目录

初始化

% Initialization

clear ; close all; clc1.WarmUpExercise()

function A = warmUpExercise()

A =eye(5);

endex1.m

%% ==================== Part 1: Basic Function ====================

% Complete warmUpExercise.m

fprintf('Running warmUpExercise ... \n');

fprintf('5x5 Identity Matrix: \n');

warmUpExercise()

fprintf('Program paused. Press enter to continue.\n');

pause;运行结果如下:

Running warmUpExercise ...

5x5 Identity Matrix:ans =

1 0 0 0 0

0 1 0 0 0

0 0 1 0 0

0 0 0 1 0

0 0 0 0 1Program paused. Press enter to continue.

2.单变量线性回归

2.1 绘制数据

function plotData(x, y)

%绘制x,y的散点图

plot(x,y,'rx','MarkerSize',10); %取值点样式为'rx'即红色×状点,大小为10号

ylabel('Profit in $10,000s'); %设置y轴标签

xlabel('Population of City in 10,000s'); %设置x轴标签

endex1.m

%% ======================= Part 2: Plotting =======================

fprintf('Plotting Data ...\n')

data = load('ex1data1.txt'); %将训练集数据导入

X = data(:, 1); y = data(:, 2); %X为训练集中的第一列,m*1矩阵

%y为训练集中的第二列,m*1矩阵

m = length(y); % 训练集长度

plotData(X, y);

fprintf('Program paused. Press enter to continue.\n');

pause;

运行结果如下:

2.2 梯度下降

2.2.1 更新方程

线性回归的目标是最小化代价函数;

其中h_θ(x)定义如下:

同时要同步更新θ值:

2.2.2 实施

X = [ones(m, 1), data(:,1)]; % 为X阵添加一列1,X是m*2矩阵

theta = zeros(2, 1); % 初始化合适的θ值

iterations = 1500; %迭代次数

alpha = 0.01; %学习率α初值2.2.3 计算代价函数

function J = computeCost(X, y, theta)

m = length(y); % 训练集大小

J = 0; %为J设定初值

h_x=X*theta; %h_x(θ)

J_error=(h_x-y).^2; %实际值与预估值的误差

M=1/(2*m);

J=M*sum(J_error); %代价函数2.2.4 梯度下降

function [theta, J_history] = gradientDescent(X, y, theta, alpha, num_iters)

m = length(y); % 训练集大小

J_history = zeros(num_iters, 1); % 定义一个维度为迭代次数*1的零矩阵

for iter = 1:num_iters %进入循环,循环次数为迭代次数

theta=theta-alpha*(X'*(X*theta-y))/m; %更新θ

J_history(iter) = computeCost(X, y, theta); %将每次迭代得到的J值存入矩阵中

end

endex1.m

X = [ones(m, 1), data(:,1)]; % X矩阵

theta = zeros(2, 1); % θ矩阵

iterations = 1500; % 迭代次数

alpha = 0.01;

% 学习率

fprintf('\nTesting the cost function ...\n')

J = computeCost(X, y, theta);

fprintf('With theta = [0 ; 0]\nCost computed = %f\n', J);

fprintf('Expected cost value (approx) 32.07\n'); %θ为初始值时,J值大小

J = computeCost(X, y, [-1 ; 2]);

fprintf('\nWith theta = [-1 ; 2]\nCost computed = %f\n', J);

fprintf('Expected cost value (approx) 54.24\n'); % 更改θ值,J值变化

fprintf('Program paused. Press enter to continue.\n');

pause;

fprintf('\nRunning Gradient Descent ...\n') % 运行梯度下降算法

theta = gradientDescent(X, y, theta, alpha, iterations); % 通过梯度下降法更新θ

fprintf('Theta found by gradient descent:\n');

fprintf('%f\n', theta);

fprintf('Expected theta values (approx)\n');

fprintf(' -3.6303\n 1.1664\n\n'); % 期望θ值为-3.6303;1.1664

hold on; % 维持散点图

plot(X(:,2), X*theta, '-') %绘制横坐标为X第二列数据,纵坐标为X*θ的直线图

legend('Training data', 'Linear regression') %曲线标签

hold off

predict1 = [1, 3.5] *theta;

fprintf('For population = 35,000, we predict a profit of %f\n',...

predict1*10000);

predict2 = [1, 7] * theta;

fprintf('For population = 70,000, we predict a profit of %f\n',...

predict2*10000);

fprintf('Program paused. Press enter to continue.\n');

pause;

运行结果如下:

2.3 调试

略

2.4 可视化代价函数

在二维平面上显现代价函数,以更好的理解

ex1.m

fprintf('Visualizing J(theta_0, theta_1) ...\n')

theta0_vals = linspace(-10, 10, 100); % 生成矢量(-10到10的1*100)

theta1_vals = linspace(-1, 4, 100); % 生成矢量(-1到4的1*100)

