本节主要介绍另一种 active strategy:credit strategy

同样先介绍一些基本概念,再介绍策略(这章的知识感觉比较庞杂)

credit valuation adjustment (CVA)考虑了两样:default risk (also called probability of default:POD);loss severity (also called loss given default:LGD)

不考虑time value的话:(credit) Spread ≈ LGD × POD

this estimate works well for bonds trading close to par, 而 distressed bonds tend to trade on a price rather than a spread basis,这种情况就应该用 recovery rate:1 − LGD 而不是credit spread

credit loss rate = POD * LGD

credit loss rate 与 credit spread 的区别:

loss rate 是事后的实际损失率,而 spread 是事前投资者要求的 spread,所以貌似公式一样,实际使用的参数不同

credit loss rate represents the realized percentage of par value lost to default for a group of bonds, or the bonds’ default rate multiplied by the loss severity

判断 Credit Cycle and Credit Spread Curve Changes,一般是指近期(即short-term)的变化,而假设长期维持较原来稳定的水平:

ie:in an economic downturn,是近期的 credit spread 上升,导致 credit curve flatten;而不是 credit curve 整个steepen

empirical duration:observed negative correlation between high-yield credit spreads and government benchmark yields to maturity:

analytical duration calculation overestimates the price gain versus the empirical duration estimate(即 empirical duration 一般比 analytical duration 小)

一般是出现 flight to quality 时,低YTM(往往是 high credit quality)的政府债比 high-yield的公司债还值钱:the magnitude of credit spread changes is greater for lower- versus higher-rate bonds

现在介绍各种spread:

(1)(risky asset) yield spread = (risky asset) YTM - YTM on the nearest on-the-run government bond

(2)G-spread = (risky asset) YTM - YTM on maturity-matched government bond with interpolation calculation

书中例题有一种小应用:假设 G-spread 不变,只要其中有一期的 risk-free government bond有变化,会导致按 interpolation calculation 计出的 benchmark yield 不同,这就会导致用 risky = risk-free + spread 倒算出的 risky 不同了

计 fair value spread for the new issue based on outstanding debt 应该用对应期限的 G-spread + new issue premium(这项题目会给)

(3)I-spread (interpolated spread):uses interest rate swaps as the benchmark

it incorporates yield levels using a point on the curve to estimate a risky bond’s yield spread rather than the term structure of interest rates

is limited to option-free bonds as a credit risk measure

(4)asset swap spread (ASW) = the bond’s fixed coupon rate - (the fixed rate on an interest rate swap + MRR)

the fixed rate on an interest rate swap 是 swap spread,而不是 swap rate

ASW = (risky) bond coupon - (maturity-matched) swap rate = coupon - (swap spread + MRR),MRR其实就是risk-free yield

I-spread = (risky) bond yield - swap rate(这里提的 yield 可以理解为是 YTM)

Asset swaps convert a bond’s periodic fixed coupon to MRR plus (or minus) a spread

即定义 asset swap 为 MRR + ASW,区别于 swap rate

要注意区分 asset swaps 和 asset swap spread(ASW)

后面会介绍 asset swap 在 management liquidity risk 的应用

(5)zero-volatility spread (Z-spread)

While both the G-spread and I-spread use the same discount rate for each cash flow, a more precise approach incorporating the term structure of interest rates is to derive a constant spread over a government (or interest rate swap) spot curve instead

more accurate than either the G-spread or I-spread

assumes zero volatility and therefore does not capture the value of bond options

Credit default swap (CDS) basis refers to the difference between the Z-spread on a specific bond and the CDS spread of the same (or interpolated) maturity for the same issuer

Negative basis arises if the yield spread is above the CDS spread, and positive basis indicates a yield spread in excess of the CDS market

