本文部分代码参考github:Machine-Learning-for-Beginner-by-Python3

本文所有代码和数据集文件可在此下载:https://download.csdn.net/download/ljw_study_in_CSDN/19546447

文章目录

(一)线性回归和多项式回归

根据给定数据集,利用线性回归和多项式回归模型训练和测试一个数据预测模型,并对模型的性能和预测能力进行分析;

1. 线性回归(最小二乘法/梯度下降法)

实验代码:

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from sklearn import preprocessing as spp # 引入数据预处理的库

# 在训练样本集的最后一列加1

def Trans(xdata):

ones = np.ones(len(xdata)).reshape(-1, 1)

xta = np.append(xdata, ones, axis=1)

return xta

# 利用传统的最小二乘法求解参数,即公式 W=(XT.X)-1*XT.Y

def ljw_leastsq(xdata, ydata):

xdata = Trans(xdata)

xTx = np.dot(xdata.T, xdata)

# 判断行列式是否为零

if np.linalg.det(xTx) == 0:

print("the Matrix cannot do inverse!")

return

invert = np.linalg.inv(xTx) # 求逆阵

ws = np.dot(np.dot(invert, xdata.T), ydata)

return ws

# 梯度下降法

def Gradient(xdata1, ydata, learn_rate=0.1, iter_times=100000, error=1e-8):

xdata = Trans(xdata1)

# 系数w,b的初始化

weights = np.zeros((xdata.shape[1], 1)) # (len(xdata[1]), 1))

# 存储成本函数的值

cost_function = []

for i in range(iter_times):

# 得到回归的值

y_predict = np.dot(xdata, weights)

# 最小二乘法计算误差

cost = np.sum((y_predict - ydata) ** 2) / len(xdata)

cost_function.append(cost)

# 计算梯度

dJ_dw = 2 * np.dot(xdata.T, (y_predict - ydata)) / len(xdata)

# 更新系数w,b的值

weights = weights - learn_rate * dJ_dw

# 提前结束循环的机制

if len(cost_function) > 1:

if 0 < cost_function[-2] - cost_function[-1] < error:

break

return weights

def predict(xdata, ws):

xt = Trans(xdata)

return np.dot(xt, ws)

# 读入文本文件数据并对x进行归一化处理

def preprocess_data(filename):

data = pd.read_table(filename, header=None).values

x = data[:, 0].reshape(-1, 1) # 将x由列表转化为二维数组

y = data[:, 1].reshape(-1, 1) # 将y由列表转化为二维数组

x = spp.MinMaxScaler().fit_transform(x) # 对x进行极大极小归一化

return x, y

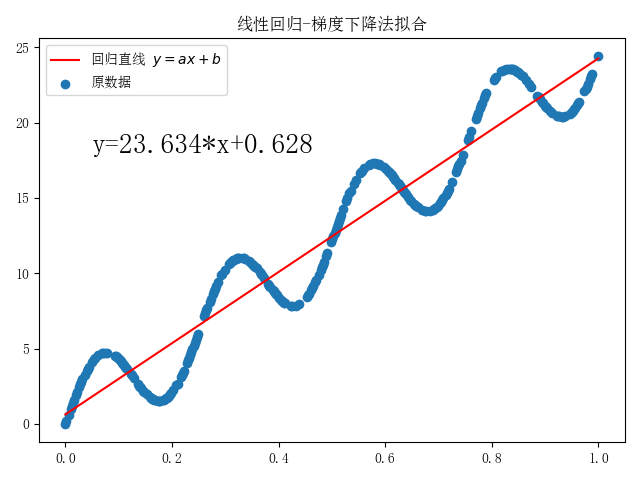

def draw(pic_num, fun, title):

plt.figure(pic_num)

w = fun(x_train, y_train) # 用最小二乘函数或梯度下降函数,求解参数

plt.plot(x_train, predict(x_train, w), "r", label="回归直线 $y=ax+b$") # 拟合的直线(标为红色)

plt.scatter(x_train, y_train, label="原数据") # 原数据的散点图

plt.legend()

s = "y=" + str(round(w[0][0], 3)) + "*x+" + str(round(w[1][0], 3)) # 回归直线

plt.text(0.05, 18, s, fontsize=20)

plt.title(title)

plt.show()

if __name__ == "__main__":

x_train, y_train = preprocess_data("train.txt")

plt.rcParams['font.sans-serif'] = 'SimSun' # 设置中文字体

draw(1, ljw_leastsq, "线性回归-最小二乘法拟合")

draw(2, Gradient, "线性回归-梯度下降法拟合")

