知识点:

1. 不平衡数据集的处理策略:过采样、修改权重、修改阈值

2. 交叉验证代码

作业:

从示例代码可以看到 效果没有变好,所以很多步骤都是理想是好的,但是现实并不一定可以变好。这个实验仍然有改进空间,如下。

1. 我还没做smote+过采样+修改权重的组合策略,有可能一起做会变好。

2. 我还没有调参,有可能调参后再取上述策略可能会变好

针对上面这2个探索路径,继续尝试下去,看看是否符合猜测。

步骤一:数据预处理

# 先运行之前预处理好的代码

import pandas as pd

import pandas as pd #用于数据处理和分析,可处理表格数据。

import numpy as np #用于数值计算,提供了高效的数组操作。

import matplotlib.pyplot as plt #用于绘制各种类型的图表

import seaborn as sns #基于matplotlib的高级绘图库,能绘制更美观的统计图形。

import warnings

warnings.filterwarnings("ignore")

# 设置中文字体(解决中文显示问题)

plt.rcParams['font.sans-serif'] = ['SimHei'] # Windows系统常用黑体字体

plt.rcParams['axes.unicode_minus'] = False # 正常显示负号

data = pd.read_csv('data.csv') #读取数据

# 先筛选字符串变量

discrete_features = data.select_dtypes(include=['object']).columns.tolist()

# Home Ownership 标签编码

home_ownership_mapping = {

'Own Home': 1,

'Rent': 2,

'Have Mortgage': 3,

'Home Mortgage': 4

}

data['Home Ownership'] = data['Home Ownership'].map(home_ownership_mapping)

# Years in current job 标签编码

years_in_job_mapping = {

'< 1 year': 1,

'1 year': 2,

'2 years': 3,

'3 years': 4,

'4 years': 5,

'5 years': 6,

'6 years': 7,

'7 years': 8,

'8 years': 9,

'9 years': 10,

'10+ years': 11

}

data['Years in current job'] = data['Years in current job'].map(years_in_job_mapping)

# Purpose 独热编码,记得需要将bool类型转换为数值

data = pd.get_dummies(data, columns=['Purpose'])

data2 = pd.read_csv("data.csv") # 重新读取数据,用来做列名对比

list_final = [] # 新建一个空列表,用于存放独热编码后新增的特征名

for i in data.columns:

if i not in data2.columns:

list_final.append(i) # 这里打印出来的就是独热编码后的特征名

for i in list_final:

data[i] = data[i].astype(int) # 这里的i就是独热编码后的特征名

# Term 0 - 1 映射

term_mapping = {

'Short Term': 0,

'Long Term': 1

}

data['Term'] = data['Term'].map(term_mapping)

data.rename(columns={'Term': 'Long Term'}, inplace=True) # 重命名列

continuous_features = data.select_dtypes(include=['int64', 'float64']).columns.tolist() #把筛选出来的列名转换成列表

# 连续特征用中位数补全

for feature in continuous_features:

mode_value = data[feature].mode()[0] #获取该列的众数。

data[feature].fillna(mode_value, inplace=True) #用众数填充该列的缺失值,inplace=True表示直接在原数据上修改。

# 最开始也说了 很多调参函数自带交叉验证,甚至是必选的参数,你如果想要不交叉反而实现起来会麻烦很多

# 所以这里我们还是只划分一次数据集

from sklearn.model_selection import train_test_split

X = data.drop(['Credit Default'], axis=1) # 特征,axis=1表示按列删除

y = data['Credit Default'] # 标签

# 按照8:2划分训练集和测试集

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42) # 80%训练集,20%测试集

步骤二:基准模型作为参照

输入:

from sklearn.ensemble import RandomForestClassifier #随机森林分类器

from sklearn.metrics import accuracy_score, precision_score, recall_score, f1_score # 用于评估分类器性能的指标

from sklearn.metrics import classification_report, confusion_matrix #用于生成分类报告和混淆矩阵