所以 CDS (basis) = CDS-spread - Z-spread

CDS price 在后面介绍

参考品职的解释,小结 basis trade 原理:

credit spread 和 CDS spread 是分别从债券市场的角度和债券衍生品市场的角度去衡量credit risk,对于同一个债券两者应该相等,但由于CDS是标准化合约且本身不含权,再加上期限不匹配以及用来衡量 credit spread 的各种 spread 各有优劣,导致 credit spread 与 CDS spread 会出现不一样的情况,这时就可以用 basis trade 来套利了,只是 CDS basis 指定了用 Z-spread 来代表债券市场角度衡量 credit risk;而 CDS-spread 本身并没有剔除权利的影响,所以用 Z-spread 又比用 OAS 好。

CDS basis < 0,即 Z-spread 要下降 & CDS-spread 要上升 来消除套利空间,所以应该 long bond 同时 buy CDS(保费要升,趁现在低价买入,buy CDS 即 short CDS) ;

反之 CDS basis > 0,short bond & long CDS

option-adjusted spread (OAS) is a generalization of the Z-spread calculation that incorporates bond option pricing based on assumed interest rate volatility:

OAS is the constant yield spread over the zero curve which makes the arbitrage-free value of such a bond equal to its market price

OAS approach is the most appropriate yield spread measure for active fixed-income portfolio managers

the main drawback of the OAS is that it is highly dependent on volatility and other model assumptions

OAS is the most widely accepted credit spread measure

it incorporates a volatility assumption to account for the value of bond options

介绍一些工具:

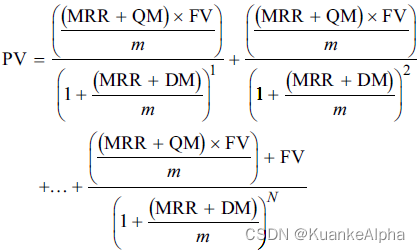

floating-rate notes (FRNs):

quoted margin (QM):每期付息 = (MRR + QM)/m,m:一年付息m期

discount margin (DM):FRN每期的利息和折现率都是基于MRR,利率是(MRR+QM)/m,而折现率则是 (MRR+DM)/m

MRR is based on current MRR and therefore implies a flat forward curve

QM一般是考虑了credit risk,但如果合同约定QM本身是一个基于 rating 变化的相对固定数则这里的QM不含credit risk(总结就是要理解不能死记硬背)

FRN is priced at par on a rate reset date,即 On each reset date, the floater will be priced at par value

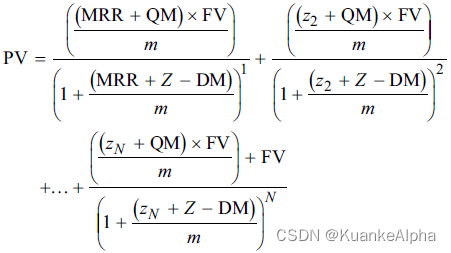

zero-discount margin (Z-DM):

Z-spread for fixed rate bond,Z-DM for FRN

对于FRN而言,z1=MRR,所以是后面是要对比:QM vs zi+DM(in an upward-sloping yield curve 即 zi 是上升, the Z-DM will be below the DM)

介绍了一大堆的零散知识,主要都是围绕 credit,而这正是本节的重点,一般会将 credit spread 单独拿出来研究,所以:

将 E(expected change on yield) 这项的第一部分 - (EffSpreadDur * Δspread) 称为 spread duration(一般会用 OAS duration 来衡量 credit spread,这时则称为OAS duration)

固收1中提过:Duration Times Spread (DTS) ≈ (EffSpreadDur × Spread),这是YC静态时的一个概念,不要将两者混淆,是不同YC状态下的同一个东西

应用:给出OAS由125bp widens by 10bp、OAS、EffspreadDur,求组合的 performance,即

E = DTS * 10/125 = (OAS * EffspreadDur) * 10/125 = 60bp,即 expected 60 bps p.a. widening for the bond portfolio.