实验结果:

从上图可以发现,当设置梯度下降法的超参数error=1e-8时,与最小二乘法计算得到的系数w相差较小。通过不断调小参数error,梯度下降法算出的系数将更接近最小二乘法计算出的结果。

2. 多项式回归

实验代码:

import numpy as np

import pandas as pd

from scipy.optimize import leastsq

import matplotlib.pyplot as plt

# 定义多项式,w为多项式的系数

def fit_func(w, x):

f = np.poly1d(w) # np.ploy1d()用来构造多项式,默认 ax^3+bx^2+c^x+d

return f(x)

# 残差函数

def err_func(w, x, y):

ret = fit_func(w, x) - y

return ret

# n项(最高n-1次)多项式拟合,有n个系数

def n_poly(n, x, y):

w_init = np.random.randn(n) # 生成n个随机数作为参数初值

parameters = leastsq(err_func, w_init, args=(np.array(x), np.array(y))) # 调用最小二乘法,x,y为列表型变量

return parameters[0]

def read_data(filename): # 读入文本文件数据

data = pd.read_table(filename, header=None).values

return data[:, 0], data[:, 1]

if __name__ == '__main__':

x_train, y_train = read_data("train.txt") # 读入数据

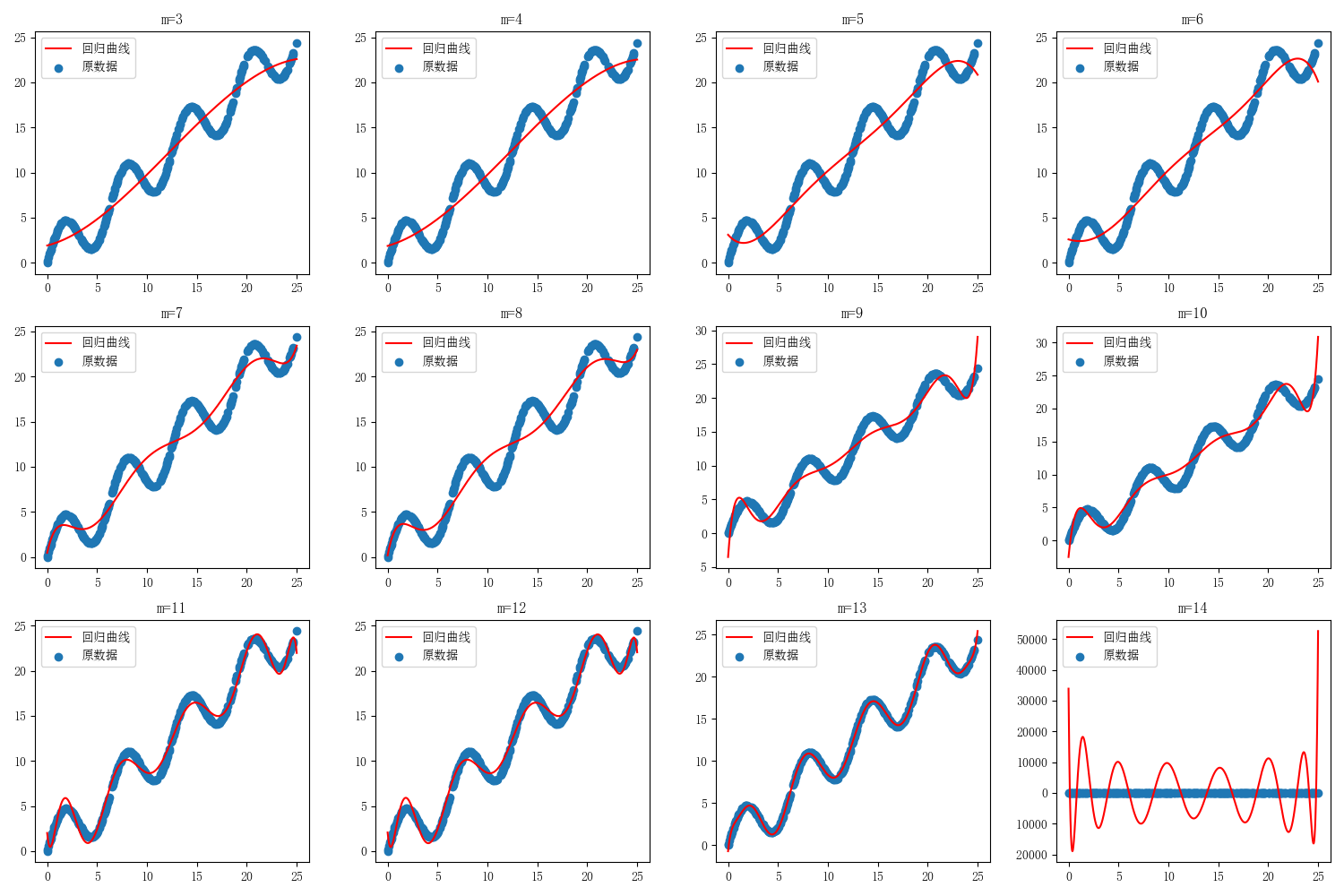

x_temp = np.linspace(0, 25, 10000) # 绘制拟合回归时需要的监测点

row = 3

col = 4

plt.rcParams["font.sans-serif"] = "SimSun" # 设置中文字体

# 绘制子图,子图大小row*col,绘制出m次多项式的拟合回归,m设为3~14

fig, ax = plt.subplots(row, col, figsize=(15, 10))

m_num = row * col

m = np.linspace(3, 3 + m_num - 1, m_num).astype(int) # m = [3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14]

for i in range(row):

for j in range(col):

m_index = i * col + j

