概述:

本篇博文,使用逻辑回归进行银行卡欺诈分析,对于不均衡样本的数据预处理处理展示了两种方法:

- 向下采样策略

- 向上采样策略(文中使用SMOTE算法)

然后对比了数据进行上述处理前后的效果对比。此外还对不同阈值对分类模型的影响进行了探讨。文中有完整的代码和图示。并有详细的中英文代码注释。

涉及到的技术有:

- pandas库

- numpy库

- sklearn库

- imblearn库

- matplot库

下面是正文:

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

%matplotlib inline

data = pd.read_csv("creditcard.csv")

data.head()

| Time | V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Amount | Class | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.0 | -1.359807 | -0.072781 | 2.536347 | 1.378155 | -0.338321 | 0.462388 | 0.239599 | 0.098698 | 0.363787 | ... | -0.018307 | 0.277838 | -0.110474 | 0.066928 | 0.128539 | -0.189115 | 0.133558 | -0.021053 | 149.62 | 0 |

| 1 | 0.0 | 1.191857 | 0.266151 | 0.166480 | 0.448154 | 0.060018 | -0.082361 | -0.078803 | 0.085102 | -0.255425 | ... | -0.225775 | -0.638672 | 0.101288 | -0.339846 | 0.167170 | 0.125895 | -0.008983 | 0.014724 | 2.69 | 0 |

| 2 | 1.0 | -1.358354 | -1.340163 | 1.773209 | 0.379780 | -0.503198 | 1.800499 | 0.791461 | 0.247676 | -1.514654 | ... | 0.247998 | 0.771679 | 0.909412 | -0.689281 | -0.327642 | -0.139097 | -0.055353 | -0.059752 | 378.66 | 0 |

| 3 | 1.0 | -0.966272 | -0.185226 | 1.792993 | -0.863291 | -0.010309 | 1.247203 | 0.237609 | 0.377436 | -1.387024 | ... | -0.108300 | 0.005274 | -0.190321 | -1.175575 | 0.647376 | -0.221929 | 0.062723 | 0.061458 | 123.50 | 0 |

| 4 | 2.0 | -1.158233 | 0.877737 | 1.548718 | 0.403034 | -0.407193 | 0.095921 | 0.592941 | -0.270533 | 0.817739 | ... | -0.009431 | 0.798278 | -0.137458 | 0.141267 | -0.206010 | 0.502292 | 0.219422 | 0.215153 | 69.99 | 0 |

5 rows × 31 columns

#count_classes = pd.value_counts(data['Class'], sort = True).sort_index() #

#把某列数据传入,自动计算各类型数据的数量

count_classes = pd.value_counts(data['Class'], sort = True)

count_classes.plot(kind = 'bar')

plt.title("Fraud class histogram")

plt.xlabel("Class")

plt.ylabel("Frequency")

Text(0, 0.5, 'Frequency')

#sklearn(库)中有数据预处理模块(processing) and 函数(StandardScaler)

from sklearn.preprocessing import StandardScaler

# 将给定数据进行标准化,并作为新的一列存入data(新的列名“normAmount”)

# data['normAmount'] = StandardScaler().fit_transform(data['Amount'].reshape(-1, 1)) #已弃用,原因,data[]的类型是series,而data[].values类型是numpy.ndarray which support reshape operation

data['normAmount'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1,1))

# 丢弃指定的列

data = data.drop(['Time','Amount'],axis=1)

data.head()

| V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | V10 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Class | normAmount | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | -1.359807 | -0.072781 | 2.536347 | 1.378155 | -0.338321 | 0.462388 | 0.239599 | 0.098698 | 0.363787 | 0.090794 | ... | -0.018307 | 0.277838 | -0.110474 | 0.066928 | 0.128539 | -0.189115 | 0.133558 | -0.021053 | 0 | 0.244964 |

| 1 | 1.191857 | 0.266151 | 0.166480 | 0.448154 | 0.060018 | -0.082361 | -0.078803 | 0.085102 | -0.255425 | -0.166974 | ... | -0.225775 | -0.638672 | 0.101288 | -0.339846 | 0.167170 | 0.125895 | -0.008983 | 0.014724 | 0 | -0.342475 |

