第11章 时间序列

时间序列数据主要有:时间戳、固定时间、时间间隔以及实验或过程时间。

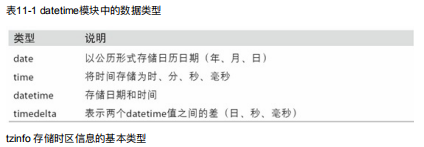

11.1 日期和时间数据类型及工具

一般使用datetime.datetime数据类型。

from datetime import datetime

now= datetime.now()

print(now)

print(now.year,now.month,now.day)

#datetime是用毫秒的方式存储时间的

2020-02-05 11:59:28.917677

2020 2 5

delta = datetime(2011, 1, 7) - datetime(2008, 6, 24, 8, 15)

print(delta.days)

print('\n')

print(delta.seconds)

print('\n')

print(delta)#delta是一个timedelta对象,表示两个datetime对象之间的时间差。

926

56700

926 days, 15:45:00

可以给datetime加上或减去一个或者多个timedelta。

from datetime import timedelta

start = datetime(2011, 1, 7)

start + timedelta(12)

start - 2 * timedelta(12)

datetime.datetime(2010, 12, 14, 0, 0)

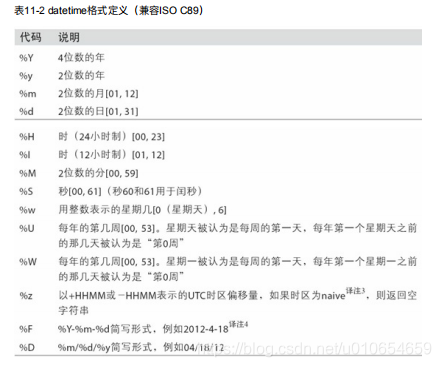

字符串和datetime的相互转换

利用str或strftime方法可以将datetime对象和pandas的timestamp对象转化挖诶字符串。

datetime的strftime方法可以对把上述格式的编码字符串转换为日期。

stamp = datetime(2011, 1, 3)

print(str(stamp))

print(stamp.strftime('%Y-%m-%d'))

2011-01-03 00:00:00

2011-01-03

value = '2011-01-03'

datetime.strptime(value, '%Y-%m-%d')

datestrs = ['7/6/2011', '8/6/2011']

print([datetime.strptime(x, '%m/%d/%Y') for x in datestrs])

[datetime.datetime(2011, 7, 6, 0, 0), datetime.datetime(2011, 8, 6, 0, 0)]

对于常用的日期格式,可以用dateutil这个第三方包中的parser.parse方法。

from dateutil.parser import parse

parse('2011-01-03')

parse('Jan 31, 1997 10:45 PM')

datetime.datetime(1997, 1, 31, 22, 45)

#日出现在月的前面很普遍,传入dayfirst=True即可解决这个问题:

parse('6/12/2011', dayfirst=True)

datetime.datetime(2011, 12, 6, 0, 0)

import pandas as pd

#to_datetime方法可以解析多种不同的日期表示形式

datestrs = ['2011-07-06 12:00:00', '2011-08-06 00:00:00']

pd.to_datetime(datestrs)

DatetimeIndex(['2011-07-06 12:00:00', '2011-08-06 00:00:00'], dtype='datetime64[ns]', freq=None)

特定于当前环境的日期格式。

11.2 时间序列基础

from datetime import datetime

import numpy as np

dates = [datetime(2011, 1, 2), datetime(2011, 1, 5),

datetime(2011, 1, 7), datetime(2011, 1, 8),

datetime(2011, 1, 10), datetime(2011, 1, 12)]

ts = pd.Series(np.random.randn(6), index=dates)

print(ts)

2011-01-02 -1.716667

2011-01-05 -1.539430

2011-01-07 -1.207904

2011-01-08 -2.273456

2011-01-10 0.205142

2011-01-12 0.316390

dtype: float64

ts.index

DatetimeIndex(['2011-01-02', '2011-01-05', '2011-01-07', '2011-01-08',

'2011-01-10', '2011-01-12'],

dtype='datetime64[ns]', freq=None)

ts + ts[::2]

