对 SPY 和 IWM 之间的日内均值回归配对策略进行回测

在本文中,我们将讨论我们的第一个日内交易策略。它将使用经典的交易理念,即“交易对”。在这种情况下,我们将利用两只交易所交易基金(ETF),SPY和IWM,它们在纽约证券交易所 (NYSE) 交易,并分别试图代表美国股票市场指数,即标准普尔 500 指数和罗素 2000 指数。

该策略通过做多一只 ETF 并做空一定数量的 ETF 来大致在 ETF 对之间创建“价差”。多头与空头的比率可以通过多种方式定义,例如利用统计协整时间序列技术。在这种情况下,我们将通过滚动线性回归计算 SPY 和 IWM 之间的对冲比率。这将使我们能够在 SPY 和 IWM 之间创建“价差”,并将其标准化为z 分数。当 z 分数超过某些阈值时,将生成交易信号,因为我们相信价差将恢复到平均值。

该策略的原理是 SPY 和 IWM 大致描述了相同的情况,即一组大型和小型美国公司的经济状况。前提是,如果采用价格差,那么它应该是均值回归的,因为虽然“局部”(时间)事件可能会分别影响 S&P500 或 Russell 2000 指数(例如小型/大型股差异、重新平衡日期或大宗交易),但两者的长期价格序列可能会协整。

策略

该策略按以下步骤进行:

- 数据- SPY 和 IWM 的 1 分钟条形图是从 2007 年 4 月到 2014 年 2 月获得的。

- 处理- 数据正确对齐,缺失的条形被相互丢弃。

- 价差- 两只 ETF 之间的对冲比率是通过滚动线性回归计算得出的。这被定义为𝛽回归系数使用*回溯窗口,*该窗口向前移动 1 条并重新计算回归系数。因此对冲比率𝛽我,用于酒吧𝑏我跨点计算𝑏我−1−钾到𝑏我−1回顾钾酒吧。

- Z 分数- 点差的标准分数以通常的方式计算。这意味着减去点差的(样本)平均值并除以点差的(样本)标准差。这样做的理由是使阈值参数更易于理解,因为 z 分数是无量纲量。我们故意在计算中引入了前瞻偏差,以显示它有多么微妙。试着留意它!

- 交易- 当负 z 分数低于预定(或优化后)阈值时,会产生多头信号,而空头信号则相反。当绝对 z 分数低于另一个阈值时,会产生退出信号。对于此策略,我(有点随意地)选择了绝对进入阈值|是|=2退出门槛为|是|=1. 假设价差呈现均值回归行为,则有望捕捉到这种关系并提供积极的表现。

深入了解该策略的最佳方式可能是实际实施它。以下部分描述了用于实施此均值回归策略的完整 Python 代码(单个文件)。为了帮助理解,我对代码进行了大量的注释。

Python 实现

与所有 Python/pandas 教程一样,需要按照本教程中的说明设置 Python 研究环境。设置完成后,第一项任务是导入必要的 Python 库。此回测需要matplotlib和pandas 。

我使用的具体库版本如下:

- Python - 3.8

- NumPy-1.20

- 熊猫-1.3

- matplotlib-3.4

- 统计模型-0.12

让我们继续导入库:

# mr_spy_iwm.py

import matplotlib.pyplot as plt

import numpy as np

import os, os.path

import pandas as pd

import seaborn as sns

import statsmodels.api as sm

from statsmodels.regression.rolling import RollingOLS

sns.set_style("darkgrid")

以下函数create_pairs_dataframe导入两个包含两个符号的日内条形图的 CSV 文件。在我们的例子中,这两个符号是 SPY 和 IWM。然后,它创建一个单独的数据框pairs,使用两个原始文件的索引。由于它们的时间戳可能由于错过交易和错误而不同,因此这可以保证我们将获得匹配的数据。这是使用 pandas 等数据分析库的主要好处之一。“样板”代码以非常高效的方式为我们处理。

# mr_spy_iwm.py

def create_pairs_dataframe(datadir, symbols):

"""

Creates a pandas DataFrame containing the closing price

of a pair of symbols based on CSV files containing a datetime

stamp and OHLCV data.