| 2 | -1.358354 | -1.340163 | 1.773209 | 0.379780 | -0.503198 | 1.800499 | 0.791461 | 0.247676 | -1.514654 | 0.207643 | ... | 0.247998 | 0.771679 | 0.909412 | -0.689281 | -0.327642 | -0.139097 | -0.055353 | -0.059752 | 0 | 1.160686 |

| 3 | -0.966272 | -0.185226 | 1.792993 | -0.863291 | -0.010309 | 1.247203 | 0.237609 | 0.377436 | -1.387024 | -0.054952 | ... | -0.108300 | 0.005274 | -0.190321 | -1.175575 | 0.647376 | -0.221929 | 0.062723 | 0.061458 | 0 | 0.140534 |

| 4 | -1.158233 | 0.877737 | 1.548718 | 0.403034 | -0.407193 | 0.095921 | 0.592941 | -0.270533 | 0.817739 | 0.753074 | ... | -0.009431 | 0.798278 | -0.137458 | 0.141267 | -0.206010 | 0.502292 | 0.219422 | 0.215153 | 0 | -0.073403 |

5 rows × 30 columns

type(data[data.Class == 1].values) #Values 获取数据底层存储的是numpy数组

numpy.ndarray

#构造特征X 和 目标值 y

#data.iloc[] can :

# *Indexing both axes**

# You can mix the indexer types for the index and columns. Use ``:`` to

# select the entire axis.

X = data.iloc[:, data.columns != 'Class'] # 与x = data[data.columns!="Class"]不等价:We are left with two options: a single key, and a collection of keys,

y = data.iloc[:, data.columns == 'Class']

# Number of data points in the minority class

# 计算欺诈样本个数和对应的索引 indices(index的复数形式) 。注意:Values 获取数据底层存储的是numpy数组 Index 获取索引

number_records_fraud = len(data[data.Class == 1])

fraud_indices = np.array(data[data.Class == 1].index)

# Picking the indicates of the normal classes

#获取未被欺诈的样本的索引

normal_indices = data[data.Class == 0].index

# Out of the indicates we picked, randomly select "x" number (number_records_fraud)

random_normal_indices = np.random.choice(normal_indices, number_records_fraud, replace = False)

#下面一行代码操作其实多余,因为上一行的结果就是numpy.ndarray

random_normal_indices = np.array(random_normal_indices)

# Appending the 2 indicates:

#将两个索引结合 concatenate:将一系列事情结合(联系)起来

under_sample_indices = np.concatenate([fraud_indices,random_normal_indices])

# Under sample dataset

#根据索引获取对应的数据,生成新的数据样本:under_sample_data

under_sample_data = data.iloc[under_sample_indices,:]

#从新样本中构造X 和 Y ,用于后面训练

X_undersample = under_sample_data.iloc[:, under_sample_data.columns != 'Class']

y_undersample = under_sample_data.iloc[:, under_sample_data.columns == 'Class']

# Showing ratio

#显示新样本中比率信息

print("Percentage of normal transactions: ", len(under_sample_data[under_sample_data.Class == 0])/len(under_sample_data))

print("Percentage of fraud transactions: ", len(under_sample_data[under_sample_data.Class == 1])/len(under_sample_data))

print("Total number of transactions in resampled data: ", len(under_sample_data))

Percentage of normal transactions: 0.5

Percentage of fraud transactions: 0.5

Total number of transactions in resampled data: 984

from sklearn.model_selection import train_test_split #交叉验证模块 导入数据分割函数

#交叉验证:在训练数据平分,将每份分别做验证集,另外的做训练集,将误差取一个均值(除以平分数)

# Whole dataset

#数据分割操作

X_train, X_test, y_train, y_test = train_test_split(X,y,test_size = 0.3, random_state = 0)

print("Number transactions train dataset: ", len(X_train))

print("Number transactions test dataset: ", len(X_test))

print("Total number of transactions: ", len(X_train)+len(X_test))