2011-01-02 -3.433335

2011-01-05 NaN

2011-01-07 -2.415809

2011-01-08 NaN

2011-01-10 0.410284

2011-01-12 NaN

dtype: float64

ts.index.dtype

dtype('<M8[ns]')

stamp = ts.index[0]

stamp

Timestamp('2011-01-02 00:00:00')

索引、选取、子集构造

stamp = ts.index[2]

ts[stamp]

-1.2079043608040851

#还可以传入可以被解释成日期的字符串,通过这样的方式,也可以索引数据。

ts['1/10/2011']

0.2051420361141498

#对于长序列,只需要传入“年”或者“年月”即可轻松选取数据的切片。

longer_ts = pd.Series(np.random.randn(1000),

index=pd.date_range('1/1/2000', periods=1000))

print(longer_ts['2001'])#选择年

print('\n')

print(longer_ts['2001-05'])#选择年月

2001-01-01 0.338687

2001-01-02 -1.073274

2001-01-03 0.637883

2001-01-04 0.309464

2001-01-05 0.692688

...

2001-12-27 0.264949

2001-12-28 0.881644

2001-12-29 -2.017786

2001-12-30 0.003661

2001-12-31 -0.060487

Freq: D, Length: 365, dtype: float64

2001-05-01 0.936911

2001-05-02 1.060100

2001-05-03 0.044787

2001-05-04 -0.780111

2001-05-05 -2.865649

2001-05-06 -1.078818

2001-05-07 -1.159225

2001-05-08 -0.327021

2001-05-09 -0.410140

2001-05-10 -0.851768

2001-05-11 0.519780

2001-05-12 -0.236362

2001-05-13 2.319194

2001-05-14 -1.141007

2001-05-15 -0.348985

2001-05-16 -0.118603

2001-05-17 -0.049692

2001-05-18 -0.210484

2001-05-19 0.804600

2001-05-20 -0.697858

2001-05-21 -0.275231

2001-05-22 1.777904

2001-05-23 1.053514

2001-05-24 -2.172931

2001-05-25 0.509915

2001-05-26 0.926985

2001-05-27 1.499682

2001-05-28 0.007916

2001-05-29 1.339204

2001-05-30 1.239413

2001-05-31 -1.425689

Freq: D, dtype: float64

#datetime对象也可以切片.方式是通过将时间作为索引。

ts[datetime(2011, 1, 7):]

2011-01-07 -1.207904

2011-01-08 -2.273456

2011-01-10 0.205142

2011-01-12 0.316390

dtype: float64

ts['1/6/2011':'1/11/2011']

2011-01-07 -1.207904

2011-01-08 -2.273456

2011-01-10 0.205142

dtype: float64

带有重复索引的时间序列

dates = pd.DatetimeIndex(['1/1/2000', '1/2/2000', '1/2/2000',

'1/2/2000', '1/3/2000'])

dup_ts = pd.Series(np.arange(5), index=dates)

print(dup_ts)

2000-01-01 0

2000-01-02 1

2000-01-02 2

2000-01-02 3

2000-01-03 4

dtype: int32

#通过is_unique属性,可以判断时间序列数据的索引是不是唯一的

dup_ts.index.is_unique

False

#如果要对非唯一的时间戳的数据进行聚合,可以使用groupby,对level设置为0.

grouped = dup_ts.groupby(level=0)

print(grouped.mean())

print('\n')

print(grouped.count())

2000-01-01 0

2000-01-02 2

2000-01-03 4

dtype: int32

2000-01-01 1

2000-01-02 3

2000-01-03 1

dtype: int64

11.3 日期的范围、频率以及移动

可以将之前那个时间序列转换为1个具有固定频率(每天)的时间序列,只需调用resample即可。

ts

2011-01-02 -1.716667

2011-01-05 -1.539430

2011-01-07 -1.207904

2011-01-08 -2.273456

2011-01-10 0.205142

2011-01-12 0.316390

dtype: float64

resampler = ts.resample('D')#D为每天的意思

生成日期范围

date_range可以生成时间范围。

index = pd.date_range('2012-04-01', '2012-06-01')

print(index)

