LOS 2.a

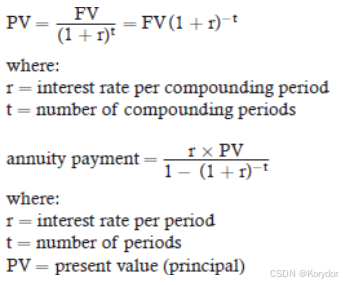

The value of a ixed-income instrument or an equity security is the present value of its future cash lows, discounted at the investor’s required rate of return:

The PV of a perpetual bond or a preferred stock![]() , where r = required rate of return.

, where r = required rate of return.

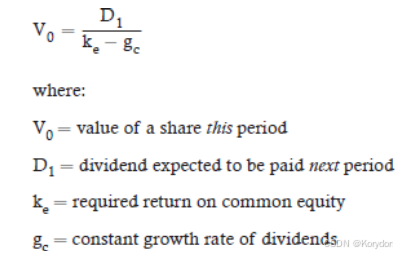

The PV of a common stock with a constant growth rate of dividends is:

LOS 2.b

By rearranging the present value relationship, we can calculate a security’s required rate of return based on its price and its future cash lows. The relationship between prices and required rates of return is inverse.

For an equity share with a constant rate of dividend growth, we can estimate the required rate of return as the dividend yield plus the assumed constant growth rate, or we can estimate the implied growth rate as the required rate of return minus the dividend yield.

LOS 2.c

Using the cash low additivity principle, we can divide up a series of cash lows any way we like, and the present value of the pieces will equal the present value of the original

series. This principle is the basis for the no-arbitrage condition, under which two sets of future cash lows that are identical must have the same present value.

990

990

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言