Parameters

----------

datadir : `str`

Directory location of CSV files containing OHLCV intraday data.

symbols : `tup`

Tuple containing ticker symbols as `str`.

Returns

-------

pairs : `pd.DataFrame`

A DataFrame containing Close price for SPY and IWM. Index is a

Datetime object.

"""

# Open the individual CSV files and read into pandas DataFrames

# using the first column as an index and col_names as the headers

print("Importing CSV data...")

col_names = ['datetime','open','high','low','close', 'volume', 'na']

sym1 = pd.read_csv(

os.path.join(datadir, '%s.csv' % symbols[0]),

header=0,

index_col=0,

names=col_names

)

sym2 = pd.read_csv(

os.path.join(datadir, '%s.csv' % symbols[1]),

header=0,

index_col=0,

names=col_names

)

# Create a pandas DataFrame with the close prices of each symbol

# correctly aligned and dropping missing entries

print("Constructing dual matrix for %s and %s..." % symbols)

pairs = pd.DataFrame(index=sym1.index)

pairs['%s_close' % symbols[0].lower()] = sym1['close']

pairs['%s_close' % symbols[1].lower()] = sym2['close']

pairs.index = pd.to_datetime(pairs.index)

pairs = pairs.dropna()

return pairs

下一步是执行 SPY 和 IWM 之间的滚动线性回归。在这种情况下,IWM 是预测因子(“x”),SPY 是响应(“y”)。我已设置 100 条的默认回溯窗口。如上所述,这是策略的一个参数。为了使策略被视为稳健,我们理想情况下希望将回报概况(或其他绩效衡量标准)视为回溯期的凸函数。因此,在代码的后期阶段,我们将通过在一定范围内改变回溯期来进行敏感性分析。

在SPY-IWM 的线性回归模型中计算出滚动贝塔pairs系数后,我们将其添加到DataFrame 中并删除空行。这构成了第一组与回溯大小相等的条形图,作为修剪指标。然后,我们创建两个 ETF 的价差,作为 SPY 和−𝛽我IWM 单位。显然,这不是现实情况,因为我们采用的是 IWM 的分数,这在实际实施中是不可能的。

最后,我们创建价差的 z 分数,该分数通过减去价差的平均值并用价差的标准差进行归一化来计算。请注意,这里出现了一个相当微妙的前瞻偏差。我故意把它留在代码中,因为我想强调在研究中犯这样的错误是多么容易。平均值和标准差是针对整个价差时间序列计算的。如果这是为了反映真实的历史准确性,那么这些信息将无法获得,因为它隐含地利用了未来信息。因此,我们应该使用滚动平均值和标准差来计算 z 分数。

# mr_spy_iwm.py

def calculate_spread_zscore(pairs, symbols, lookback=100):

"""

Creates a hedge ratio between the two symbols by calculating

a rolling linear regression with a defined lookback period. This

is then used to create a z-score of the 'spread' between the two

symbols based on a linear combination of the two.

Parameters

----------

pairs : `pd.DataFrame`

A DataFrame containing Close price for SPY and IWM. Index is a

Datetime object.

symbols : `tup`

Tuple containing ticker symbols as `str`.

lookback : `int`, optional (default: 100)

Lookback preiod for rolling linear regression.

Returns

-------

pairs : 'pd.DataFrame'

Updated DataFrame containing the spread and z score between

the two symbols based on the rolling linear regression.

"""

# Use the statsmodels Rolling Ordinary Least Squares method to fit

# a rolling linear regression between the two closing price time series

print("Fitting the rolling Linear Regression...")

model = RollingOLS(

endog=pairs['%s_close' % symbols[0].lower()],

exog=sm.add_constant(pairs['%s_close' % symbols[1].lower()]),

window=lookback

)

rres = model.fit()

params = rres.params.copy()

# Construct the hedge ratio and eliminate the first

# lookback-length empty/NaN period

pairs['hedge_ratio'] = params['iwm_close']

pairs.dropna(inplace=True)

# Create the spread and then a z-score of the spread

print("Creating the spread/zscore columns...")

pairs['spread'] = (

pairs['spy_close'] - pairs['hedge_ratio']*pairs['iwm_close']

)

pairs['zscore'] = (

pairs['spread'] - np.mean(pairs['spread']))/np.std(pairs['spread']