DatetimeIndex(['2012-04-01', '2012-04-02', '2012-04-03', '2012-04-04',

'2012-04-05', '2012-04-06', '2012-04-07', '2012-04-08',

'2012-04-09', '2012-04-10', '2012-04-11', '2012-04-12',

'2012-04-13', '2012-04-14', '2012-04-15', '2012-04-16',

'2012-04-17', '2012-04-18', '2012-04-19', '2012-04-20',

'2012-04-21', '2012-04-22', '2012-04-23', '2012-04-24',

'2012-04-25', '2012-04-26', '2012-04-27', '2012-04-28',

'2012-04-29', '2012-04-30', '2012-05-01', '2012-05-02',

'2012-05-03', '2012-05-04', '2012-05-05', '2012-05-06',

'2012-05-07', '2012-05-08', '2012-05-09', '2012-05-10',

'2012-05-11', '2012-05-12', '2012-05-13', '2012-05-14',

'2012-05-15', '2012-05-16', '2012-05-17', '2012-05-18',

'2012-05-19', '2012-05-20', '2012-05-21', '2012-05-22',

'2012-05-23', '2012-05-24', '2012-05-25', '2012-05-26',

'2012-05-27', '2012-05-28', '2012-05-29', '2012-05-30',

'2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')

#此外还可以传入时间结束或者开始点

print(pd.date_range(start='2012-04-01', periods=20))

print('\n')

print(pd.date_range(end='2012-06-01', periods=20))

DatetimeIndex(['2012-04-01', '2012-04-02', '2012-04-03', '2012-04-04',

'2012-04-05', '2012-04-06', '2012-04-07', '2012-04-08',

'2012-04-09', '2012-04-10', '2012-04-11', '2012-04-12',

'2012-04-13', '2012-04-14', '2012-04-15', '2012-04-16',

'2012-04-17', '2012-04-18', '2012-04-19', '2012-04-20'],

dtype='datetime64[ns]', freq='D')

DatetimeIndex(['2012-05-13', '2012-05-14', '2012-05-15', '2012-05-16',

'2012-05-17', '2012-05-18', '2012-05-19', '2012-05-20',

'2012-05-21', '2012-05-22', '2012-05-23', '2012-05-24',

'2012-05-25', '2012-05-26', '2012-05-27', '2012-05-28',

'2012-05-29', '2012-05-30', '2012-05-31', '2012-06-01'],

dtype='datetime64[ns]', freq='D')

按着时间频率进行时间序列的排列

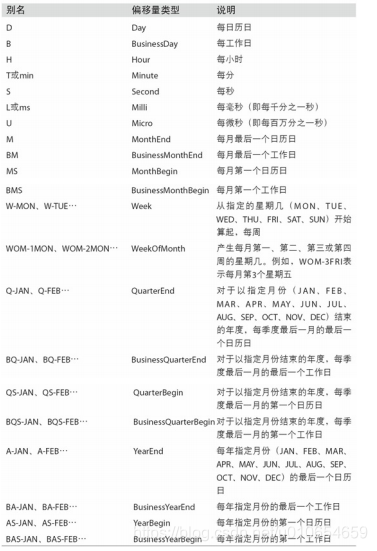

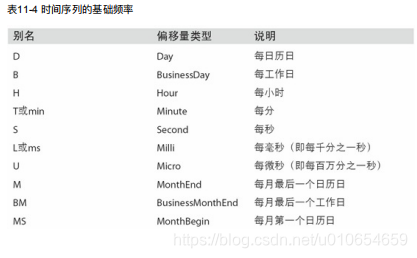

基本的时间序列函数有:

pd.date_range('2000-01-01', '2000-12-01', freq='BM')

#BM表示每月最后一个工作日

DatetimeIndex(['2000-01-31', '2000-02-29', '2000-03-31', '2000-04-28',

'2000-05-31', '2000-06-30', '2000-07-31', '2000-08-31',

'2000-09-29', '2000-10-31', '2000-11-30'],

dtype='datetime64[ns]', freq='BM')

频率和日期偏移量

按着某个频率进行时间上的选取。

相关的选择参数:

from pandas.tseries.offsets import Hour, Minute

pd.date_range('2000-01-01', '2000-01-03 23:59', freq='4h')