这节知识点比较多,引入了很多近似的概念,很容易混淆,如马上又引入:

excess spread (return) vs. E(ExcessSpread)

(1)ExcessSpread ≈ − (EffSpreadDur × ΔSpread)

若给出年化,而只持有半年的话,要去年化(除2)

credit spread narrows 即 Δspread为负(用期末减期初就最直观,不易搞混)

(2)E[ExcessSpread] ≈ − (EffSpreadDur × ΔSpread) − (POD × LGD)

其实就是多考虑了default

POD、LGD一般给年化的,若只持有半年也是要去年化

instantaneous (holding period of zero) 即 = 0

当比较 issuers with different credit-related risk, the investor must decide whether the additional spread is sufficient compensation for the incremental exposure,这时就是要应用E[ExcessSpread]

(1)当假设 no change in spreads,计 estimated excess return

即 E(excess spread) = − (EffSpreadDur × 0) − (POD × LGD)

(2)比较 Which bond is more attractive if spreads are expected to widen by 10%:仍是计E(excess spread),

注意DTS、E(expected change on yield) 的公式中 Δspread 用比例,而 E(excess spread) 中的Δspread 可不是

若原来的 spread 是 x bp,则 Δspread 是 x*10% bp 而不是 10%

大量铺垫过后,现在开始正式学习 credit strategy,三种:

(1)an individual security selection process or bottom-up approach

typically begins with a manager defining the universe of eligible bonds within a mandate and then grouping the universe into categories that allow consistent relative value analysis across comparable borrowers

如 divide eligible bonds into industry sectors, subsectors and/or firms located in different jurisdictions

statistical credit analysis models to measure individual issuer creditworthiness can be categorized as:

reduced form credit models

solve for default intensity, or the POD over a specific time period, using observable company-specific variables(ie. financial ratios)& recovery assumptions as well as macroeconomic variables, including economic growth and market volatility measures

Z-score

structural credit models

use market-based variables to estimate the market value of an issuer’s assets & the volatility of asset value

The likelihood of default is defined as the probability of the asset value falling below that of liabilities

Moody’s Analytics Expected Default Frequency (EDF) & Bloomberg’s Default Risk (DRSK) models

The EDF model estimates a forward-looking POD defined as the point at which the market value of assets falls below a firm’s obligations

Both the EDF and DRSK approaches are sometimes referred to as “distance to default” models because a probability distribution is used to determine how far an issuer’s current market value of assets is from the default threshold for a given period

(2)macro- or market-based, top-down approach

Macro factors include:economic growth, real rates and inflation, changes in expected market volatility and risk appetite, recent credit spread changes, industry trends, geopolitical risk, and currency movements(标颜色的两点不是区分的判断依据,bottom-up的 reduced form 也有)

top-down approach的分类更广,如分成investment-grate,而bottom-up是分成医疗、石油等

Top-down credit strategies are often based on macro factors and group investment choices by credit rating and industry sector categories

ratings tend to lag the market’s pricing of credit risk

S&P ratings focused on the POD, while Moody’s focuses on expected losses

The use of spread-based rather than rating-based measures,一般 spread-based 更被推崇

(3)combination of both

Factor-Based Credit Strategies

based on style factors

the application of systematic risk factors such as size, value, and momentum in fixed-income markets is relatively new

有一位学者指出4种有效因子:carry, defensive, momentum, value

increasingly include ESG factors

Green bonds are fixed-income instruments that directly fund ESG-related initiatives such as those related to environmental or climate benefits

现在讲解另一个知识点:liquidity risk & tail risk

For bonds quoted actively on a request-for-quote system by individual dealers, the effective spread transaction cost statistic:

is an inadequate gauge of trading costs for positions that are traded in smaller orders over time and/or whose execution affects market spreads

Fixed-income ETFs

create and redeem shares using an OTC primary market that exists between a set of institutional investors (or authorized participants) and the ETF sponsor

trade in the secondary market on an exchange, overcoming the liquidity constraints of individual OTC-traded bonds