)

return pairs

交易信号create_long_short_market_signals已创建。这些信号通过以下方式计算:当 z 分数负向超过负 z 分数时做多价差,当 z 分数正向超过正 z 分数时做空价差。当 z 分数的绝对值小于或等于另一个(幅度较小的)阈值时,发出退出信号。

为了实现这种情况,必须知道每个条形图的策略是“进入”市场还是“退出”市场。long_market和short_market是两个变量,用于跟踪多头和空头市场头寸。不幸的是,与矢量化方法相比,以迭代方式编码要简单得多,因此计算速度很慢。尽管 1 分钟的条形图需要每个 CSV 文件约 700,000 个数据点,但在我的旧台式机上计算速度仍然相对较快!

要迭代 pandas DataFrame(诚然这不是一个常见操作),必须使用该iterrows方法,该方法提供了一个可以迭代的生成器:

# mr_spy_iwm.py

def create_long_short_market_signals(

pairs, symbols, z_entry_threshold=2.0, z_exit_threshold=1.0

):

"""

Create the entry/exit signals based on the exceeding of z_entry_threshold

for entering a position and falling below z_exit_threshold for exiting

a position.

Parameters

----------

pairs : `pd.DataFrame`

Updated DataFrame containing the close price, spread and z score

between the two symbols.

symbols : `tup`

Tuple containing ticker symbols as `str`.

z_entry_threshold : `float`, optional (default:2.0)

Z Score threshold for market entry.

z_exit_threshold : `float`, optional (default:1.0)

Z Score threshold for market exit.

Returns

-------

pairs : `pd.DataFrame`

Updated DataFrame containing long, short and exit signals.

"""

# Calculate when to be long, short and when to exit

pairs['longs'] = (pairs['zscore'] <= -z_entry_threshold)*1.0

pairs['shorts'] = (pairs['zscore'] >= z_entry_threshold)*1.0

pairs['exits'] = (np.abs(pairs['zscore']) <= z_exit_threshold)*1.0

# These signals are needed because we need to propagate a

# position forward, i.e. we need to stay long if the zscore

# threshold is less than z_entry_threshold by still greater

# than z_exit_threshold, and vice versa for shorts.

pairs['long_market'] = 0.0

pairs['short_market'] = 0.0

# These variables track whether to be long or short while

# iterating through the bars

long_market = 0

short_market = 0

# Calculates when to actually be "in" the market, i.e. to have a

# long or short position, as well as when not to be.

# Since this is using iterrows to loop over a dataframe, it will

# be significantly less efficient than a vectorised operation,

# i.e. slow!

print("Calculating when to be in the market (long and short)...")

for i, b in enumerate(pairs.iterrows()):

# Calculate longs

if b[1]['longs'] == 1.0:

long_market = 1

# Calculate shorts

if b[1]['shorts'] == 1.0:

short_market = 1

# Calculate exists

if b[1]['exits'] == 1.0:

long_market = 0

short_market = 0

# This directly assigns a 1 or 0 to the long_market/short_market

# columns, such that the strategy knows when to actually stay in!

pairs.iloc[i]['long_market'] = long_market

pairs.iloc[i]['short_market'] = short_market

return pairs

在此阶段,我们已更新pairs以包含实际的多头/空头信号,这使我们能够确定是否需要进入市场。现在我们需要创建一个投资组合来跟踪头寸的市场价值。第一个任务是创建一个positions结合多头和空头信号的列。这将包含来自(1,0,−1), 和1代表多头/市场仓位,0表示没有头寸(应该退出)并且−1表示空头/市场仓位。sym1和sym2列表示每根柱线收盘时 SPY 和 IWM 仓位的市场价值。

创建 ETF 市场价值后,我们会将它们相加,以在每条柱状图末尾得出总市场价值。然后,pct_change该 Series 对象的方法会将其转换为回报流。后续代码行会清除不良条目(NaN 和 inf 元素),最后计算完整的权益曲线。

# mr_spy_iwm.py

def create_portfolio_returns(pairs, symbols):

"""

Creates a portfolio pandas DataFrame which keeps track of

the account equity and ultimately generates an equity curve.

This can be used to generate drawdown and risk/reward ratios.