J_vals = zeros(length(theta0_vals), length(theta1_vals));% 初始化J_vals矩阵,100*100的零矩阵

for i = 1:length(theta0_vals)

for j = 1:length(theta1_vals) % 循环100*100次

t = [theta0_vals(i); theta1_vals(j)]; % t即为θ值,θ随着循环进行不断改变

J_vals(i,j) = computeCost(X, y, t); % J_vals矩阵更改为J值

end

end %最后应得到一个100*100的J_vals矩阵,矩阵中值为J值

J_vals = J_vals'; %转置

figure;

surf(theta0_vals, theta1_vals, J_vals) %绘制三维曲面图,z轴为矩阵

xlabel('\theta_0'); ylabel('\theta_1');

figure;

contour(theta0_vals, theta1_vals, J_vals, logspace(-2, 3, 20)) %绘制等高线

xlabel('\theta_0'); ylabel('\theta_1');

hold on;

plot(theta(1), theta(2), 'rx', 'MarkerSize', 10, 'LineWidth', 2); %标记θ最优解运行结果如下:

3.多变量线性回归

以俄勒冈州波特兰市房屋价格为例:

3.1 特征归一化

通常,房屋大小为卧室数量的上千倍,需要进行特征缩放

·从数据集中减去每个特征的平均值

·减去平均值后,将比例特征值除以标准差

function [X_norm, mu, sigma] = featureNormalize(X)

X_norm = X; % 不改变X原数据

mu = zeros(1, size(X, 2));

sigma = zeros(1, size(X, 2));

mu=mean(X); % 均值

sigma=std(X); % 标准差

X_norm=(X_norm-mu)./sigma % 归一化

end3.2 梯度下降

·实现具有多变量的线性回归代价函数以及梯度回归。

·使用Size(X,2)可以找出数据集中存在多少特性。

·在多元情况下,可使用以下向量化形式表示:

因单变量线性回归时使用了向量化算法,因此多变量线性回归的代价函数以及梯度下降代码不变

3.2.1 选择学习率

梯度下降代码如下:

fprintf('Running gradient descent ...\n');

alpha = 1.2; % 学习率

num_iters = 400; % 迭代次数

theta = zeros(3, 1);

[theta, J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters);

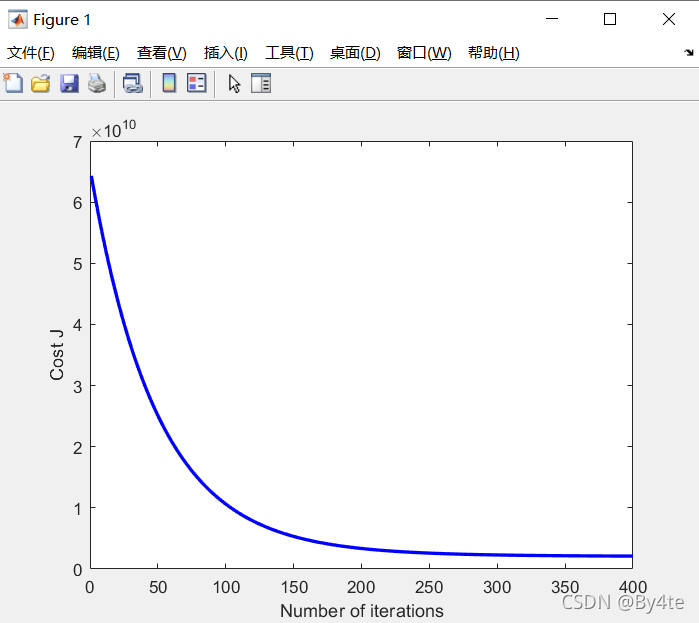

figure;

plot(1:numel(J_history), J_history, '-b', 'LineWidth', 2);

xlabel('Number of iterations');

ylabel('Cost J'); % 代价函数图像

fprintf('Theta computed from gradient descent: \n');

fprintf(' %f \n', theta);

fprintf('\n');

predict_x=[1650,3]; % 预测房价

predict_x=(predict_x-mu)./sigma;

price=[1,predict_x]*theta;

fprintf(['Predicted price of a 1650 sq-ft, 3 br house ' ...

'(using gradient descent):\n $%f\n'], price);

fprintf('Program paused. Press enter to continue.\n');

pause;

3.3 正规方程

线性回归封闭形式解如下:

使用该公式时无需进行特征缩放,将直接得到精确解

代码如下:

function [theta] = normalEqn(X, y)

theta = zeros(size(X, 2), 1);

theta=pinv(X'*X)*X'*y

end

通过正规方程找到的θ与梯度下降找到的θ进行预测的结果相同

ex1_multi.m代码如下:

clear ; close all; clc

fprintf('Loading data ...\n');

data = load('ex1data2.txt');

X = data(:, 1:2);

y = data(:, 3);

m = length(y);

% Print out some data points

fprintf('First 10 examples from the dataset: \n');

fprintf(' x = [%.0f %.0f], y = %.0f \n', [X(1:10,:) y(1:10,:)]');

fprintf('Program paused. Press enter to continue.\n');

pause;

fprintf('Normalizing Features ...\n');

[X mu sigma] = featureNormalize(X);