# Undersampled dataset

#X_undersample是根据向下根据采样策略从原始数据的一个子集

#下采样策略:本案例,欺诈用户远远小于正常用户,所以从正常用户抽取和欺诈用户数量相同的数据,与欺诈用户共同构成子集

X_train_undersample, X_test_undersample, y_train_undersample, y_test_undersample = train_test_split(X_undersample

,y_undersample

,test_size = 0.3

,random_state = 0)

print("")

print("Number transactions train dataset: ", len(X_train_undersample))

print("Number transactions test dataset: ", len(X_test_undersample))

print("Total number of transactions: ", len(X_train_undersample)+len(X_test_undersample))

Number transactions train dataset: 199364

Number transactions test dataset: 85443

Total number of transactions: 284807

Number transactions train dataset: 688

Number transactions test dataset: 296

Total number of transactions: 984

#Recall = TP/(TP+FN)

#What is Recall(召回率):

#是数据挖掘、机器学习和推荐系统中的评测指标之一,召回率是覆盖面的度量,度量有多个正例被分为正例,详情:https://www.cnblogs.com/Zhi-Z/p/8728168.html

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import KFold, cross_val_score #KFold用于交叉验证 cross_val_score用于交叉验证评估结果

from sklearn.metrics import confusion_matrix,recall_score,classification_report #混淆矩阵 召回率评估 分类结果报告

def printing_Kfold_scores(x_train_data,y_train_data):

fold = KFold(n_splits=5,shuffle=False) #切分成指定份数

# Different C parameters

#正则化惩罚项,图例:https://img-blog.csdnimg.cn/20200215102344486.png

#下面的c_param_range就是惩罚力度,i.e.(c*惩罚项)

c_param_range = [0.01,0.1,1,10,100]

results_table = pd.DataFrame(index = range(len(c_param_range),2), columns = ['C_parameter','Mean recall score'])

results_table['C_parameter'] = c_param_range

# the k-fold will give 2 lists: train_indices = indices[0], test_indices = indices[1]

j = 0

for c_param in c_param_range:

print('-------------------------------------------')

print('C parameter: ', c_param)

print('-------------------------------------------')

print('')

recall_accs = []

for iteration, indices in enumerate(fold.split(x_train_data.values),start=1): #enumerate返回一个序号(可以指定start参数从几开始)和 可迭代参数

# Call the logistic regression model with a certain C parameter

# 创建一个逻辑回归模型,指定惩罚力度和惩罚项生成方法(l1 表示使用权重绝对值之和)

lr = LogisticRegression(C = c_param, penalty = 'l1',solver= 'liblinear')

# Use the training data to fit the model. In this case, we use the portion of the fold to train the model

# with indices[0]. We then predict on the portion assigned as the 'test cross validation' with indices[1]

# 使用x和y训练模型。注意X的行数和y的行数应该相同

lr.fit(x_train_data.iloc[indices[0],:],y_train_data.iloc[indices[0],:].values.ravel())

# Predict values using the test indices in the training data

# 传入x进行预测,生成预测值predicted y

y_pred_undersample = lr.predict(x_train_data.iloc[indices[1],:].values)

# Calculate the recall score and append it to a list for recall scores representing the current c_parameter

# 将预测值和真实值进行比较

recall_acc = recall_score(y_train_data.iloc[indices[1],:].values,y_pred_undersample)

recall_accs.append(recall_acc)

print('Iteration ', iteration,': recall score = ', recall_acc)

# The mean value of those recall scores is the metric we want to save and get hold of.

#设置第j个惩罚力度对应的平均召回率,更二维数组某个元素赋值一个道理,只不过列名是字符串而已。更c++中a[i][j]一个意思

results_table.loc[j,'Mean recall score'] = np.mean(recall_accs,out=None)

j += 1

print('')

print('Mean recall score ', np.mean(recall_accs))

print('')

print(results_table)

print("")

#idxmax函数返回Series的最大值的索引,注意,series内部一定要是数字类型。不能是object。因为object无法比较大小

best_c = results_table.loc[results_table['Mean recall score'].astype('float64').idxmax()]['C_parameter']