ax[i, j].plot(x_temp, fit_func(n_poly(m[m_index] + 1, x_train, y_train), x_temp), 'r') # 拟合的曲线(标为红色)

ax[i, j].scatter(x_train, y_train) # 原数据的散点图

ax[i, j].set_title("m=" + str(m[m_index]))

ax[i, j].legend(labels=["回归曲线", "原数据"])

plt.show()

实验结果:

分别令最高幂次m=3,4,5,6,7,8,9,10,11,12,13,14。

从上图可以发现m=13时,多项式模型拟合效果最好。

(二)利用线性回归模型进行波斯顿房价预测

利用马萨诸塞州波士顿郊区的房屋信息数据,利用线性回归模型训练和测试一个房价预测模型,并对模型的性能和预测能力进行测试分析;

实验代码:

import numpy as np

import pandas as pd

from sklearn import preprocessing as spp # 引入数据预处理的库

import matplotlib.pyplot as plt # 绘图

from pylab import mpl

# 创建线性回归的类

class LinearRegression:

def __init__(self, learn_rate=0.2, iter_times=200000, error=1e-9):

self.learn_rate = learn_rate

self.iter_times = iter_times

self.error = error

def Trans(self, xdata):

one1 = np.ones(len(xdata))

xta = np.append(xdata, one1.reshape(-1, 1), axis=1)

return xta

# 梯度下降法

def Gradient(self, xdata, ydata):

xdata = self.Trans(xdata)

# 系数w,b的初始化

self.weights = np.zeros((len(xdata[0]), 1))

# 存储成本函数的值

cost_function = []

for i in range(self.iter_times):

# 得到回归的值

y_predict = np.dot(xdata, self.weights)

# 最小二乘法计算误差

cost = np.sum((y_predict - ydata) ** 2) / len(xdata)

cost_function.append(cost)

# 计算梯度

dJ_dw = 2 * np.dot(xdata.T, (y_predict - ydata)) / len(xdata)