import warnings #用于忽略警告信息

warnings.filterwarnings("ignore") # 忽略所有警告信息

# --- 1. 默认参数的随机森林 ---

# 评估基准模型,这里确实不需要验证集

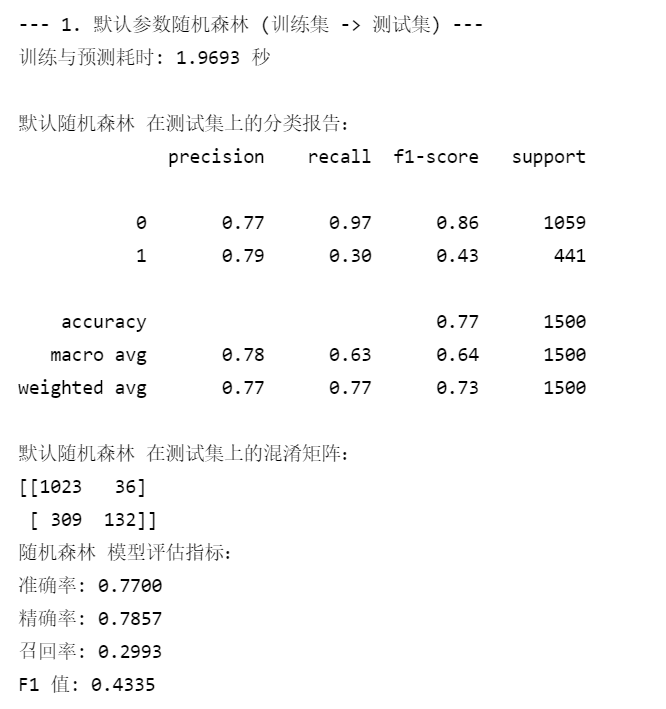

print("--- 1. 默认参数随机森林 (训练集 -> 测试集) ---")

import time # 这里介绍一个新的库,time库,主要用于时间相关的操作,因为调参需要很长时间,记录下会帮助后人知道大概的时长

start_time = time.time() # 记录开始时间

rf_model = RandomForestClassifier(random_state=42)

rf_model.fit(X_train, y_train) # 在训练集上训练

rf_pred = rf_model.predict(X_test) # 在测试集上预测

end_time = time.time() # 记录结束时间

print(f"训练与预测耗时: {end_time - start_time:.4f} 秒")

print("\n默认随机森林 在测试集上的分类报告:")

print(classification_report(y_test, rf_pred))

print("默认随机森林 在测试集上的混淆矩阵:")

print(confusion_matrix(y_test, rf_pred))

rf_accuracy = accuracy_score(y_test, rf_pred)

rf_precision = precision_score(y_test, rf_pred)

rf_recall = recall_score(y_test, rf_pred)

rf_f1 = f1_score(y_test, rf_pred)

print("随机森林 模型评估指标:")

print(f"准确率: {rf_accuracy:.4f}")

print(f"精确率: {rf_precision:.4f}")

print(f"召回率: {rf_recall:.4f}")

print(f"F1 值: {rf_f1:.4f}")输出:

步骤三:SMOTE过采样+权重调整的组合策略

输入:

# 1. SMOTE过采样+权重调整的组合策略

from imblearn.over_sampling import SMOTE

from imblearn.pipeline import Pipeline

from sklearn.model_selection import GridSearchCV

# 计算类别权重

minority_class = np.argmin(np.bincount(y_train))

majority_class = np.argmax(np.bincount(y_train))

scale_pos_weight = np.bincount(y_train)[majority_class] / np.bincount(y_train)[minority_class]

# 创建SMOTE和随机森林的pipeline

pipeline = Pipeline([

('smote', SMOTE(random_state=42)),

('rf', RandomForestClassifier(random_state=42, class_weight='balanced'))

])

# 训练模型

pipeline.fit(X_train, y_train)

# 2. 调参后再应用组合策略

# 定义参数网格

param_grid = {

'rf__n_estimators': [100, 200],

'rf__max_depth': [None, 10, 20],

'rf__min_samples_split': [2, 5],

'rf__min_samples_leaf': [1, 2]

}

# 使用F1分数作为评估指标(更适合不平衡数据)

scorer = make_scorer(f1_score, pos_label=minority_class)

# 创建网格搜索对象

grid_search = GridSearchCV(

estimator=pipeline,

param_grid=param_grid,

scoring=scorer,

cv=5,

n_jobs=-1

)