# Finally, we can check which C parameter is the best amongst the chosen.

print('*********************************************************************************')

print('Best model to choose from cross validation is with C parameter = ', best_c)

print('*********************************************************************************')

return best_c

best_c = printing_Kfold_scores(X_train_undersample,y_train_undersample)

#best_c i.e 最佳的惩罚力度值

-------------------------------------------

C parameter: 0.01

-------------------------------------------

Iteration 1 : recall score = 0.9452054794520548

Iteration 2 : recall score = 0.9315068493150684

Iteration 3 : recall score = 1.0

Iteration 4 : recall score = 0.9594594594594594

Iteration 5 : recall score = 0.9848484848484849

Mean recall score 0.9642040546150135

-------------------------------------------

C parameter: 0.1

-------------------------------------------

Iteration 1 : recall score = 0.8493150684931506

Iteration 2 : recall score = 0.863013698630137

Iteration 3 : recall score = 0.9661016949152542

Iteration 4 : recall score = 0.9324324324324325

Iteration 5 : recall score = 0.8939393939393939

Mean recall score 0.9009604576820737

-------------------------------------------

C parameter: 1

-------------------------------------------

Iteration 1 : recall score = 0.8493150684931506

Iteration 2 : recall score = 0.8904109589041096

Iteration 3 : recall score = 0.9830508474576272

Iteration 4 : recall score = 0.9459459459459459

Iteration 5 : recall score = 0.9090909090909091

Mean recall score 0.9155627459783485

-------------------------------------------

C parameter: 10

-------------------------------------------

Iteration 1 : recall score = 0.8493150684931506

Iteration 2 : recall score = 0.8904109589041096

Iteration 3 : recall score = 0.9830508474576272

Iteration 4 : recall score = 0.9594594594594594

Iteration 5 : recall score = 0.9090909090909091

Mean recall score 0.9182654486810511

-------------------------------------------

C parameter: 100

-------------------------------------------

Iteration 1 : recall score = 0.8493150684931506

Iteration 2 : recall score = 0.8904109589041096

Iteration 3 : recall score = 0.9830508474576272

Iteration 4 : recall score = 0.9594594594594594

Iteration 5 : recall score = 0.9090909090909091

Mean recall score 0.9182654486810511

C_parameter Mean recall score

0 0.01 0.964204

1 0.10 0.90096

2 1.00 0.915563

3 10.00 0.918265

4 100.00 0.918265

*********************************************************************************

Best model to choose from cross validation is with C parameter = 0.01

*********************************************************************************

def plot_confusion_matrix(cm, classes,

title='Confusion matrix',

cmap=plt.cm.Blues):

"""

This function prints and plots the confusion matrix.

"""

plt.imshow(cm, interpolation='nearest', cmap=cmap)

plt.title(title)

plt.colorbar()

tick_marks = np.arange(len(classes))

plt.xticks(tick_marks, classes, rotation=0)

plt.yticks(tick_marks, classes)

thresh = cm.max() / 2.

for i, j in itertools.product(range(cm.shape[0]), range(cm.shape[1])):

plt.text(j, i, cm[i, j],

horizontalalignment="center",

color="white" if cm[i, j] > thresh else "black")

plt.tight_layout()

plt.ylabel('True label')

plt.xlabel('Predicted label')

# 以下用向下采样处理后的数据集训练模型,并使用该数据集中分割出来的测试集进行测试

import itertools #itertools 是python的迭代器模块,itertools提供的工具相当高效且节省内存。

# 创建&训练Logistic Regression模型并预测

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample = lr.predict(X_test_undersample.values)

# Compute confusion matrix

# 计算混淆矩阵

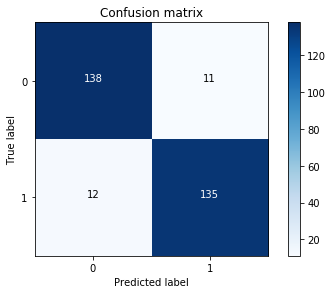

cnf_matrix = confusion_matrix(y_test_undersample,y_pred_undersample)

print("混淆矩阵:\n",cnf_matrix,"\n",type(cnf_matrix),"\n")

np.set_printoptions(precision=2) #输出的精度,即小数点后位数,默认8

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# Plot non-normalized confusion matrix