# 更新系数w,b的值

self.weights = self.weights - self.learn_rate * dJ_dw

# 提前结束循环的机制

if len(cost_function) > 1:

if 0 < cost_function[-2] - cost_function[-1] < self.error:

break

return self.weights, cost_function

# 根据公式

def Formula(self, xdata, ydata):

xdata = self.Trans(xdata)

self.weights = np.dot(np.dot(np.linalg.inv(np.dot(xdata.T, xdata)), xdata.T), ydata)

y_predict = np.dot(xdata, self.weights)

cost = [np.sum((ydata - np.mean(ydata)) ** 2) / len(xdata)] # 开始是以y值得平均值作为预测值计算cost

cost += [np.sum((y_predict - ydata) ** 2) / len(xdata)] # 利用公式,一次计算便得到参数的值,不需要迭代。

return self.weights, cost # 包括2个值

# 预测

def predict(self, xdata):

return np.dot(self.Trans(xdata), self.weights)

def figure(title, *datalist):

for jj in datalist:

plt.plot(jj[0], '-', label=jj[1], linewidth=2)

plt.plot(jj[0], 'o')

plt.grid()

plt.title(title)

plt.legend()

plt.show()

# 计算R2的函数

def getR(ydata_tr, ydata_pre):

sum_error = np.sum(((ydata_tr - np.mean(ydata_tr)) ** 2))

inexplicable = np.sum(((ydata_tr - ydata_pre) ** 2))

return 1 - inexplicable / sum_error

# 读取数据并进行数据预处理

def preprocess_data(percent=0.1):

data = pd.read_csv(r'Boston.csv')

xdata = data.drop('MEDV', axis=1).values

xdata = spp.MinMaxScaler().fit_transform(xdata) # 归一的x值,y值分为训练数据集和预测数据集

ydata = data['MEDV']

sign_list = list(range(len(xdata)))

# 用于测试的序号

select_sign = sorted(np.random.choice(sign_list, int(len(xdata) * percent), replace=False))

# 用于训练的序号

no_select_sign = [isign for isign in sign_list if isign not in select_sign]

# 测试数据

x_predict_data = xdata[select_sign]

y_predict_data = ydata[select_sign].values.reshape(len(select_sign), 1) # 转化数据结构

# 训练数据

x_train_data = xdata[no_select_sign]

y_train_data = ydata[no_select_sign].values.reshape(len(no_select_sign), 1) # 转化数据结构

return x_train_data, y_train_data, x_predict_data, y_predict_data # 训练集、测试集

if __name__ == "__main__":

regressor = LinearRegression()

lrdata = preprocess_data() # 可用于算法的数据

train_error = regressor.Gradient(lrdata[0], lrdata[1]) # 开始训练

predict_result = regressor.predict(lrdata[2]) # 用于预测数据的预测值

train_pre_result = regressor.predict(lrdata[0]) # 用于训练数据的预测值

mpl.rcParams['font.sans-serif'] = ['SimHei'] # 设置中文字体

mpl.rcParams['axes.unicode_minus'] = False

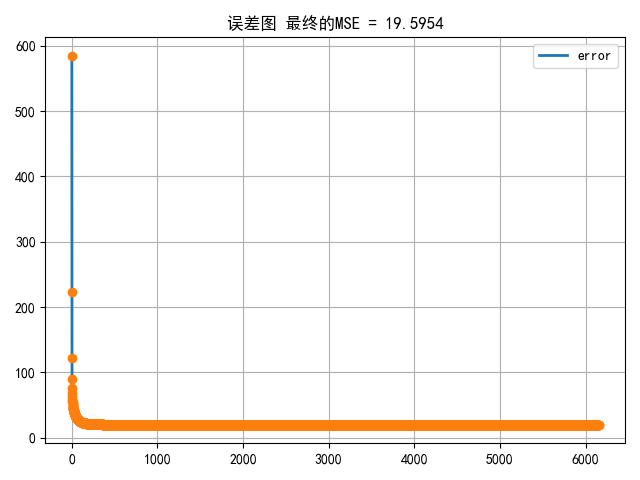

figure('误差图 最终的MSE = %.4f' % (train_error[1][-1]), [train_error[1], 'error']) # 绘制误差图

