Wiener过程是连续时间随机过程,以纪念Norbert Wiener命名。 通常用于用随机成分表示噪音或财务状况。

可以计算几何布朗运动以可视化某些界限(以分位数表示)以暗示绝对范围。 为了进行计算,需要以下参数:

- µ(mu):平均百分比

- σ(sigma):方差

- t:时间段

- v:初始值

常规计算的扩展使用:m:每个时间段的增值(在我的情况下为月度值)中断:分位数中断以计算界限

计算值的代码:

import java.time.LocalDate;

import java.util.*;

import static java.lang.Math.sqrt;

import static java.lang.Math.exp;

public class WienerProcess {

/**

* Run the Wiener process for a given period and initial amount with a monthly value that is added every month. The

* code calculates the projection of the value, a set of quantiles and the brownian geometric motion based on a

* random walk.

*

* @param mu mean value (annualized)

* @param sigma standard deviation (annualized)

* @param years projection duration in years

* @param initialValue the initial value

* @param monthlyValue the value that is added per month

* @param breaks quantile breaks

* @return a List of double arrays containing the values per month for the given quantile breaks

*/

public static List<double[]> getProjection(double mu, double sigma, int years, int initialValue,

int monthlyValue, double[] breaks) {

double periodizedMu = mu / 12;

double periodizedSigma = sigma / Math.sqrt(12);

int periods = years * 12;

List<double[]> result = new ArrayList<double[]>();

for (int i = 0; i < periods; i++) {

double value = initialValue + (monthlyValue * i);

NormalDistribution normalDistribution = new NormalDistribution(periodizedMu * (i + 1),

periodizedSigma * sqrt(i + 1));

double bounds[] = new double[breaks.length];

for (int j = 0; j < breaks.length; j++) {

double normInv = normalDistribution.inverseCumulativeProbability(breaks[j]);

bounds[j] = value * exp(normInv);

}

result.add(bounds);

}

return result;

}

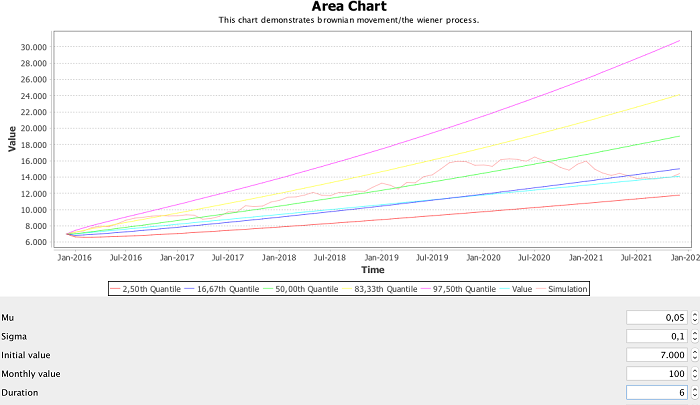

}应用值:

- 亩:0.05(或5%)

- sigma:0.1(或10%)

- 初始值:7000

- 每月增加:100

- 时间:6年

结果如下表:

- 该代码可从Github获得。 它带有Swing GUI来输入值并根据计算结果绘制图表。 https://gist.github.com/mp911de/464c1e0e2d19dfc904a7

相关信息

翻译自: https://www.javacodegeeks.com/2015/12/geometric-brownian-motion-java.html

724

724

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言