用 asset swap 来 management liquidity risk:

asset swap 的概念已在上面介绍过

假设持有15年期债券,一般由于日交易量远小于所持数量,所以要 enter asset swap 来 hedge(manage the benchmark interest rate risk associated with liquidating this bond position)

因为原持仓是 long spread duration,所以现在要 short duration,即 pay fixed & receive floating

且 unwinding the swap position over time in proportion to the amount of the bond sold,即动态调整

VaR 会misleading的原因:

VaR tends to underestimate the frequency and severity of extreme adverse events

fails to capture the downside correlation and liquidity risks associated with market stress scenarios

fails to quantify the average or expected loss under an extreme adverse market scenario,只是 addresses minimum loss for a specific confidence level

Conditional value at risk (CVaR), or expected loss(expected shortfall):

measures the average loss over a specific time period conditional on that loss exceeding the VaR threshold

often measured using historical simulation or Monte Carlo techniques

incremental VaR (or partial VaR):

measure the impact of adding or removing a portfolio position

relative VaR:

measure the expected tracking error versus a benchmark portfolio

3 种常用的估计参数的方法:parametric method,historical simulation,monte carlo analysis

parametric 假设 return 服从正态分布且不适用于含权债券;蒙特卡罗法也有model assumption(如每步怎么走,只是不假设回报服从正态分布而已)

Hypothetical scenario analyses are often used to supplement these three methods

上面的 reduced form 和 structural model 都是会估计 volatility,而这对于估计 tail risk 也很重要

CDS(credit default swap)

CDS is the basic building block for strategies to manage credit risk separately from interest rate risk

often more liquid than an issuer’s underlying bonds

usually quoted on an issuer’s CDS spread

hazard rate 就是首次违约率

CDS Price ≈ 1 + [ (Fixed Coupon − CDS Spread) × ]

CDS Spread is the issuer’s current CDS market spread,而 fixed coupon 则是规定的:1% for investment-grade,5% for high-yield,所以造成会有可能出现价差

计出是负数则 CDS protection buyer 反而会先收到补偿

fixed coupon相当于每期续保的保费,要每期给 CDS seller 的

notional is not exchanged 而是用来计算赔额的

CDS spread widen 的话,CDS buyer是有 mark-to-market gain,因为这个公式其实计出的是违约的话要按多少比例来赔(名字叫 pricing 会易让人疑惑而已),之前某个 bond 可以按 10% 来赔,现在如果再想投保就只能按 7% 来赔,之前买了这个保险的当然是有 gain

CDS price 公式变形推导得:

Δ(CDS Price)/Δ(CDS Spread) ≈ − [ Δ(CDS Spread) × ]

如果只是给出 rating 本来也可以对应知道是 investment-grade 还是 high-yield,但没明确说的话(即 fixed coupon 不知道)就应该用这个公式

Δ(CDS Spread) 是绝对值,不是变化百分比;计出的数再乘 notional 就是影响值

预期 CDS widen 的话,即预期 credit risk 变高,需要 underweight 这个 issuer 的 bond,就要purchase 对应的CDS

Payer Option on CDS:Option buyer pays premium for right to buy protection

Receiver Option on CDS:Option buyer pays premium for right to sell protection

CDS strategies 所说的 credit curve 是 CDS curve 而不是之前的 credit curve 了

CDS curve 其实是表示 default probability,越高表示违约率越高

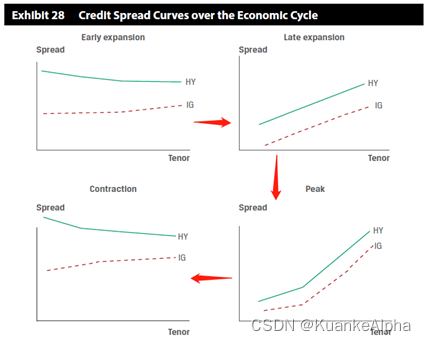

接下来是属于 credit spread curve strategy 的内容

early expansion

HY bond 的 credit 与 IG 不一致,反而 HY 的与常识一致会 flatten(flat to inverted),而 IG的就是正常的上升

lower (near-term) credit spread levels

late expansion

HY 和 IG 都是最正常的,变成时间主导,时间越长的越易违约,所以都是向上且应理解为是短期 decline 而不是长期 raise

peak

HY 和 IG 仍然形状一致,但这时期应理解为长期 raise 导致的 steepen(应该除了这里要理解为长期变化,其他地方都是按长期不变,短期变化来理解)