# 执行网格搜索

grid_search.fit(X_train, y_train)

# 输出最佳参数

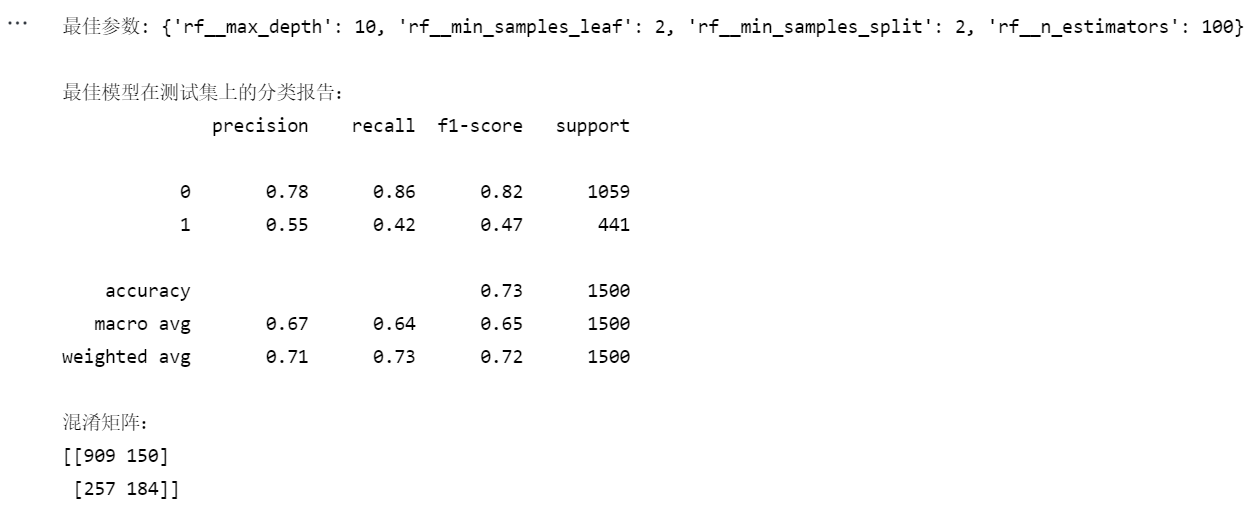

print("最佳参数:", grid_search.best_params_)

# 使用最佳参数训练最终模型

best_model = grid_search.best_estimator_

best_model.fit(X_train, y_train)

# 评估模型

y_pred = best_model.predict(X_test)

print("\n最佳模型在测试集上的分类报告:")

print(classification_report(y_test, y_pred))

print("混淆矩阵:")

print(confusion_matrix(y_test, y_pred))输出:

笔记

一、不平衡数据集处理策略

1. 过采样技术

1.1 随机过采样 (Random Oversampling)

from imblearn.over_sampling import RandomOverSampler

ros = RandomOverSampler(sampling_strategy='auto', random_state=42)

X_resampled, y_resampled = ros.fit_resample(X_train, y_train)

# 查看采样后分布

print("过采样后类别分布:", pd.Series(y_resampled).value_counts())特点:

-

简单复制少数类样本

-

可能导致过拟合

-

适合小规模数据集

1.2 SMOTE (Synthetic Minority Oversampling Technique)

from imblearn.over_sampling import SMOTE

smote = SMOTE(sampling_strategy=0.5, # 使少数类达到多数类的50%

k_neighbors=5,

random_state=42)

X_smote, y_smote = smote.fit_resample(X_train, y_train)特点:

-

通过插值生成新样本

-

比随机过采样更不易过拟合

-

参数

k_neighbors影响生成样本质量

1.3 ADASYN (Adaptive Synthetic Sampling)

from imblearn.over_sampling import ADASYN

adasyn = ADASYN(sampling_strategy='minority',

n_neighbors=5,

random_state=42)

X_adasyn, y_adasyn = adasyn.fit_resample(X_train, y_train)特点:

-

根据样本密度自适应生成样本

-

对难分类样本生成更多合成样本

-

计算成本高于SMOTE

2. 类别权重调整

2.1 自动计算类别权重

from sklearn.utils.class_weight import compute_class_weight

classes = np.unique(y_train)

weights = compute_class_weight('balanced', classes=classes, y=y_train)

class_weights = dict(zip(classes, weights))