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix

, classes=class_names

, title='Confusion matrix')

plt.show()

混淆矩阵:

[[138 11]

[ 12 135]]

<class 'numpy.ndarray'>

Recall metric in the testing dataset: 0.9183673469387755

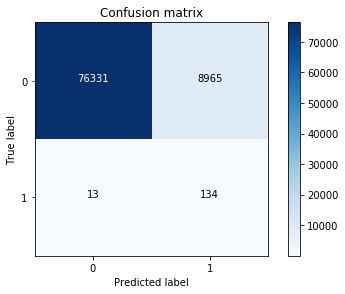

# 以下用向下采样处理后的数据集训练模型,并使用原始数据中分割出来的测试集进行测试

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred = lr.predict(X_test.values)

# Compute confusion matrix

cnf_matrix = confusion_matrix(y_test,y_pred)

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# Plot non-normalized confusion matrix

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix

, classes=class_names

, title='Confusion matrix')

plt.show()

Recall metric in the testing dataset: 0.9115646258503401

#下面不对原始数据作向下采样处理,并直接训练模型。分析模型和混淆矩阵

best_c = printing_Kfold_scores(X_train,y_train)

-------------------------------------------

C parameter: 0.01

-------------------------------------------

Iteration 1 : recall score = 0.4925373134328358

Iteration 2 : recall score = 0.6027397260273972

Iteration 3 : recall score = 0.6833333333333333

Iteration 4 : recall score = 0.5692307692307692

Iteration 5 : recall score = 0.45

Mean recall score 0.5595682284048672

-------------------------------------------

C parameter: 0.1

-------------------------------------------

Iteration 1 : recall score = 0.5671641791044776

Iteration 2 : recall score = 0.6164383561643836

Iteration 3 : recall score = 0.6833333333333333

Iteration 4 : recall score = 0.5846153846153846

Iteration 5 : recall score = 0.525

Mean recall score 0.5953102506435158

-------------------------------------------

C parameter: 1

-------------------------------------------

Iteration 1 : recall score = 0.5522388059701493

Iteration 2 : recall score = 0.6164383561643836

Iteration 3 : recall score = 0.7166666666666667

Iteration 4 : recall score = 0.6153846153846154

Iteration 5 : recall score = 0.5625

Mean recall score 0.612645688837163

-------------------------------------------

C parameter: 10

-------------------------------------------

Iteration 1 : recall score = 0.5522388059701493

Iteration 2 : recall score = 0.6164383561643836

Iteration 3 : recall score = 0.7333333333333333

Iteration 4 : recall score = 0.6153846153846154

Iteration 5 : recall score = 0.575

Mean recall score 0.6184790221704963

-------------------------------------------

C parameter: 100

-------------------------------------------

Iteration 1 : recall score = 0.5522388059701493

Iteration 2 : recall score = 0.6164383561643836

Iteration 3 : recall score = 0.7333333333333333

Iteration 4 : recall score = 0.6153846153846154

Iteration 5 : recall score = 0.575

Mean recall score 0.6184790221704963

C_parameter Mean recall score

0 0.01 0.559568

1 0.10 0.59531

2 1.00 0.612646

3 10.00 0.618479

4 100.00 0.618479

*********************************************************************************

Best model to choose from cross validation is with C parameter = 10.0

*********************************************************************************

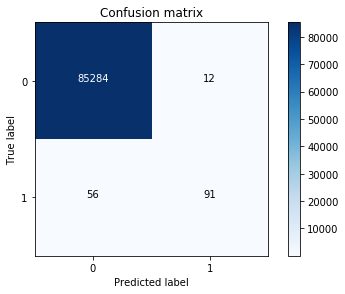

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(X_train,y_train.values.ravel())

y_pred_undersample = lr.predict(X_test.values)

# Compute confusion matrix

cnf_matrix = confusion_matrix(y_test,y_pred_undersample)

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# Plot non-normalized confusion matrix

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix

, classes=class_names

, title='Confusion matrix')

plt.show()