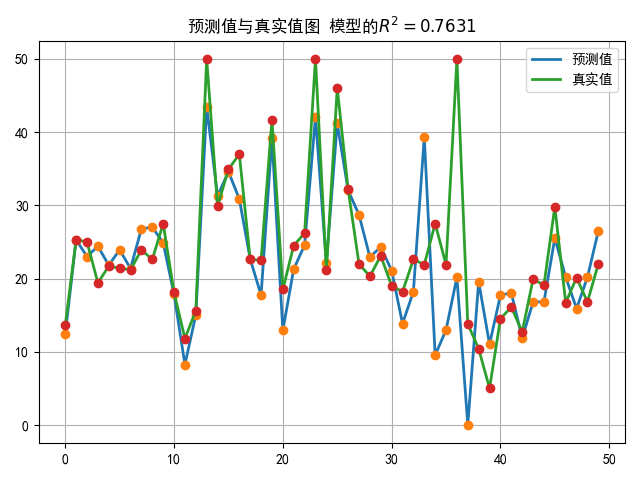

figure('预测值与真实值图 模型的' + r'$R^2=%.4f$' % (getR(lrdata[1], train_pre_result)), [predict_result, '预测值'],

[lrdata[3], '真实值']) # 绘制预测值与真实值图

plt.show()

print('线性回归的系数为:\n w = %s, \nb= %s' % (train_error[0][:-1], train_error[0][-1]))

实验结果:

(三)利用logistic回归模型进行心脏病预测

心脏病是人类健康的头号杀手。全世界1/3的人口死亡是因心脏病引起的,而我国,每年有几十万人死于心脏病。 所以,如果可以通过提取人体相关的体侧指标,通过数据挖掘的方式来分析不同特征对于心脏病的影响,对于预测和预防心脏病将起到至关重要的作用。本文将会通过真实的数据,通过Python搭建心脏病预测案例。

实验代码:

import numpy as np

import pandas as pd

from prettytable import PrettyTable # 用于计算混淆矩阵

import matplotlib.pyplot as plt

from pylab import mpl

def confusion(realy, outy):

mix = PrettyTable()

type = sorted(list(set(realy.T[0])), reverse=True)

mix.field_names = [' '] + ['预测:%d类' % si for si in type]

# 字典形式存储混淆矩阵数据

cmdict = {}

for jkj in type:

cmdict[jkj] = []

for hh in type:

hu = len(['0' for jj in range(len(realy)) if realy[jj][0] == jkj and outy[jj][0] == hh])

cmdict[jkj].append(hu)

# 输出表格

for fu in type:

mix.add_row(['真实:%d类' % fu] + cmdict[fu])

return mix

# 返回混淆矩阵用到的数据TP,TN,FP,FN

def getmatrix(realy, outy, possclass=1): # 默认类1 为正类

TP = len(['0' for jj in range(len(realy)) if realy[jj][0] == possclass and outy[jj][0] == possclass]) # 实际正预测正

TN = len(

['0' for jj in range(len(realy)) if realy[jj][0] == 1 - possclass and outy[jj][0] == 1 - possclass]) # 实际负预测负

FP = len(['0' for jj in range(len(realy)) if realy[jj][0] == 1 - possclass and outy[jj][0] == possclass]) # 实际负预测正

FN = len(['0' for jj in range(len(realy)) if realy[jj][0] == possclass and outy[jj][0] == 1 - possclass]) # 实际正预测负

# 假正率

FPR = FP / (FP + TN)

# 真正率

TPR = TP / (TP + FN)

return FPR, TPR

class LRReg:

def __init__(self, learn_rate=0.5, iter_times=40000, error=1e-9, cpn='L2'):

self.learn_rate = learn_rate

self.iter_times = iter_times

self.error = error

self.cpn = cpn

# w和b合为一个参数,也就是x最后加上一列全为1的数据。

def trans(self, xdata):

one1 = np.ones(len(xdata))

xta = np.append(xdata, one1.reshape(-1, 1), axis=1)

return xta

# 梯度下降法

def Gradient(self, xdata, ydata, func=trans):

xdata = func(self, xdata)

# 系数w,b的初始化

self.weights = np.zeros((len(xdata[0]), 1))

# 存储成本函数的值

cost_function = []

for i in range(self.iter_times):

# 得到回归的值

y_predict = np.dot(xdata, self.weights)

# Sigmoid函数的值

s_y_pre = 1 / (1 + np.exp(-y_predict))

# 计算最大似然的值

like = np.sum(np.dot(ydata.T, np.log(s_y_pre)) + np.dot((1 - ydata).T, np.log(1 - s_y_pre)))

