times x3+2 \times x4+3 \times x5}{3},\cfrac{1 \times x4+2 \times x5+3 \times x6}{3}......

31×x1+2×x2+3×x3,31×x2+2×x3+3×x4,31×x3+2×x4+3×x5,31×x4+2×x5+3×x6......

代码(C#)

private double getWeightListAverage(List<double> bufferList)

{

double sum = 0;

int sumIndex = 0;

for (int i = 0; i < bufferList.Count; i++)

{

sumIndex += i;

sum += (i * bufferList[i]);

}

return sum / sumIndex;

}

private void weightUpdateBtn_Click(object sender, EventArgs e)

{

removeSeries(weightStr);

int len = (int)weightLenUpDown.Value;

weightList.Clear();

List<double> bufferList = new List<double>();

for (int i = 0; i < len; i++)

{

if (i >= sourceList.Count)

break;

bufferList.Add(sourceList[i]);

weightList.Add(sourceList[i]);

}

for (int i = len; i < sourceList.Count; i++)

{

weightList.Add(getWeightListAverage(bufferList));

bufferList.RemoveAt(0);

bufferList.Add(sourceList[i]);

}

chartControl.BeginInit();

Series series = new Series(weightStr, ViewType.Line);

series.Label.ResolveOverlappingMode = ResolveOverlappingMode.HideOverlapped;

for (int i = 0; i < weightList.Count; i++)

{

SeriesPoint seriesPoint = new SeriesPoint(i, weightList[i]);

series.Points.Add(seriesPoint);

}

chartControl.Series.Add(series);

series.ArgumentScaleType = ScaleType.Numerical;

chartControl.EndInit();

}

效果图

卡夫曼自适应移动平均

原理

卡夫曼自适应移动不同于以上两种的移动平均算法,它既能快速反应当前的真值和预测值,又能又较好的平滑效果。

原始测定值为:

x

1

,

x

2

,

x

3

,

x

4...

,

x

n

x1,x2,x3,x4...,x_{n}

x1,x2,x3,x4...,xn

窗口长度:

L

L

L

短(快)周期长度:

f

a

s

t

L

e

n

fastLen

fastLen

长(慢)周期长度:

s

l

o

w

L

e

n

slowLen

slowLen

波动性

v

o

l

=

∑

i

i

+

L

∣

x

i

−

x

i

+

1

∣

vol = \sum_{i}^{i+L} \left| x_i-x_{i+1} \right|

vol=∑ii+L∣xi−xi+1∣

方向性

d

i

r

e

c

t

i

o

n

=

∣

x

i

−

x

i

−

L

∣

direction= \left| x_i-x_{i-L} \right|

direction=∣xi−xi−L∣

效率系数

e

r

=

d

i

r

e

c

t

i

o

n

v

o

l

er = \cfrac{direction}{vol}

er=voldirection

短周期均线系数

f

a

s

t

e

s

t

=

2

f

a

s

t

L

e

n

+

1

fastest = \cfrac{2}{fastLen+1}

fastest=fastLen+12

长周期均线系数

s

l

o

w

e

s

t

=

2

s

l

o

w

L

e

n

+

1

slowest= \cfrac{2}{slowLen+1}

slowest=slowLen+12

平滑系数

s

m

o

o

t

h

=

e

r

×

(

f

a

s

t

e

s

t

−

s

l

o

w

e

s

t

)

+

s

l

o

w

e

s

t

smooth= er \times (fastest - slowest) + slowest

smooth=er×(fastest−slowest)+slowest

c

=

s

m

o

o

t

h

×

s

m

o

o

t

h

c=smooth \times smooth

c=smooth×smooth

公式

a

m

a

=

l

a

s

t

A

m

a

+

c

×

(

x

i

−

l

a

s

t

A

m

a

)

;

ama = lastAma + c \times (x_i - lastAma);

ama=lastAma+c×(xi−lastAma);

代码(C#)

int len = (int)amaLenUpDown.Value;

int fastLen = (int)amaFastLenUpDown.Value;

int slowLen = (int)amaSlowLenUpDown.Value;

amaList.Clear();

double ama=0, lastAma=0;

for (int i = 0; i < len; i++)

{

if (i >= sourceList.Count)

break;

lastAma = sourceList[i];

ama = lastAma;

amaList.Add(ama);

}

for (int i = len; i < sourceList.Count; i++)

{

double direction = 0, er = 0, smooth= 0, c = 0, vol = 0;

double fastest = 2.0 / (fastLen + 1);

double slowest = 2.0 / (slowLen + 1);

for (int j = i-len; j < i-1; j++)

vol += Math.Abs(sourceList[j] - sourceList[j + 1]);

if (vol != 0)

{

direction = Math.Abs(sourceList[i] - sourceList[i - len]);

er = direction / vol;

smooth1 = er * (fastest - slowest) + slowest;

c = smooth * smooth;

ama = lastAma + c * (sourceList[i] - lastAma);

if (c>1000)