Parameters

----------

pairs : `pd.DataFrame`

Updated DataFrame containing the close price, spread and z score

between the two symbols and the long, short and exit signals.

symbols : `tup`

Tuple containing ticker symbols as `str`.

Returns

-------

portfolio : 'pd.DataFrame'

A DataFrame with datetime index from the pairs DataFrame, positions,

total market value and returns.

"""

# Convenience variables for symbols

sym1 = symbols[0].lower()

sym2 = symbols[1].lower()

# Construct the portfolio object with positions information

# Note the minuses to keep track of shorts!

print("Constructing a portfolio...")

portfolio = pd.DataFrame(index=pairs.index)

portfolio['positions'] = pairs['long_market'] - pairs['short_market']

portfolio[sym1] = -1.0 * pairs['%s_close' % sym1] * portfolio['positions']

portfolio[sym2] = pairs['%s_close' % sym2] * portfolio['positions']

portfolio['total'] = portfolio[sym1] + portfolio[sym2]

# Construct a percentage returns stream and eliminate all

# of the NaN and -inf/+inf cells

print("Constructing the equity curve...")

portfolio['returns'] = portfolio['total'].pct_change()

portfolio['returns'].fillna(0.0, inplace=True)

portfolio['returns'].replace([np.inf, -np.inf], 0.0, inplace=True)

portfolio['returns'].replace(-1.0, 0.0, inplace=True)

# Calculate the full equity curve

portfolio['returns'] = (portfolio['returns'] + 1.0).cumprod()

return portfolio

该__main__函数将所有内容整合在一起。盘中 CSV 文件位于路径中datadir。请确保修改以下代码以指向您的特定目录。

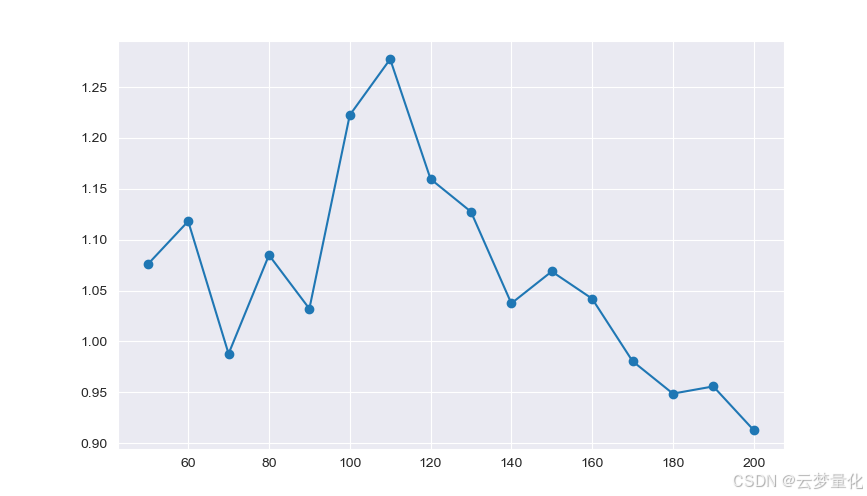

为了确定策略对回溯期的敏感度,有必要计算一系列回溯的绩效指标。我选择了投资组合的最终总回报率作为绩效衡量标准,回溯范围为[50,200]以 10 为增量。您可以在以下代码中看到,前面的函数被包装在for这个范围内的循环中,其他阈值保持不变。最后一项任务是使用 matplotlib 创建回顾与回报的折线图:

# mr_spy_iwm.py

if __name__ == "__main__":

datadir = '/your/path/to/data/' # Change this to reflect your data path!

symbols = ('SPY', 'IWM')

lookbacks = range(50, 210, 10)

returns = []

# Adjust lookback period from 50 to 200 in increments

# of 10 in order to produce sensitivities

for lb in lookbacks:

print("Calculating lookback=%s..." % lb)

pairs = create_pairs_dataframe(datadir, symbols)

pairs = calculate_spread_zscore(pairs, symbols, lookback=lb)

pairs = create_long_short_market_signals(

pairs, symbols, z_entry_threshold=2.0, z_exit_threshold=1.0

)

portfolio = create_portfolio_returns(pairs, symbols)

returns.append(portfolio.iloc[-1]['returns'])

print("Plot the lookback-performance scatterchart...")