# 正则化

if self.cpn == 'L2':

# 成本函数中添加系数的L2范数

l2norm = np.sum(0.5 * np.dot(self.weights.T, self.weights) / len(xdata))

cost = -like / len(xdata) + l2norm

grad_W = np.dot(xdata.T, (s_y_pre - ydata)) / len(xdata) + 0.9 * self.weights / len(xdata)

else:

cost = -like / (len(xdata))

grad_W = np.dot(xdata.T, (s_y_pre - ydata)) / len(xdata)

cost_function.append(cost)

print(cost, like)

# 训练提前结束

if len(cost_function) > 2:

if 0 <= cost_function[-1] - cost_function[-2] <= self.error:

break

# 更新

self.weights = self.weights - self.learn_rate * grad_W

return self.weights, cost_function

# 预测

def predict(self, xdata, func=trans, yuzhi=0.5):

pnum = np.dot(func(self, xdata), self.weights)

s_pnum = 1 / (1 + np.exp(-pnum))

latnum = [[1] if jj[0] >= yuzhi else [0] for jj in s_pnum]

return latnum

# 开始进行数据处理【没有缺失值】

def preprocess_data():

data = pd.read_csv(r'./Heart.csv')

normal = [1, 4, 5, 8, 10, 12, 11] # 标准化处理

one_hot = [3, 7, 13] # one_hot编码

binary = [14] # 原始类别为1的依然为1类,原始为2的变为0类

keylist = data.keys()

newexdata = pd.DataFrame()

for ikey in range(len(keylist)):

if ikey + 1 in normal:

newexdata[keylist[ikey]] = (data[keylist[ikey]] - data[keylist[ikey]].mean()) / data[keylist[ikey]].std()

elif ikey + 1 in binary:

newexdata[keylist[ikey]] = [1 if inum == 1 else 0 for inum in data[keylist[ikey]]]

elif ikey + 1 in one_hot:

newdata = pd.get_dummies(data[keylist[ikey]], prefix=keylist[ikey])

newexdata = pd.concat([newexdata, newdata], axis=1)

x_pre_data = newexdata.values[:, :-1]

y_data = newexdata.values[:, -1].reshape(-1, 1)

return x_pre_data, y_data

if __name__ == "__main__":

lr_re = LRReg()

H_Data = preprocess_data() # 最终的可用于算法的数据

lf = lr_re.Gradient(H_Data[0], H_Data[1])

print('系数为:\n', lr_re.weights)

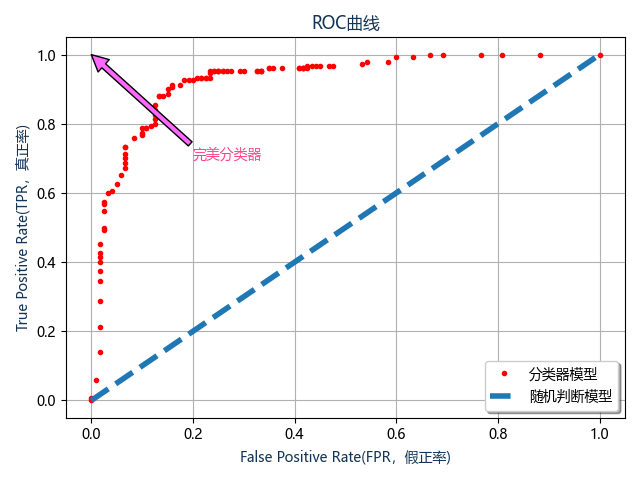

# 绘制ROC曲线

yuzi = np.linspace(0, 1, 101) # 从0到1定义不同的阈值

roc = [] # ROC 曲线数据

for yy in yuzi: # 开始遍历不同的阈值

fdatd = lr_re.predict(H_Data[0], yuzhi=yy)

if yy == 0.5:

print('阈值为%s时的混淆矩阵:\n' % yy, confusion(H_Data[1], fdatd))

roc.append(getmatrix(H_Data[1], fdatd))

fu = np.array(sorted(roc, key=lambda x: x[0])) # 首线是FPR按着从小到大排列

# 开始绘制ROC曲线图

mpl.rcParams['font.sans-serif'] = ['Microsoft Yahei'] # 作图显示中文

fig, ax1 = plt.subplots()