# 可以看到,用未处理的数据进行直接训练得到的模型,召回率偏低、误杀率偏高

Recall metric in the testing dataset: 0.6190476190476191

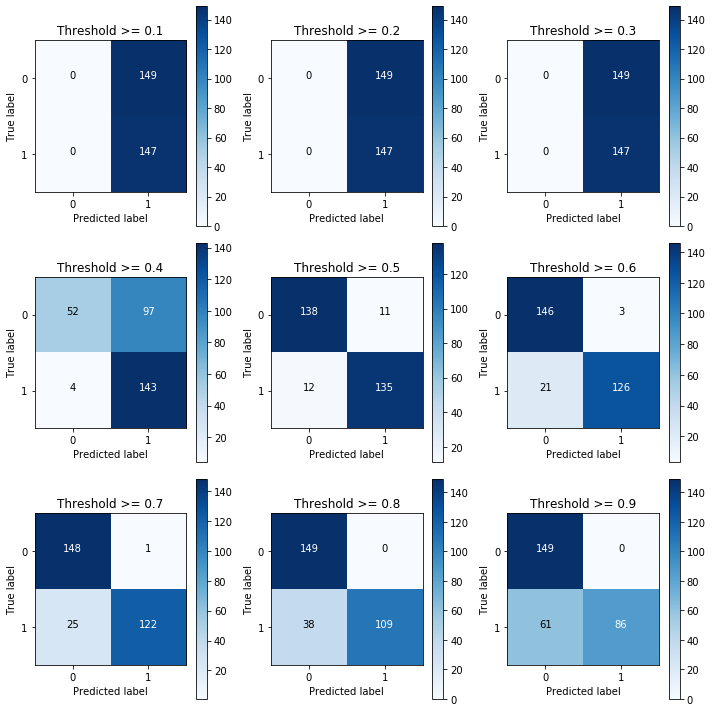

# 下面尝试用向下采样处理后的数据集进行训练、并对比不同阈值对分类效果的影响

lr = LogisticRegression(C = 0.01, penalty = 'l1',solver='liblinear')

lr.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample_proba = lr.predict_proba(X_test_undersample.values)

print("每一个样本对应的预测值:\n",y_pred_undersample_proba[0:5,:])

# 定义一个阈值

thresholds = [0.1,0.2,0.3,0.4,0.5,0.6,0.7,0.8,0.9]

plt.figure(figsize=(10,10))

j = 1

for i in thresholds:

y_test_predictions_high_recall = y_pred_undersample_proba[:,1] > i

plt.subplot(3,3,j)

j += 1

# Compute confusion matrix

cnf_matrix = confusion_matrix(y_test_undersample,y_test_predictions_high_recall)

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# Plot non-normalized confusion matrix

class_names = [0,1]

plot_confusion_matrix(cnf_matrix

, classes=class_names

, title='Threshold >= %s'%i)

每一个样本对应的预测值:

[[0.57 0.43]

[0.57 0.43]

[0. 1. ]

[0.59 0.41]

[0.54 0.46]]

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 0.9727891156462585

Recall metric in the testing dataset: 0.9183673469387755

Recall metric in the testing dataset: 0.8571428571428571

Recall metric in the testing dataset: 0.8299319727891157

Recall metric in the testing dataset: 0.7414965986394558

Recall metric in the testing dataset: 0.5850340136054422

#####################################向上采样策略:SMOTE方法 训练模型效果比较############################################

import pandas as pd

from imblearn.over_sampling import SMOTE #SMOTE数据生成算法、即向上采样策略

from sklearn.ensemble import RandomForestClassifier

from sklearn.metrics import confusion_matrix

from sklearn.model_selection import train_test_split

credit_cards=pd.read_csv('creditcard.csv')

columns=credit_cards.columns

# The labels are in the last column ('Class'). Simply remove it to obtain features columns

# 删除最后一列,最后一列索引( len(columns)-1 )

features_columns=columns.delete(len(columns)-1)

# 从原始数据分离出特征 和 标签

features=credit_cards[features_columns]

labels=credit_cards['Class']

