先声明,本博客为个人作业不一定为标准答案,仅供参考

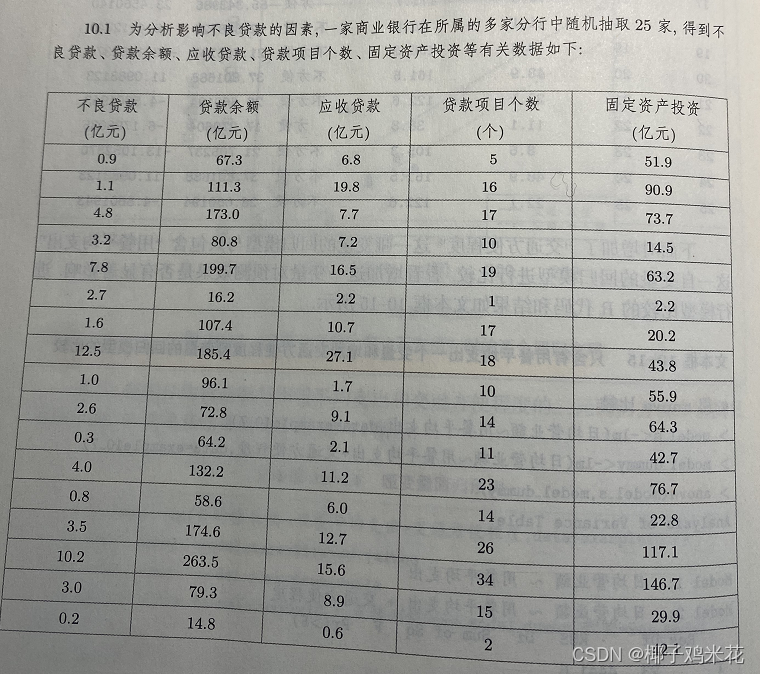

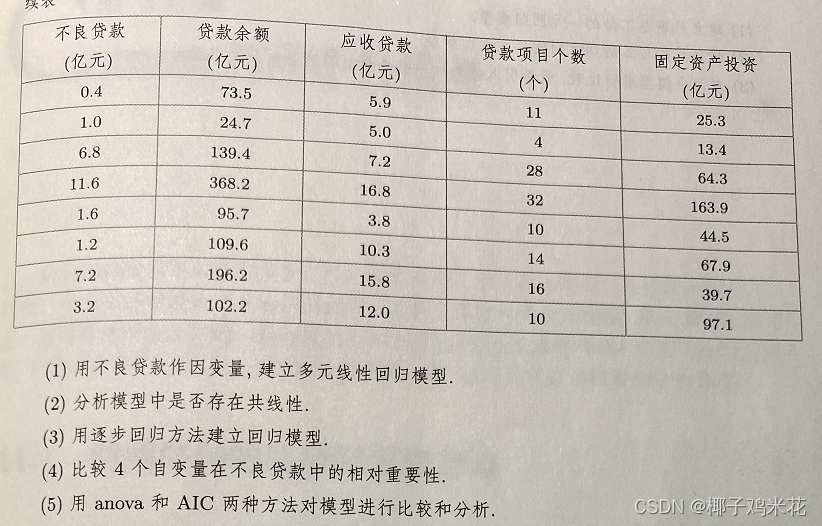

10.1 题目如下

(1)

> example10_1<-read.csv("D:/作业/统计学R/《统计学—基于R》(第4版)—例题和习题数据(公开资源)/exercise/chap10/exercise10_1.csv")

> model1<-lm(不良贷款~贷款余额+应收贷款+贷款项目个数+固定资产投资,data=example10_1)

> summary(model1)

Call:

lm(formula = 不良贷款 ~ 贷款余额 + 应收贷款 + 贷款项目个数 +

固定资产投资, data = example10_1)

Residuals:

Min 1Q Median 3Q Max

-2.9198 -0.9507 -0.2880 1.0334 3.1037

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -1.02164 0.78237 -1.306 0.20643

贷款余额 0.04004 0.01043 3.837 0.00103 **

应收贷款 0.14803 0.07879 1.879 0.07494 .