ax1.plot(list(fu[:, 0]), list(fu[:, 1]), '.', linewidth=4, color='r')

ax1.plot([0, 1], '--', linewidth=4)

ax1.grid('on')

ax1.legend(['分类器模型', '随机判断模型'], loc='lower right', shadow=True, fontsize='medium')

ax1.annotate('完美分类器', xy=(0, 1), xytext=(0.2, 0.7), color='#FF4589', arrowprops=dict(facecolor='#FF67FF'))

ax1.set_title('ROC曲线', color='#123456')

ax1.set_xlabel('False Positive Rate(FPR,假正率)', color='#123456')

ax1.set_ylabel('True Positive Rate(TPR,真正率)', color='#123456')

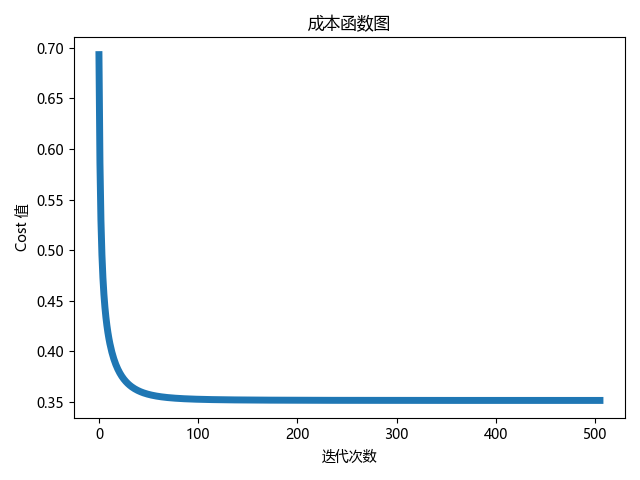

# 绘制成本函数图

fig, ax2 = plt.subplots()

ax2.plot(list(range(len(lf[1]))), lf[1], '-', linewidth=5)

ax2.set_title('成本函数图')

ax2.set_ylabel('Cost 值')

ax2.set_xlabel('迭代次数')

plt.show()

实验结果:

系数为:

[[ 0.22442019]

[ 0.66719841]

[ 0.07366912]

[ 0.60077063]

[-1.13520668]

[-0.32244956]

[-0.16243874]

[ 0.42651962]

[ 0.01357678]

[-0.23366492]

[ 0.49654308]

[-0.55760351]

[-0.22314746]

[-1.02066971]

[ 0.94635202]

[ 0.20900704]

[-0.94892758]

[ 0.20643148]]

阈值为0.5时的混淆矩阵:

+----------+----------+----------+

| | 预测:1类 | 预测:0类 |

+----------+----------+----------+

| 真实:1类 | 140 | 10 |

| 真实:0类 | 25 | 95 |

+----------+----------+----------+

(四)利用softmax回归进行莺尾花分类预测

softmax回归是logistic回归的推广,通过独热向量表示类别,使用交叉熵损失函数来学习最优的参数矩阵W,对样本进行多分类(对Iris数据集进行三分类)。

实验代码:

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from pylab import mpl

from prettytable import PrettyTable # 用于计算混淆矩阵

class LRReg:

def __init__(self, learn_rate=0.9, iter_times=40000, error=1e-17):

self.learn_rate = learn_rate

self.iter_times = iter_times

self.error = error

# w和b合为一个参数,也就是x最后加上一列全为1的数据

def trans(self, xdata):

one1 = np.ones(len(xdata))

xta = np.append(xdata, one1.reshape(-1, 1), axis=1)

return xta

# 梯度下降法

def Gradient(self, xdata, ydata, func=trans):

xdata = func(self, xdata)

# 系数w,b的初始化

self.weights = np.zeros((len(xdata[0]), len(ydata[0])))

# 存储成本函数的值

cost_function = []

for i in range(self.iter_times):

# 计算np.exp(X.W)的值

exp_xw = np.exp(np.dot(xdata, self.weights))

# 计算y_predict每一行的和值

sumrow = np.sum(exp_xw, axis=1).reshape(-1, 1)