#4个小时选择一次数据

DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 04:00:00',

'2000-01-01 08:00:00', '2000-01-01 12:00:00',

'2000-01-01 16:00:00', '2000-01-01 20:00:00',

'2000-01-02 00:00:00', '2000-01-02 04:00:00',

'2000-01-02 08:00:00', '2000-01-02 12:00:00',

'2000-01-02 16:00:00', '2000-01-02 20:00:00',

'2000-01-03 00:00:00', '2000-01-03 04:00:00',

'2000-01-03 08:00:00', '2000-01-03 12:00:00',

'2000-01-03 16:00:00', '2000-01-03 20:00:00'],

dtype='datetime64[ns]', freq='4H')

pd.date_range('2000-01-01', periods=10, freq='1h30min')

#每隔1小时30分钟进行数据提取

DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 01:30:00',

'2000-01-01 03:00:00', '2000-01-01 04:30:00',

'2000-01-01 06:00:00', '2000-01-01 07:30:00',

'2000-01-01 09:00:00', '2000-01-01 10:30:00',

'2000-01-01 12:00:00', '2000-01-01 13:30:00'],

dtype='datetime64[ns]', freq='90T')

WOM日期

wom是week of month。

'WOM-3FRI’表示每个月第三个星期五。

移动(超前和滞后)数据

Series和DataFrame都有1个shift方法用于执行单纯的前移或后移操作,保持索引不变。

ts = pd.Series(np.random.randn(4),

index=pd.date_range('1/1/2000', periods=4, freq='M'))

print(ts)

print('\n')

print(ts.shift(2))

print('\n')

print(ts.shift(-2))

2000-01-31 -0.293180

2000-02-29 -0.593455

2000-03-31 -0.446006

2000-04-30 -0.811115

Freq: M, dtype: float64

2000-01-31 NaN

2000-02-29 NaN

2000-03-31 -0.293180

2000-04-30 -0.593455

Freq: M, dtype: float64

2000-01-31 -0.446006

2000-02-29 -0.811115

2000-03-31 NaN

2000-04-30 NaN

Freq: M, dtype: float64

ts / ts.shift(1) - 1

#可以表示一个时间序列或者多个时间序列中的百分比变化

2000-01-31 NaN

2000-02-29 1.024202

2000-03-31 -0.248458

2000-04-30 0.818619

Freq: M, dtype: float64

通过偏移量对日期进行位移

from pandas.tseries.offsets import Day, MonthEnd

now = datetime(2011, 11, 17)

now + 3 * Day()

Timestamp('2011-11-20 00:00:00')

now + MonthEnd()#时间会到now时间表示的这个月底

Timestamp('2011-11-30 00:00:00')

11.4 时区处理

import pytz

pytz.common_timezones[-5:]

['US/Eastern', 'US/Hawaii', 'US/Mountain', 'US/Pacific', 'UTC']

时区本地化和转换

rng = pd.date_range('3/9/2012 9:30', periods=6, freq='D')

ts = pd.Series(np.random.randn(len(rng)), index=rng)

print(ts)

2012-03-09 09:30:00 -0.736406

2012-03-10 09:30:00 -1.689875

2012-03-11 09:30:00 1.190183

2012-03-12 09:30:00 0.674204

2012-03-13 09:30:00 0.373736

2012-03-14 09:30:00 0.471685

Freq: D, dtype: float64

pd.date_range('3/9/2012 9:30', periods=10, freq='D', tz='UTC')

DatetimeIndex(['2012-03-09 09:30:00+00:00', '2012-03-10 09:30:00+00:00',

'2012-03-11 09:30:00+00:00', '2012-03-12 09:30:00+00:00',

'2012-03-13 09:30:00+00:00', '2012-03-14 09:30:00+00:00',

'2012-03-15 09:30:00+00:00', '2012-03-16 09:30:00+00:00',

'2012-03-17 09:30:00+00:00', '2012-03-18 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')

#通过tz_localize方法处理时间的本地化转换

ts_utc = ts.tz_localize('UTC')

#当时间转换到某个特定时区后,可以用tz_convent将其转换到其他时区中。

ts_utc.tz_convert('America/New_York')

2012-03-09 04:30:00-05:00 -0.736406

2012-03-10 04:30:00-05:00 -1.689875

2012-03-11 05:30:00-04:00 1.190183

2012-03-12 05:30:00-04:00 0.674204

2012-03-13 05:30:00-04:00 0.373736

2012-03-14 05:30:00-04:00 0.471685

Freq: D, dtype: float64

11.5 时期及其算术

时期的频率转换

Period和PeriodIndex对象都可以通过其asfreq方法被转换成别的频率.