contraction/recession

HY 和 IG 都是由于短期的上升导致 flatten,HY 甚至会 inverting in some instances

if an investor’s views/forecast coincide with current credit spread curves, managers will choose active credit strategies consistent with static or stable credit market conditions

Static Credit Spread Curve Strategies:

lowering the portfolio’s average credit rating

adding credit spread duration:“buy and hold” or “carry and roll down” approach

CDS的策略:

如:经济下行时应该买/卖 IG CDS or HY CDS?第一反应会是买HY CDS(因为预期违约率变高所以要先买保障),其实正好相反,应该 买 IG CDS & 卖 HY CDS

因为CDS这个产品是相当于保费定死了是 1% 和 5%,所以都是收那么点钱,HY CDS 会升值所以高卖,而 IG 的违约率相对还是稳定的,需要继续维持这份保障

经济下行时要买IG CDS & 卖HY CDS:sell CDS其实是sell CDS protrction,即long CDS

定下了策略,就要看这个策略能赚多少:

第一项:收coupon = (5%-1%)*面值

第二项:price appreciation,即(CDS - CDS

)* long的面值 + (CDS

- CDS

)*(- short的面值)

注意,持有至 t 时,t 时刻的 EffDur 已经不同了,所以计CDS 要用 t 时刻对应的 EffDur

Investors distinguish between international credit markets in developed market countries versus emerging or frontier markets

Emerging or frontier fixed-income markets on the other hand are often dominated by sovereign issuers, state-owned or controlled enterprises, banks, and producers operating in a dominant domestic industry such as basic commodities

most developed markets face common macroeconomic factors that influence the bond term premium and expected returns

The euro-denominated 5-year European iTraxx Crossover index (iTraxx-Xover) of liquid high-yield issuers (with a 5% fixed premium) is currently trading at 400 bps with an of 4.25

这句的意思是:CDS spread = 400/10000 = 4%

government debt to GDP and the annual government budget deficit (or surplus) as a percentage of GDP are common measures of indebtedness and fiscal stability

Emerging markets are usually characterized by non-reserve currency regimes with significant external debt denominated in major foreign currencies

external debt to GDP and currency reserves as a percentage of GDP as key leverage and liquidity measures of creditworthiness, respectively

Credit quality in the emerging market credit universe exhibits a high concentration in lower investment-grade and upper high-yield ratings categories

这反映在 sovereign ceiling 即 a company’s rating is typically no higher than the sovereign credit rating of its domicile

emerging markets offer investors the opportunity to exploit divergence from interest rate parity conditions (known as the forward rate bias) by investing in higher-yielding currencies

因为按 UIRP 平价理论 HY 的货币应该贬值但短期往往不会马上贬,所以有套利机会

structured credit 的几个产品中 covered bond 值得提一下,因为底层资产是 Senior debt obligations backed by pool of commercial/residential mortgages or public sector assets,另外几个都是 Fixed-income securities backed by xxx

covered bond 有 dual recourse (both the issuing financial institution and the underlying asset pool)

covered bonds usually involve lower credit risk and a lower yield

习题遇到:MBS subportfolio 一般是对标 callable bond,所以比较 MBS 和 option-free bond 按比较 callable bond 和 option-free bond

Liquidity risk in credit markets is higher than in equities because of market structure differences and is often addressed using liquid bonds for short-term tactical positioning, less liquid positions for buy-and-hold strategies

1080

1080

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言