# 计算除去和值得值

devi_sum = exp_xw / sumrow

# 计算减法

sub_y = ydata - devi_sum

# 得到梯度

grad_W = -1 / len(xdata) * np.dot(xdata.T, sub_y)

# 正则化,成本函数中添加系数的L2范数

l2norm = np.sum(0.5 * np.dot(self.weights.T, self.weights) / len(xdata))

last_grad_W = grad_W + 0.002 * self.weights / len(xdata)

# 计算最大似然的对数的值

likehood = np.sum(ydata * devi_sum)

cost = - likehood / len(xdata) + l2norm

cost_function.append(cost)

# 训练提前结束

if len(cost_function) > 2:

if 0 <= cost_function[-2] - cost_function[-1] <= self.error:

break

# 更新

self.weights = self.weights - self.learn_rate * last_grad_W

return self.weights, cost_function

# 预测

def predict(self, xdata, func=trans):

pnum = np.dot(func(self, xdata), self.weights)

# 选择每一行中最大的数的index

maxnumber = np.max(pnum, axis=1)

# 预测的类别

y_pre_type = []

for jj in range(len(maxnumber)):

fu = list(pnum[jj]).index(maxnumber[jj]) + 1

y_pre_type.append([fu])

return np.array(y_pre_type)

# 将独热编码的类别变为标识为1,2,3的类别

def transign(eydata):

ysign = []

for hh in eydata:

ysign.append([list(hh).index(1) + 1])

return np.array(ysign)

def confusion(realy, outy, method='AnFany'):

mix = PrettyTable()

type = sorted(list(set(realy.T[0])), reverse=True)

mix.field_names = [method] + ['预测:%d类' % si for si in type]

# 字典形式存储混淆矩阵数据

cmdict = {}

for jkj in type:

cmdict[jkj] = []

for hh in type:

hu = len(['0' for jj in range(len(realy)) if realy[jj][0] == jkj and outy[jj][0] == hh])

cmdict[jkj].append(hu)

# 输出表格

for fu in type:

mix.add_row(['真实:%d类' % fu] + cmdict[fu])

return mix

# setosa [1,0,0]

# versicolor [0,1,0]

# virginica [0,0,1]

def preprocess_data():

data = pd.read_csv(r'iris.csv')

xdata = data.iloc[:, 1:5].values # x值

handle_x_data = (xdata - np.mean(xdata, axis=0)) / np.std(xdata, axis=0) # x数据标准化

ydata = pd.get_dummies(data['Species']).values # y数据独热化

xydata = np.hstack((handle_x_data, ydata)) # 首先将x数据和y数据合在一起

np.random.shuffle(xydata) # 因为数据中类别比较集中,不易于训练,因此打乱数据

return xydata[:, :4], xydata[:, 4:]

if __name__ == '__main__':

lr_re = LRReg()

data = preprocess_data()

lf = lr_re.Gradient(data[0], data[1])

y_calss_pre = lr_re.predict(data[0])

print('系数:\n', lr_re.weights)

print('混淆矩阵:\n', confusion(transign(data[1]), y_calss_pre))

# 绘制成本函数图

mpl.rcParams['font.sans-serif'] = ['FangSong'] # 设置中文字体新宋体(作图显示中文)

mpl.rcParams['axes.unicode_minus'] = False

plt.plot(list(range(len(lf[1]))), lf[1], '-', linewidth=5)

plt.title('成本函数图')

plt.ylabel('Cost 值')

plt.xlabel('迭代次数')

plt.show()

实验结果:

系数:

[[-3.18259494 2.53486939 0.64772555]

[ 3.21960963 -0.39859444 -2.82101519]

[-7.12327144 -3.49716456 10.620436 ]

[-6.67192748 -2.51948539 9.19141287]

[ 0.16517529 8.35513963 -8.52031491]]

混淆矩阵:

+----------+----------+----------+----------+

| AnFany | 预测:3类 | 预测:2类 | 预测:1类 |

+----------+----------+----------+----------+

| 真实:3类 | 49 | 1 | 0 |

| 真实:2类 | 1 | 49 | 0 |

| 真实:1类 | 0 | 0 | 50 |

+----------+----------+----------+----------+

575

575

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言