本节主要聚焦active management portfolio的构建

首先介绍一个关键概念:

excess of benchmark returns (adjusted for all costs),即 active return ()

无论fundamental or quantitative approach, 或 bottom-up or top-down strategy等等,active return主要有3个来源:

:投资组合里对因子K的敏感度;BK的B则是指benchmark

α:active return of the portfolio that can be attributed to the specific skills/strategies of the manager skills 如: security selection and factor timing

ε:the idiosyncratic return, often resulting from a random shock,可以再细分为:an incomplete factor model that ignores relevant factors 以及 exposure to idiosyncratic risks that either helped or hurt performance

(α + ε):return that cannot be explained by exposure to rewarded factors

fundamental approach runs a more concentrated portfolio, the portion of the active performance attributed to idiosyncratic risk will likely be greater

three main building blocks of portfolio construction(不是与3个来源一一对应):

1. rewarded factor weightings

2. alpha skills(主要强调择时timing)

3. position sizing (explains how each relates to the three broad sources of active returns)

position sizing influences all three components, its most dramatic impact is often on idiosyncratic risk

还有第4个 critical component:"breadth of expertise", is necessary to assemble these three building blocks into a successful portfolio construction process

The factor-oriented manager believes that she is skilled at properly setting and balancing her exposure to rewarded factors and maintains a diversified portfolio to minimize the impact of idiosyncratic risk

The stock picker believes that he is skilled at forecasting security-specific performance over a specific horizon and expresses his forward-looking views using a concentrated portfolio, assuming a higher degree of idiosyncratic risk

其中的benchmark一般用 market portfolio:would have an exposure (or beta, β) of 1 to the Market factor and no net exposure to other rewarded factors

这里的market portfolio是指理想化的市场组合,S&P500 其实也不是market portfolio,只是用来代表market portfolio的一个指数

most large-cap indexes usually have a β close to 1 to the Market factor, they usually have a negative sensitivity to the Size factor, indicating their large-cap tilt

回顾一些二级的小知识:

Independent decisions:uncorrelated decisions

fundamental law:

As a practical matter, long-term success is not achieved by being right all the time but, rather, by being right often through small victories achieved consistently over long periods

Both a bottom-up stock picker and a top-down sector rotator can run concentrated portfolios

Both a bottom-up value manager and a top-down risk allocator can run diversified portfolios

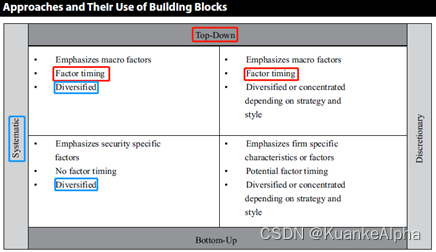

Factor timing is more likely to be implemented among discretionary managers, especially those with a top-down approach(与systemic的top-down一般也用factor timing没冲突)

另一个重要概念:Active risk is often referred to as “tracking error” or "tracking risk'

:active return at time t

衡量 benchmark-relative risk 的另一个 指标:Active Share

Active Share is 100%:a portfolio that shares no investments with those of the benchmark

active share的来源就2个:持有benchmark无的股票;持有benchmark也有的股票但比例不一致

Although portfolios that have higher active risk tend to have higher Active Share (and vice versa), this is not always the case

Active risk is affected by the degree of cross correlation, but Active Share is not

Active Share is not concerned with the efficiency of diversification

A portfolio manager can completely control Active Share, but she cannot completely control active risk because active risk depends on the correlations and variances of securities that are beyond her control

most multi-factor products have a low concentration among securities, typically have a high Active Share but they have reasonably low active risk (tracking error)

The concentrated stock picker, in contrast, has both a high Active Share and a high active risk

目前还没有研究指出high active share或high active risk如何能够转换成high active return

many investors are using Active Share to assess the fees that they pay per unit of active management,即同样收费和active return下,投资者会选择active share高的

the alpha of bottom-up managers is most likely attributable to their security selection skills

top-down managers’ alphas are largely derived from factor timing

If risk is being measured by predicted active risk, then the objective function is seeking to maximize the information ratio,属于relative framework

If risk is being measured by predicted portfolio volatility, then the objective function is seeking to maximize the Sharpe ratio,属于absolute framework

If you are assessing risk using a relative risk construct, you can no longer assume that a lower-risk asset reduces active risk or that a higher-risk asset increases it(因为与选取的benchmark有关)

The Market factor does not explain much of the active risk; the very action of building a portfolio that is structurally different from the market creates the active risk