# 将数据分成训练集 和 测试集

features_train, features_test, labels_train, labels_test = train_test_split(features,

labels,

test_size=0.2,

random_state=0)

len(labels_train)

227845

oversampler=SMOTE(random_state=0)

# 将训练数据传入,算法将会根据label值自动平衡并生成新的数据

os_features,os_labels=oversampler.fit_sample(features_train,labels_train)

len(os_labels[os_labels==1])

227454

os_features = pd.DataFrame(os_features)

os_labels = pd.DataFrame(os_labels)

best_c = printing_Kfold_scores(os_features,os_labels)

-------------------------------------------

C parameter: 0.01

-------------------------------------------

Iteration 1 : recall score = 0.8903225806451613

Iteration 2 : recall score = 0.8947368421052632

Iteration 3 : recall score = 0.9688170853159235

Iteration 4 : recall score = 0.9578263593497544

Iteration 5 : recall score = 0.9584198898671151

Mean recall score 0.9340245514566435

-------------------------------------------

C parameter: 0.1

-------------------------------------------

Iteration 1 : recall score = 0.8903225806451613

Iteration 2 : recall score = 0.8947368421052632

Iteration 3 : recall score = 0.9704105344694036

Iteration 4 : recall score = 0.9599366900781482

Iteration 5 : recall score = 0.9605631945131401

Mean recall score 0.9351939683622232

-------------------------------------------

C parameter: 1

-------------------------------------------

Iteration 1 : recall score = 0.8903225806451613

Iteration 2 : recall score = 0.8947368421052632

Iteration 3 : recall score = 0.9705211906606175

Iteration 4 : recall score = 0.9596069509018367

Iteration 5 : recall score = 0.9607830206306811

Mean recall score 0.9351941169887119

-------------------------------------------

C parameter: 10

-------------------------------------------

Iteration 1 : recall score = 0.8903225806451613

Iteration 2 : recall score = 0.8947368421052632

Iteration 3 : recall score = 0.9705211906606175

Iteration 4 : recall score = 0.9601894901133203

Iteration 5 : recall score = 0.9601455248898122

Mean recall score 0.9351831256828349

-------------------------------------------

C parameter: 100

-------------------------------------------

Iteration 1 : recall score = 0.8903225806451613

Iteration 2 : recall score = 0.8947368421052632

Iteration 3 : recall score = 0.970366271992918

Iteration 4 : recall score = 0.9594091073960497

Iteration 5 : recall score = 0.960530220595509

Mean recall score 0.9350730045469803

C_parameter Mean recall score

0 0.01 0.934025

1 0.10 0.935194

2 1.00 0.935194

3 10.00 0.935183

4 100.00 0.935073

*********************************************************************************

Best model to choose from cross validation is with C parameter = 1.0

*********************************************************************************

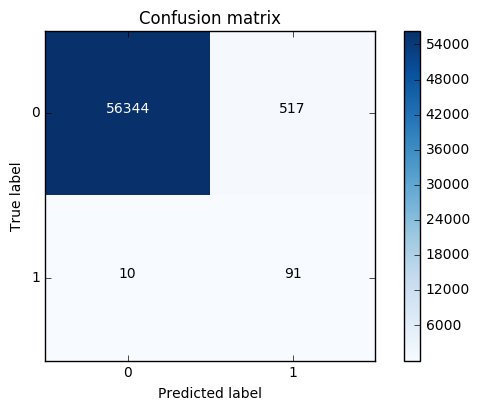

lr = LogisticRegression(C = best_c, penalty = 'l1')

lr.fit(os_features,os_labels.values.ravel())

y_pred = lr.predict(features_test.values)

# Compute confusion matrix

cnf_matrix = confusion_matrix(labels_test,y_pred)

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# Plot non-normalized confusion matrix

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix

, classes=class_names

, title='Confusion matrix')

plt.show()

Recall metric in the testing dataset: 0.90099009901

#Summary

# 对于样本不均匀的情况:

# 1、 利用下采样策略

# 2、利用SMOTE数据生成算法

#建议:数据利用越多越好。优先使用SMOTE数据生成算法

815

815

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言