1.背景

做量化交易的时候经常要用到股票的历史数据,例子中主要爬取每分钟'date','time''open','close','high','low','volume','money','avg'这几个字段数据,爬取之后存入数据库。

2.例子

```csharp

# 连接聚宽

from jqdatasdk import *

auth('注册账户','注册密码') # 账号是申请时所填写的手机号;密码为聚宽官网登录密码

# 连接数据库测试

import pymysql

# 打开数据库

db = pymysql.connect(host="localhost",user="root",password="1234",db="stock")

# 使用cursor()方法获取操作游标

cur = db.cursor()

# 根据get_price接口获取每分钟数据

# get_price没有日期字段,要通过获得索引的方式来获得日期(date)和时间(time)

df = get_price('002326.XSHE', start_date='2021-09-01 00:00:00', end_date='2022-02-28 00:00:00', frequency='1m', fields=['open','close','high','low','volume','money','avg'])

# 先在mysql建表,然后将数据插入数据库

j=0

for i in df.index:

print(df.index[j].strftime('%Y-%m-%d'))

print(df.index[j].strftime('%X'))

sql = """INSERT INTO data_002326(date,time,open,close,high,low,volume,money,avg)

VALUES ('%s','%s','%s', '%s', '%s', '%s', '%s', '%s', '%s')""" % (df.index[j].strftime('%Y-%m-%d'),df.index[j].strftime('%X'),df.loc[i,'open'],df.loc[i,'close'],df.loc[i,'high'],df.loc[i,'low'],df.loc[i,'volume'],df.loc[i,'money'],df.loc[i,'avg'])

j=j+1

try:

cur.execute(sql)

#提交

db.commit()

except Exception as e:

#错误回滚

db.rollback()

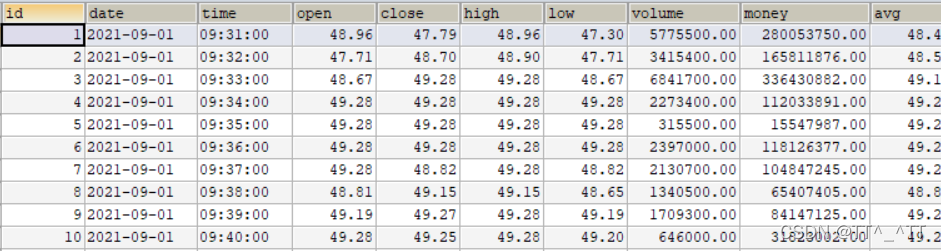

结果:

# mysql建表

CREATE TABLE IF NOT EXISTS `data_600030`(

`id` INT UNSIGNED AUTO_INCREMENT,

`date` VARCHAR(100),

`time` VARCHAR(100) ,

`open` DECIMAL(10,2) ,

`close` DECIMAL(10,2) ,

`high` DECIMAL(10,2) ,

`low` DECIMAL(10,2) ,

`volume` DECIMAL(15,2) ,

`money` DECIMAL(15,2),

`avg` DECIMAL(10,2),

PRIMARY KEY ( `id` )

)ENGINE=INNODB DEFAULT CHARSET=utf8;

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言