贷款项目个数 0.01453 0.08303 0.175 0.86285

固定资产投资 -0.02919 0.01507 -1.937 0.06703 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.779 on 20 degrees of freedom

Multiple R-squared: 0.7976, Adjusted R-squared: 0.7571

F-statistic: 19.7 on 4 and 20 DF, p-value: 1.035e-06

(2)

> library(car)

> vif(model1)

贷款余额 应收贷款 贷款项目个数 固定资产投资

5.330807 1.889860 3.834823 2.781220 VIF最大值为5.330807<10,显示模型的共线性在可容忍范围内

(3)

> model2<-step(model1)

Start: AIC=33.22

不良贷款 ~ 贷款余额 + 应收贷款 + 贷款项目个数 + 固定资产投资

Df Sum of Sq RSS AIC

- 贷款项目个数 1 0.097 63.376 31.255

<none> 63.279 33.217

- 应收贷款 1 11.168 74.447 35.280

- 固定资产投资 1 11.868 75.147 35.514

- 贷款余额 1 46.594 109.873 45.011

Step: AIC=31.26

不良贷款 ~ 贷款余额 + 应收贷款 + 固定资产投资

Df Sum of Sq RSS AIC

<none> 63.376 31.255

- 应收贷款 1 11.333 74.709 33.368

- 固定资产投资 1 12.147 75.523 33.639

- 贷款余额 1 69.939 133.315 47.846逐步回归显示,应剔除贷款项目个数这个自变量来建立模型

逐步回归建模结果如下:

> summary(model2)

Call:

lm(formula = 不良贷款 ~ 贷款余额 + 应收贷款 + 固定资产投资, data = example10_1)

Residuals:

Min 1Q Median 3Q Max

-2.8531 -0.8766 -0.3685 0.9586 3.0772

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.971605 0.711240 -1.366 0.1864

贷款余额 0.041039 0.008525 4.814 9.31e-05 ***

应收贷款 0.148858 0.076817 1.938 0.0662 .

固定资产投资 -0.028502 0.014206 -2.006 0.0579 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.737 on 21 degrees of freedom

Multiple R-squared: 0.7973, Adjusted R-squared: 0.7683

F-statistic: 27.53 on 3 and 21 DF, p-value: 1.802e-07(4)

> library(lm.beta)

> model1.beta<-lm.beta(model1)

> summary(model1.beta)

Call:

lm(formula = 不良贷款 ~ 贷款余额 + 应收贷款 + 贷款项目个数 +

固定资产投资, data = example10_1)

Residuals:

Min 1Q Median 3Q Max

-2.9198 -0.9507 -0.2880 1.0334 3.1037

Coefficients:

Estimate Standardized Std. Error t value Pr(>|t|)

(Intercept) -1.02164 0.00000 0.78237 -1.306 0.20643

贷款余额 0.04004 0.89131 0.01043 3.837 0.00103 **

应收贷款 0.14803 0.25982 0.07879 1.879 0.07494 .

贷款项目个数 0.01453 0.03447 0.08303 0.175 0.86285

固定资产投资 -0.02919 -0.32492 0.01507 -1.937 0.06703 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.779 on 20 degrees of freedom

Multiple R-squared: 0.7976, Adjusted R-squared: 0.7571

F-statistic: 19.7 on 4 and 20 DF, p-value: 1.035e-06

由标准化回归系数可知各个自变量的相对重要性依次为:贷款余额>固定资产投资>应收贷款>贷款项目个数

(5)

Anova方法:

> anova(model2,model1)

Analysis of Variance Table

Model 1: 不良贷款 ~ 贷款余额 + 应收贷款 + 固定资产投资

Model 2: 不良贷款 ~ 贷款余额 + 应收贷款 + 贷款项目个数 + 固定资产投资

Res.Df RSS Df Sum of Sq F Pr(>F)

1 21 63.376

2 20 63.279 1 0.096877 0.0306 0.8629p=0.8629>0.05,不拒绝H0,两个模型没有显著差异,从回归模型的简约原则看,选择逐步回归保留的3个自变量建立模型比较合适

AIC方法:

> AIC(model2,model1)

df AIC

model2 5 104.2022

model1 6 106.1639AIC值越小模型越好,因此选择逐步回归模型的结果更好

10.2 题目如下

多元线性回归模型结果如下:

> model1<-lm(disp~mpg+cyl+drat+hp+wt,data=mtcars)

> summary(model1)

Call:

lm(formula = disp ~ mpg + cyl + drat + hp + wt, data = mtcars)

Residuals:

Min 1Q Median 3Q Max

-72.393 -26.432 4.697 30.160 59.418

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -233.6420 160.8590 -1.452 0.158335

mpg 3.2249 3.1044 1.039 0.308454

cyl 30.3927 10.5133 2.891 0.007658 **

drat -13.5209 22.5147 -0.601 0.553348

hp 0.3208 0.2187 1.467 0.154479

wt 66.2331 16.1055 4.112 0.000348 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 40.99 on 26 degrees of freedom

Multiple R-squared: 0.9082, Adjusted R-squared: 0.8906

F-statistic: 51.47 on 5 and 26 DF, p-value: 1.157e-12回归结果显示,5个自变量中,只有cyl和wt显著,其余均不显著,模型可能存在多重共线性

VIF结果如下:

> library(car)

> vif(model1)

mpg cyl drat hp wt

6.457610 6.503052 2.673212 4.149207 4.580898 mpg和cyl的VIF较大,可能需要进一步做逐步回归

逐步回归过程如下:

> model2<-step(model1)

Start: AIC=243.02

disp ~ mpg + cyl + drat + hp + wt

Df Sum of Sq RSS AIC

- drat 1 606.1 44300 241.46

- mpg 1 1813.5 45507 242.32

<none> 43694 243.01

- hp 1 3614.6 47308 243.56

- cyl 1 14044.6 57738 249.93

- wt 1 28421.4 72115 257.05

Step: AIC=241.46

disp ~ mpg + cyl + hp + wt

Df Sum of Sq RSS AIC

- mpg 1 1605 45905 240.59

<none> 44300 241.46

- hp 1 3011 47310 241.56

- cyl 1 20694 64993 251.72

- wt 1 32903 77202 257.23

Step: AIC=240.59

disp ~ cyl + hp + wt

Df Sum of Sq RSS AIC

- hp 1 2078 47983 240.01

<none> 45905 240.59

- cyl 1 19108 65012 249.73

- wt 1 40338 86243 258.77

Step: AIC=240.01

disp ~ cyl + wt

Df Sum of Sq RSS AIC

<none> 47983 240.01

- wt 1 40748 88731 257.68

- cyl 1 52726 100709 261.74逐步回归结果显示,只保留了cyl和wt两个自变量,其余的均被剔除

逐步回归建模结果如下:

> summary(model2)

Call:

lm(formula = disp ~ cyl + wt, data = mtcars)

Residuals:

Min 1Q Median 3Q Max

-72.888 -20.507 2.902 31.644 64.701

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -190.21 27.17 -7.001 1.07e-07 ***

cyl 37.09 6.57 5.645 4.23e-06 ***

wt 59.51 11.99 4.963 2.81e-05 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 40.68 on 29 degrees of freedom

Multiple R-squared: 0.8992, Adjusted R-squared: 0.8923

F-statistic: 129.4 on 2 and 29 DF, p-value: 3.532e-15用Anova方法比较模型:

> anova(model2,model1)

Analysis of Variance Table

Model 1: disp ~ cyl + wt

Model 2: disp ~ mpg + cyl + drat + hp + wt

Res.Df RSS Df Sum of Sq F Pr(>F)

1 29 47983

2 26 43694 3 4289.3 0.8508 0.4788用AIC方法比较模型:

> AIC(model2,model1)

df AIC

model2 4 332.8237

model1 7 335.8272模型比较显示,两个模型差异不显著,逐步回归模型的AIC值小于含有5个自变量的模型,故选用逐步回归模型较好

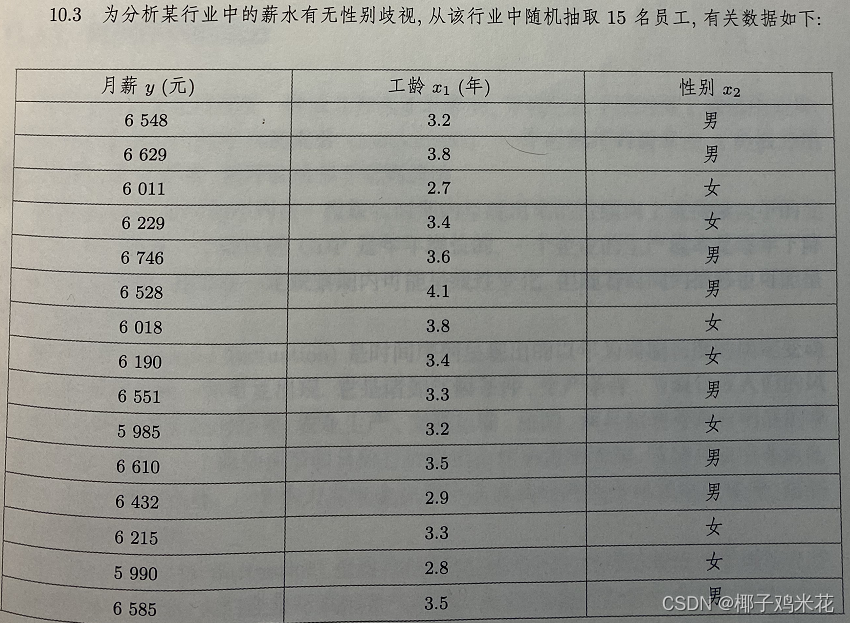

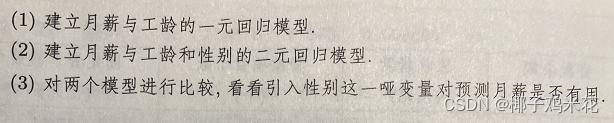

10.3 题目如下

(1)

> example10_3<-read.csv("D:/作业/统计学R/《统计学—基于R》(第4版)—例题和习题数据(公开资源)/exercise/chap10/exercise10_3.csv")

> model1<-lm(月薪~工龄,data=example10_3)

> summary(model1)

Call:

lm(formula = 月薪 ~ 工龄, data = example10_3)

Residuals:

Min 1Q Median 3Q Max

-474.90 -152.54 -63.05 218.46 318.53

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 5249.7 587.1 8.941 6.48e-07 ***

工龄 327.2 173.3 1.887 0.0817 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 248.4 on 13 degrees of freedom

Multiple R-squared: 0.2151, Adjusted R-squared: 0.1547

F-statistic: 3.562 on 1 and 13 DF, p-value: 0.08165回归结果显示,模型不显著,R2=21.51%,模型的拟合程度较差

(2)

引入哑变量,建立二元回归模型

> model2<-lm(月薪~工龄+性别,data=example10_3)

> summary(model2)

Call:

lm(formula = 月薪 ~ 工龄 + 性别, data = example10_3)

Residuals:

Min 1Q Median 3Q Max

-136.697 -67.380 1.351 54.888 154.863

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6190.74 253.71 24.401 1.35e-11 ***

工龄 111.22 72.08 1.543 0.149

性别女 -458.68 53.46 -8.580 1.82e-06 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 96.79 on 12 degrees of freedom

Multiple R-squared: 0.89, Adjusted R-squared: 0.8717

F-statistic: 48.54 on 2 and 12 DF, p-value: 1.773e-06引入哑变量后,模型显著,Ra2=87.17%,模型的拟合程度大幅提高,表示有必要引入哑变量

(3)

用Anova方法比较模型:

> anova(model2,model1)

Analysis of Variance Table

Model 1: 月薪 ~ 工龄 + 性别

Model 2: 月薪 ~ 工龄

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 112423

2 13 802137 -1 -689714 73.62 1.823e-06 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1用AIC方法比较模型:

> AIC(model2,model1)

df AIC

model2 4 184.3978

model1 3 211.8729比较结果显示,引入性别哑变量模型比不引入性别哑变量模型差异显著,AIC也较小,表示有必要引入哑变量

本次记录就到这~~

1282

1282

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言