X = [ones(m, 1) X];

fprintf('Running gradient descent ...\n');

alpha = 1.2;

num_iters = 400;

theta = zeros(3, 1);

[theta, J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters);

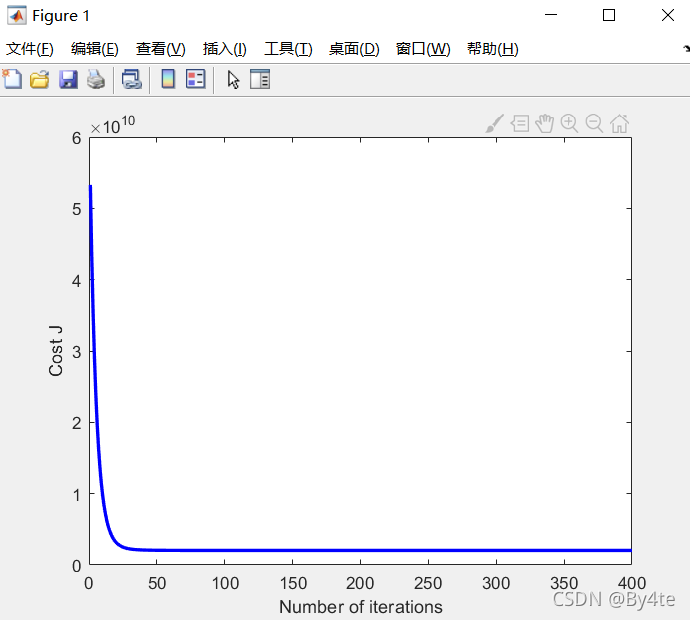

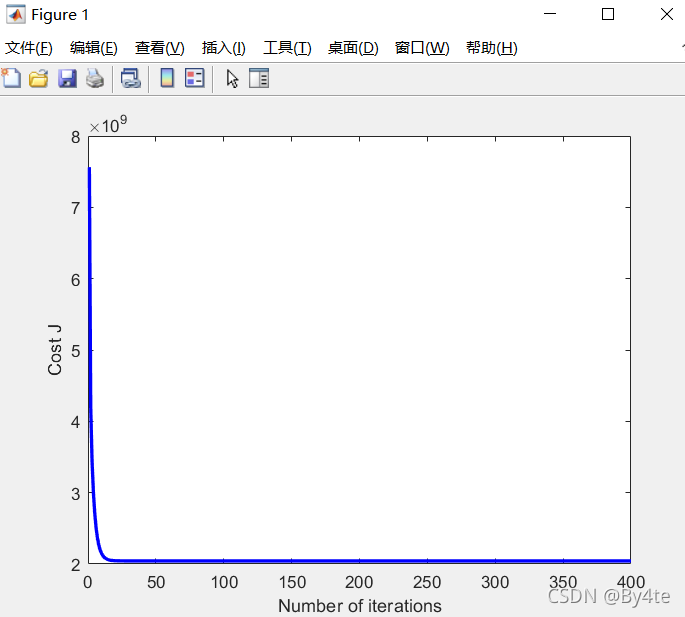

figure;

plot(1:numel(J_history), J_history, '-b', 'LineWidth', 2);

xlabel('Number of iterations');

ylabel('Cost J');

fprintf('Theta computed from gradient descent: \n');

fprintf(' %f \n', theta);

fprintf('\n');

predict_x=[1650,3];

predict_x=(predict_x-mu)./sigma;

price=[1,predict_x]*theta;

fprintf(['Predicted price of a 1650 sq-ft, 3 br house ' ...

'(using gradient descent):\n $%f\n'], price);

fprintf('Program paused. Press enter to continue.\n');

pause;

fprintf('Solving with normal equations...\n');

data = csvread('ex1data2.txt');

X = data(:, 1:2);

y = data(:, 3);

m = length(y);

X = [ones(m, 1) X];

theta = normalEqn(X, y);

fprintf('Theta computed from the normal equations: \n');

fprintf(' %f \n', theta);

fprintf('\n');

price=[1,1650,3]*theta;

fprintf(['Predicted price of a 1650 sq-ft, 3 br house ' ...

'(using normal equations):\n $%f\n'], price);

结果如下:

Loading data ...

First 10 examples from the dataset:

x = [2104 3], y = 399900

x = [1600 3], y = 329900

x = [2400 3], y = 369000

x = [1416 2], y = 232000

x = [3000 4], y = 539900

x = [1985 4], y = 299900

x = [1534 3], y = 314900

x = [1427 3], y = 198999

x = [1380 3], y = 212000

x = [1494 3], y = 242500

Program paused. Press enter to continue.

Normalizing Features ...

Running gradient descent ...

Theta computed from gradient descent:

340412.659574

110631.050279

-6649.474271Predicted price of a 1650 sq-ft, 3 br house (using gradient descent):

$293081.464335

Program paused. Press enter to continue.

Solving with normal equations...

Theta computed from the normal equations:

89597.909544

139.210674

-8738.019113Predicted price of a 1650 sq-ft, 3 br house (using normal equations):

$293081.464335

3330

3330

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言