p = pd.Period(2007, freq='A-DEC')

p+5

Period('2012', 'A-DEC')

p.asfreq('M', how='start')#转换为月的数据

Period('2007-01', 'M')

p.asfreq('M', how='end')

Period('2007-12', 'M')

rng = pd.period_range('2006', '2009', freq='A-DEC')

ts = pd.Series(np.random.randn(len(rng)), index=rng)

ts.asfreq('M', how='start')

2006-01 0.295788

2007-01 1.363306

2008-01 1.014115

2009-01 -0.556755

Freq: M, dtype: float64

按季度计算的时期频率

p = pd.Period('2012Q4', freq='Q-JAN')

#注意不同的freq参数,最后确定的数据也是不一样的

p.asfreq('D', 'start')

Period('2011-11-01', 'D')

rng = pd.period_range('2011Q3', '2012Q4', freq='Q-JAN')

ts = pd.Series(np.arange(len(rng)), index=rng)

print(ts)

2011Q3 0

2011Q4 1

2012Q1 2

2012Q2 3

2012Q3 4

2012Q4 5

Freq: Q-JAN, dtype: int32

将Timestamp转换为Period(及其反向过程)

rng = pd.date_range('2000-01-01', periods=3, freq='M')

ts = pd.Series(np.random.randn(3), index=rng)

pts = ts.to_period()

print(ts)

print('\n')

print(pts)

2000-01-31 1.730324

2000-02-29 0.947510

2000-03-31 1.073048

Freq: M, dtype: float64

2000-01 1.730324

2000-02 0.947510

2000-03 1.073048

Freq: M, dtype: float64

通过数组创建PeriodIndex

data = pd.read_csv('examples/macrodata.csv')

print(data.head(5))

year quarter realgdp realcons realinv realgovt realdpi cpi \

0 1959.0 1.0 2710.349 1707.4 286.898 470.045 1886.9 28.98

1 1959.0 2.0 2778.801 1733.7 310.859 481.301 1919.7 29.15

2 1959.0 3.0 2775.488 1751.8 289.226 491.260 1916.4 29.35

3 1959.0 4.0 2785.204 1753.7 299.356 484.052 1931.3 29.37

4 1960.0 1.0 2847.699 1770.5 331.722 462.199 1955.5 29.54

m1 tbilrate unemp pop infl realint

0 139.7 2.82 5.8 177.146 0.00 0.00

1 141.7 3.08 5.1 177.830 2.34 0.74

2 140.5 3.82 5.3 178.657 2.74 1.09

3 140.0 4.33 5.6 179.386 0.27 4.06

4 139.6 3.50 5.2 180.007 2.31 1.19

print(data.year)

0 1959.0

1 1959.0

2 1959.0

3 1959.0

4 1960.0

...

198 2008.0

199 2008.0

200 2009.0

201 2009.0

202 2009.0

Name: year, Length: 203, dtype: float64

index = pd.PeriodIndex(year=data.year, quarter=data.quarter,

freq='Q-DEC')

data.index = index

print(data.infl)

1959Q1 0.00

1959Q2 2.34

1959Q3 2.74

1959Q4 0.27

1960Q1 2.31

...

2008Q3 -3.16

2008Q4 -8.79

2009Q1 0.94

2009Q2 3.37

2009Q3 3.56

Freq: Q-DEC, Name: infl, Length: 203, dtype: float64

11.6 重采样及频率转换

高频到低频是降采样,低频到高频是升采样。

rng = pd.date_range('2000-01-01', periods=100, freq='D')

ts = pd.Series(np.random.randn(len(rng)), index=rng)

print(ts)

2000-01-01 -2.036950

2000-01-02 0.196854

2000-01-03 0.191711

2000-01-04 1.131291

2000-01-05 0.225399

...