{ //防止大跳跃,大突变

ama = sourceList[i];

}

lastAma = ama;

}

else

{

ama = lastAma;

}

amaList.Add(ama);

}

chartControl.BeginInit();

Series series = new Series(amaStr, ViewType.Line);

series.Label.ResolveOverlappingMode = ResolveOverlappingMode.HideOverlapped;

for (int i = 0; i < amaList.Count; i++)

{

SeriesPoint seriesPoint = new SeriesPoint(i, amaList[i]);

series.Points.Add(seriesPoint);

}

chartControl.Series.Add(series);

series.ArgumentScaleType = ScaleType.Numerical;

chartControl.EndInit();

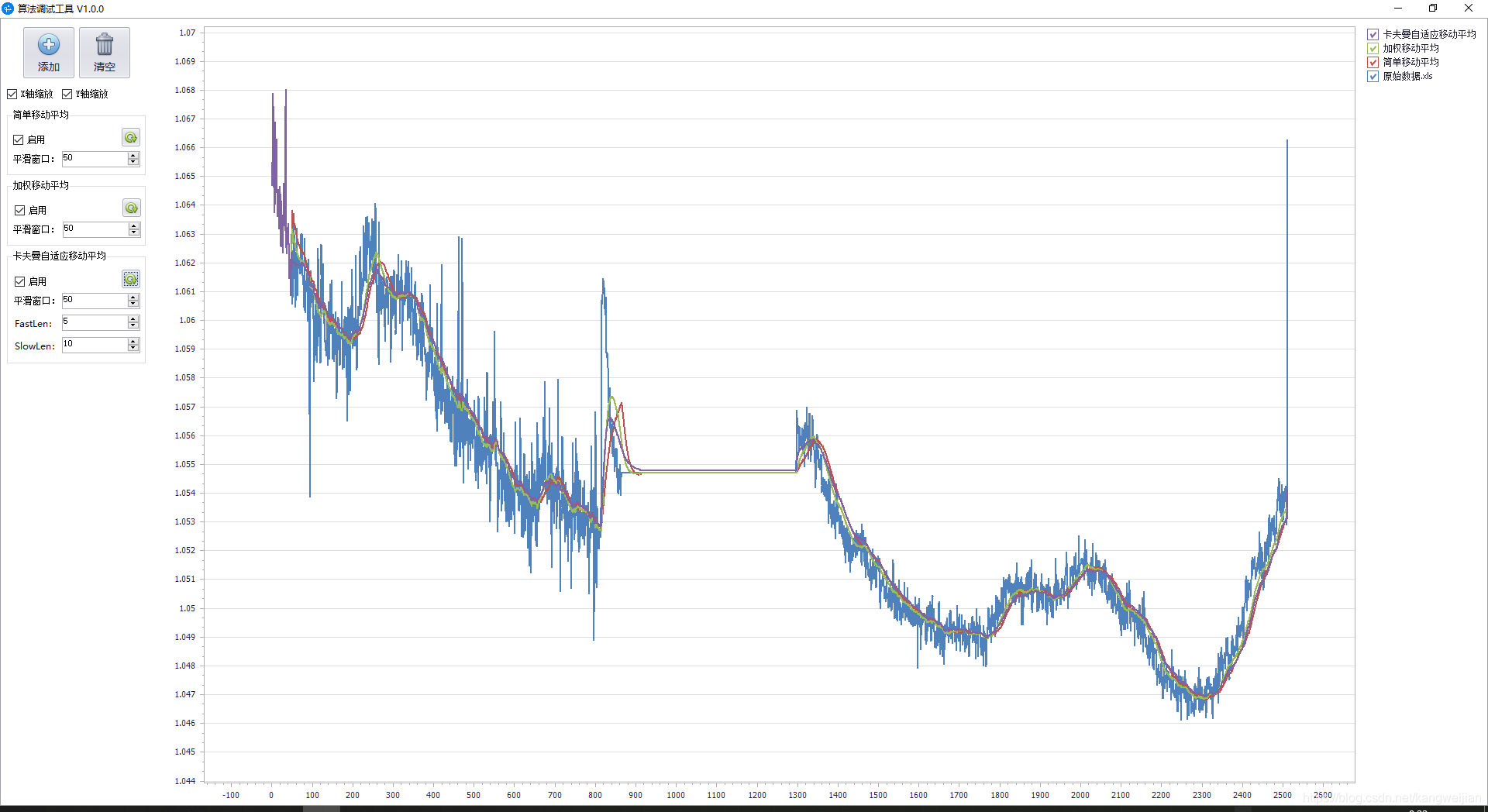

效果图

分析

不需要很大的窗口,就能有很好的平滑效果,且迟滞性很低。

这次分享到此结束,这类博客还有很多可以写的,后面希望能写出一个系列,分享更多更优更好的算法,迭代功能更强的算法调试工具。

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言