# 在模型中使用

model = RandomForestClassifier(class_weight=class_weights, random_state=42)2.2 自定义权重

# 根据业务需求设置权重

custom_weights = {0: 1, 1: 3} # 少数类(1)的误分类代价是多数类(0)的3倍

model = RandomForestClassifier(class_weight=custom_weights, random_state=42)权重设置原则:

-

少数类样本的误分类代价越高,权重应越大

-

可通过网格搜索寻找最优权重比

3. 阈值调整 (Threshold Moving)

3.1 基于概率调整决策阈值

from sklearn.metrics import precision_recall_curve

# 获取预测概率

y_probs = model.predict_proba(X_test)[:, 1]

# 计算最佳阈值

precision, recall, thresholds = precision_recall_curve(y_test, y_probs)

f1_scores = 2 * (precision * recall) / (precision + recall)

optimal_threshold = thresholds[np.argmax(f1_scores)]

# 应用新阈值

y_pred_adj = (y_probs >= optimal_threshold).astype(int)3.2 代价敏感学习

from sklearn.metrics import make_scorer

from sklearn.metrics import confusion_matrix

def cost_sensitive_score(y_true, y_pred):

tn, fp, fn, tp = confusion_matrix(y_true, y_pred).ravel()

cost = fp * 1 + fn * 5 # 假设假阴性的代价是假阳性的5倍

return -cost # 返回负代价以便最大化

cost_scorer = make_scorer(cost_sensitive_score, greater_is_better=False)二、交叉验证实现

1. 基础交叉验证

1.1 K折交叉验证

from sklearn.model_selection import cross_val_score

from sklearn.metrics import make_scorer

from sklearn.metrics import f1_score

# 使用f1加权平均作为评估指标

f1_scorer = make_scorer(f1_score, average='weighted')

scores = cross_val_score(

estimator=model,

X=X_train,

y=y_train,

cv=5, # 5折交叉验证

scoring=f1_scorer,

n_jobs=-1

)

print("交叉验证F1分数:", scores)

print("平均F1分数: {:.3f} ± {:.3f}".format(scores.mean(), scores.std()))1.2 分层K折交叉验证

from imblearn.pipeline import make_pipeline

from sklearn.model_selection import StratifiedKFold

# 创建包含采样的流水线

pipeline = make_pipeline(

SMOTE(random_state=42),

RandomForestClassifier(random_state=42)

)

# 分层交叉验证

skf = StratifiedKFold(n_splits=5, shuffle=True, random_state=42)

scores = cross_val_score(pipeline, X_train, y_train, cv=skf, scoring=f1_scorer)适用场景:

-

分类问题

-

保持每折中类别比例与原数据一致

2. 不平衡数据的交叉验证

2.1 在交叉验证中应用采样

from imblearn.pipeline import make_pipeline

from sklearn.model_selection import StratifiedKFold

# 创建包含采样的流水线

pipeline = make_pipeline(

SMOTE(random_state=42),

RandomForestClassifier(random_state=42)

)

# 分层交叉验证

skf = StratifiedKFold(n_splits=5, shuffle=True, random_state=42)

scores = cross_val_score(pipeline, X_train, y_train, cv=skf, scoring=f1_scorer)注意事项:

-

采样只应在训练折叠上进行,验证折叠保持原始分布

-

使用

imblearn.pipeline确保采样步骤正确执行

2.2 重复交叉验证

from sklearn.model_selection import RepeatedStratifiedKFold

rskf = RepeatedStratifiedKFold(

n_splits=5,

n_repeats=3, # 重复3次

random_state=42

)

scores = cross_val_score(pipeline, X_train, y_train, cv=rskf, scoring=f1_scorer)优点:

-

更可靠的性能估计

-

减少因数据划分导致的方差

3. 时间序列交叉验证

from sklearn.model_selection import TimeSeriesSplit

tscv = TimeSeriesSplit(n_splits=5)

scores = cross_val_score(model, X_train, y_train, cv=tscv, scoring=f1_scorer)特点:

-

保持时间顺序

-

训练集总是早于测试集

-

适合时间相关数据

三、总结对比表

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言