2000-04-05 0.191335

2000-04-06 -1.054301

2000-04-07 0.571078

2000-04-08 0.314156

2000-04-09 -0.375186

Freq: D, Length: 100, dtype: float64

ts.resample('M').mean()

2000-01-31 0.071255

2000-02-29 -0.007097

2000-03-31 0.019090

2000-04-30 0.266123

Freq: M, dtype: float64

#降采样

rng = pd.date_range('2000-01-01', periods=12, freq='T')

ts = pd.Series(np.arange(12), index=rng)

print(ts)

2000-01-01 00:00:00 0

2000-01-01 00:01:00 1

2000-01-01 00:02:00 2

2000-01-01 00:03:00 3

2000-01-01 00:04:00 4

2000-01-01 00:05:00 5

2000-01-01 00:06:00 6

2000-01-01 00:07:00 7

2000-01-01 00:08:00 8

2000-01-01 00:09:00 9

2000-01-01 00:10:00 10

2000-01-01 00:11:00 11

Freq: T, dtype: int32

ts.resample('5min', closed='right').sum()

#默认情况下,面元的右边界是包含的,因此00:00到00:05的区间中是包含00:05的。

1999-12-31 23:55:00 0

2000-01-01 00:00:00 15

2000-01-01 00:05:00 40

2000-01-01 00:10:00 11

Freq: 5T, dtype: int32

OHLC重采样

第一个值、最后一个值、最大值、最小值。传入how='chlc’即可。

print(ts.resample('5min').ohlc())

open high low close

2000-01-01 00:00:00 0 4 0 4

2000-01-01 00:05:00 5 9 5 9

2000-01-01 00:10:00 10 11 10 11

升采样和插值

frame = pd.DataFrame(np.random.randn(2, 4),

index=pd.date_range('1/1/2000', periods=2,

freq='W-WED'),

columns=['Colorado', 'Texas', 'New York', 'Ohio'])

df_daily = frame.resample('D').asfreq()

print(df_daily)

Colorado Texas New York Ohio

2000-01-05 -0.141497 -0.299701 0.374013 -1.185863

2000-01-06 NaN NaN NaN NaN

2000-01-07 NaN NaN NaN NaN

2000-01-08 NaN NaN NaN NaN

2000-01-09 NaN NaN NaN NaN

2000-01-10 NaN NaN NaN NaN

2000-01-11 NaN NaN NaN NaN

2000-01-12 0.396594 -0.509955 1.038497 2.786482

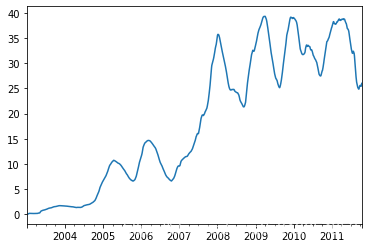

11.7 移动窗口函数

import matplotlib.pyplot as plt

close_px_all = pd.read_csv('examples/stock_px_2.csv',

parse_dates=True, index_col=0)

close_px = close_px_all[['AAPL', 'MSFT', 'XOM']]

close_px = close_px.resample('B').ffill()

close_px.AAPL.plot()

close_px.AAPL.rolling(250).mean().plot()

<matplotlib.axes._subplots.AxesSubplot at 0x92ce330>

appl_std250 = close_px.AAPL.rolling(250, min_periods=10).std()

appl_std250.plot()

<matplotlib.axes._subplots.AxesSubplot at 0x937d6f0>

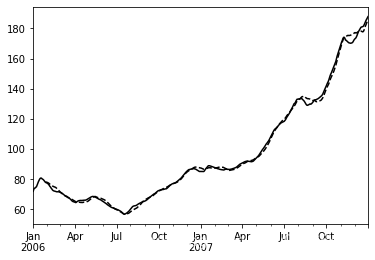

指数加权函数

aapl_px = close_px.AAPL['2006':'2007']

ma60 = aapl_px.rolling(30, min_periods=20).mean()

ewma60 = aapl_px.ewm(span=30).mean()

ma60.plot(style='k--', label='Simple MA')

ewma60.plot(style='k-', label='EW MA')

<matplotlib.axes._subplots.AxesSubplot at 0x95491f0>

说明:

放上参考链接,复现的这个链接中的内容。

放上原链接: https://www.jianshu.com/p/04d180d90a3f

作者在链接中放上了书籍,以及相关资源。因为平时杂七杂八的也学了一些,所以这次可能是对书中的部分内容的复现。也可能有我自己想到的内容,内容暂时都还不定。在此感谢原简书作者SeanCheney的分享

344

344

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言