plt.plot(lookbacks, returns, '-o')

plt.show()

现在可以看到回溯期与回报的图表。请注意,在回溯等于 110 条时有一个“全局”最大值。如果我们看到回溯与回报无关的情况,那么这将引起关注:

SPY-IWM 线性回归对冲比率回顾期敏感性分析

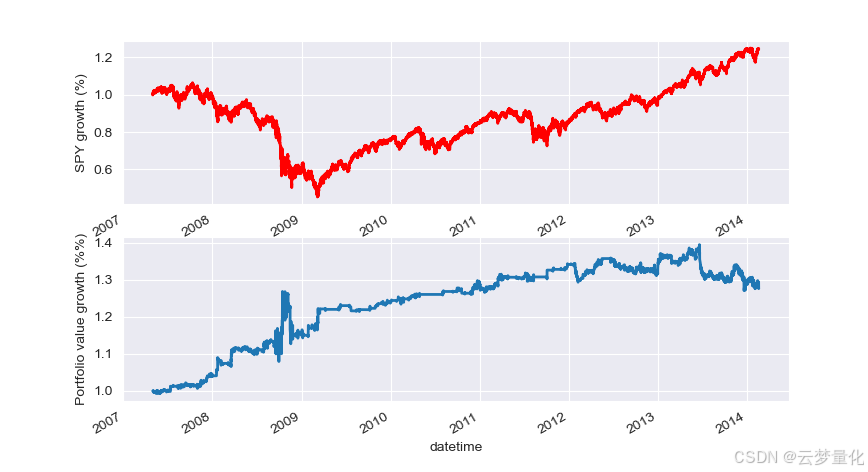

如果没有向上倾斜的股权曲线,那么任何回溯测试文章都是不完整的!因此,如果您希望绘制累计收益与时间的曲线,则可以使用以下代码,该代码将绘制从回溯参数研究中生成的最终投资组合。您需要根据要可视化的图表来选择回溯。该图表还绘制了 SPY 在同一时期的收益,以帮助进行比较:

#mr_spy_iwm.py

# This is still within the main function

print("Plotting the performance charts...")

fig = plt.figure()

ax1 = fig.add_subplot(211, ylabel='%s growth (%%)' % symbols[0])

(pairs['%s_close' % symbols[0].lower()].pct_change()+1.0).cumprod().plot(ax=ax1, color='r', lw=2.)

ax2 = fig.add_subplot(212, ylabel='Portfolio value growth (%%)')

portfolio['returns'].plot(ax=ax2, lw=2.)

plt.show()

以下股权曲线图的回顾期为 100 天:

SPY-IWM 均值回归策略投资组合权益曲线

请注意,SPY 在 2009 年金融危机期间的下跌幅度很大。该策略在此阶段也经历了一段波动期。还请注意,由于 SPY 在此期间的强烈趋势性(反映了标准普尔 500 指数),其表现在去年有所恶化。

请注意,在计算价差的 z 分数时,我们仍然必须考虑前瞻偏差。此外,所有这些计算都是在没有交易成本的情况下进行的。一旦考虑到这些因素,该策略的表现肯定会非常糟糕。费用、买卖价差和滑点目前都未考虑在内。此外,该策略以 ETF 的零碎单位进行交易,这也非常不现实。

转存中…(img-DmAD6tBp-1729221920090)]SPY-IWM 均值回归策略投资组合权益曲线

请注意,SPY 在 2009 年金融危机期间的下跌幅度很大。该策略在此阶段也经历了一段波动期。还请注意,由于 SPY 在此期间的强烈趋势性(反映了标准普尔 500 指数),其表现在去年有所恶化。

请注意,在计算价差的 z 分数时,我们仍然必须考虑前瞻偏差。此外,所有这些计算都是在没有交易成本的情况下进行的。一旦考虑到这些因素,该策略的表现肯定会非常糟糕。费用、买卖价差和滑点目前都未考虑在内。此外,该策略以 ETF 的零碎单位进行交易,这也非常不现实。

在后面的文章中,我们将创建一个更加复杂的事件驱动回测器,它将考虑到这些因素,并让我们对我们的权益曲线和绩效指标更加有信心。

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言