The proportion of total portfolio variance contributed by Asset A is:0.008416/0.014212 = 59.22%(0.014212 是给出的 整个portfolio的total variance)

the variance attributed to the factor i:

∑coefficients(i) * coefficients(j) * covariance(i, j) / variance of the portfolio

一些小知识:

:the expected compounded/geometric return of an assetis

:expected arithmetic/periodic return

还有一些衡量risk的方法,不一一列举,如:

CVaR is the average loss that would be incurred if the VaR cutoff is exceeded

It is also sometimes referred to as the expected tail loss or expected shortfall

It is not technically a VaR measure

收益、风险都已经提及了,成本也是一个绕不开的话题

smaller-AUM funds may pay more in explicit costs (such as broker commissions), these funds may incur lower implicit costs (such as delay and market impact) than large-AUM funds

Slippage(延误)is often measured as the difference between the execution price and the midpoint of the bid and ask quotes at the time the trade was first entered

It incorporates both the effect of volatility/trend costs and market impact

Volatility/trend costs:costs associated with buying in a rising market and selling in a declining market

For some strategies, the true cost of slippage may be the opportunity cost of not being able to implement the strategy as assets grow

是指管理的规模变大后,超出基金经理的能力,无法在大规模下实施原规模声称的策略

Dark pools and crossing networks are examples of unlit venues

A well-constructed portfolio will not guarantee excess return relative to the appropriate benchmark, especially over a shorter horizon, but it will be designed to deliver the risk characteristics desired by the manager and promised to investors

equity组合的构建方法,本质上和equity-related hedge fund一样

long/short,long extension,market-neutral都是long/short的一种,只是:

1. long/short 只强调同时有long和short,可以是long 40% & short 60%

书中将long/short细分为:active extension, market neutral, and directional

long/short strategies are often less risky than long-only or short-only strategies

Operational risk is significantly greater with long/short investing

In the long/short approach, position weights are not necessarily constrained to sum to 1

The sum of the longs plus the absolute value of the shorts is called the portfolio’s gross exposure

The absolute value of the longs minus the absolute value of the shorts is called the portfolio’s net exposure(

)

A net exposure greater than zero implies some positive exposure to the Market factor

2. long extension是必须net exposure为long,如long 60% & short 40%;比较极端就是long 130% & short 30%

Long extension strategies are a hybrid of long-only and long/short strategies. They are often called “enhanced active equity” strategies

allows the strength of the positive and negative views to be expressed more symmetrically

构建方法:

builds a portfolio of long positions worth more than 100% of the wealth invested in the strategy and the short positions are funding the excess long positions, resulting gross leverage (即gross exposure > 100%) potentially allows for greater alpha and a more efficient exposure to rewarded factors

本质是 "gross exposure > 100%" & "net exposure = 100%"

3. Market-neutral strategies:ensure that the portfolio’s exposures to a wide variety of risk factors is zero

最简单的 Market-neutral portfolio:zero net investment, often called “dollar neutral”

But dollar neutral is not the same thing as market neutral

True market-neutral strategies hedge out most market risk

Market-neutral portfolio construction attempts to exactly match and offset the systematic risks of the long positions with those of the short positions(其实不止是market risk,可以拓展到其他risk也可以hedge out)

其本质目的是扬长避短规避掉自己不擅长判断的risk而专注于自己擅长的领域,如specific skills,所以一般仍有positive information ratio,且一般也无法 eliminate all risks

market-neutral strategies seek to remove major sources of systematic risk from a portfolio, these strategies are usually less volatile than long-only strategies

the correlation of market-neutral strategies with other types of strategies is typically quite low

A specific form of market-neutral strategy is pairs trading

A more quantitatively oriented form of pairs trading called statistical arbitrage (“stat arb”) :uses statistical techniques to identify two securities that are historically highly correlated with each other

注意:correlations between exposures are continually shifting

4. long only也可以认为是long/short的一种特例

Long-only investing, particularly strategies that focus on large-cap stocks, generally offers greater investment capacity than other approaches

这句的理解角度:在大盘股用long-only策略,一般可认为是无限制(因为那一点点买卖根本对股价无影响)

Long-only strategies may face capacity constraints, however, if they focus on smaller and illiquid stocks or employ a strategy reliant on a high level of portfolio turnover

the capacity of short-selling strategies is limited by the availability of securities to borrow

这里的investment capacity应该理解为实现投资的能力而不是是否够钱去投资

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言