ISLR(6)-压缩估计方法与正则化

Ridge & Lasso 在信用卡数据集的应用

笔记要点:

0.Shrinkage Method

1.Ridge Regression

-- scale control

2.Lasso

3.参考

0. Shrinkage Method

除了使用最小二乘法对包含预测变量子集的线性模型进行拟合, 还可以使用对系数进行约束或加罚的技巧对包含

- 引入这种约束会增加一点点误差, 但「显著减少了估计量方差」

1. Ridge Regression

在简单线性回归中, 通过最小化残差平方和RSS进行估计

岭回归的系数估计值通过最小化RSS+penalty的权衡得到

-

: 压缩惩罚(shrinkage penalty)

- it has the effect of shrinking the estimates of

towards zero

- it has the effect of shrinking the estimates of

-

: 调节参数 (tuning parameter)

-

controls the impact on the regression coefficient estimates

-

: the penalty grows, and all

will be minimized to 0

-

-

-

- 可以通过交叉验证选择合适的

- 可以通过交叉验证选择合适的

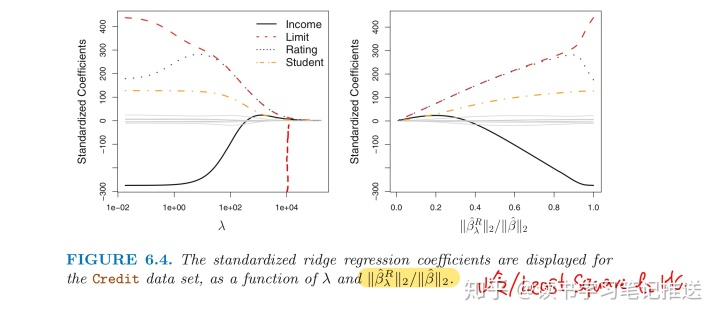

岭回归处理信用卡数据集

当

income,

limit,

rating,

student 的岭回归系数估计值

「趋近0」

-

「least squares coefficient estimates」

: the vector of

-

「

: the

of a vector, and measures the distance ofnorm」

from zero

- As

increases, the

norm of

「always decreasewill

0」

- and 「

will decrease」

- 「

: amount that the ridge regression coefficient estimates have been shrunken towards zero

norm ratio」

- a small value = close to zero

- and 「

「范围控制」

最小二乘估计是尺度不变的(scale invariant)

- Multiplying

by a constant

「scaling ofsimply leads to a

by a factor of」

- Regardless of how the

predictor is scaled,

will remain the same

岭回归的估计系数会随着预测变量的改变而显著改变:

- 因为岭回归公式中的

, 变量的扩大缩小倍数不能简单的改变系数估计值的变化

-

的最终预测结果不只是取决于

, 也取决于

的尺度

通过标准化将岭回归的所有变量缩到同一尺度:

- The denominator is the estimated standard deviation of the jth predictor among n samples

- 标准化后的变量标准差为1, 最后的拟合不再受变量尺度的影响

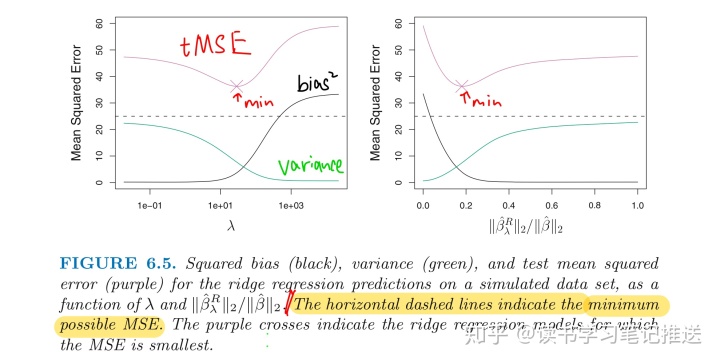

为什么岭回归提升最小二乘效果?

与最小二乘相比, 岭回归的优势在于它权衡了误差和方差

- as

increases, the flexibility of the ridge regression fit decreases,

- leading to slight increased bias

- but significant decreased variance

当响应变量和预测变量的关系接近线性时, 最小二乘估计会有较低的方差和「较大的方差」

- 训练集数据一个「微小的改变」可能导致最小二乘「系数的较大改变」

-

方差很大

-

最小二乘估计没有唯一解

- 岭回归通过偏差小幅上升来换取方差「大幅度下降」

-

「Ridge的优点」

Ridge regression has substantial computational advantages over best subset selection

- which requires searching through

models

For any fixed value of

- the model-fitting procedure can be performed as quickly as least squares

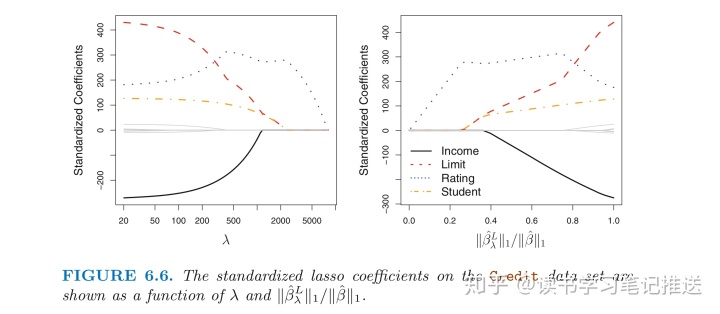

2. Lasso

「Ridge的劣势」

最优子集, 逐步方法会选择出变量的一个子集进行建模, 岭回归的最终模型包含全部p个变量

- 「

无法「确切」压缩0, 除非

惩罚项」

「Lasso」可以克服岭回归的缺点:

「

- Lasso和最优子集法类似, 完成了变量选择

- Lasso建立的模型与岭回归相比, 更易于解释

- Sparse Model 稀疏模型: the model that involve only a subset of the variables

- 同样可以通过交叉验证的方法选择好的

右图与岭回归的表现有很大的差异:

-

,

从1到0 (右=>左)

- Lasso首先和最小二乘一样, 然后

student和limit归零- 最后得到一个只包含

rating的模型,

- 最后得到一个只包含

根据不同的

- 岭回归得到的模型自始至终包含所有变量, 虽然系数估计值的大小会随着

变化

4. 参考:

- 《Introduction to Statistical Learning》

- 《老董聊卡》

3466

3466

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言