python数据分析--- ch14-15 python计量回归模型

1.Ch14–python 回归分析

1.1 相关分析

1.1.1 相关系数的概念

r = ∑ ( x i − x ˉ ) ( y i − y ˉ ) ∑ ( x i − x ˉ ) 2 ∑ ( y i − y ˉ ) 2 r = \frac{\sum (x_i - \bar{x})(y_i - \bar{y})}{\sqrt{\sum (x_i - \bar{x})^2 \sum (y_i - \bar{y})^2}} r=∑(xi−xˉ)2∑(yi−yˉ)2∑(xi−xˉ)(yi−yˉ)

1.1.2 使用模拟数据计算变量之间的相关系数和绘图

# 导入包

import numpy as np

import statsmodels.tsa.stattools as sts

import matplotlib.pyplot as plt#绘图

import pandas as pd

import seaborn as sns#绘图

import statsmodels.api as sm

#生成随机数并绘制图形

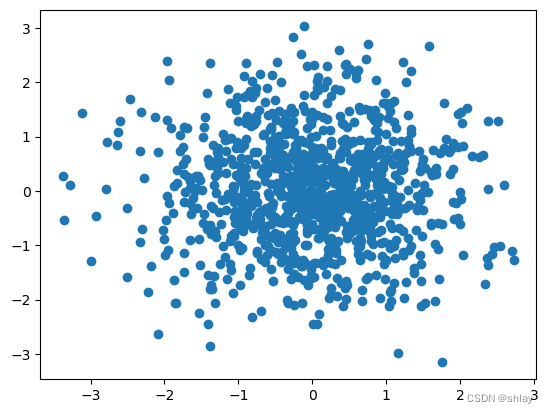

X = np.random.randn(1000)

Y = np.random.randn(1000)

plt.scatter(X,Y)

plt.show()

print("correlation of X and Y is ")

np.corrcoef(X,Y)[0,1]

output

correlation of X and Y is

-0.0070692509611224395

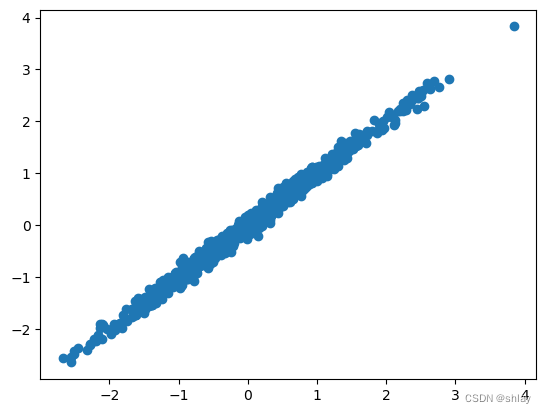

X = np.random.randn(1000)

Y = X + np.random.normal(0,0.1,1000)

plt.scatter(X,Y)

plt.show()

print("correlation of X and Y is ")

np.corrcoef(X,Y)[0,1]

output

correlation of X and Y is

0.9953589318626792

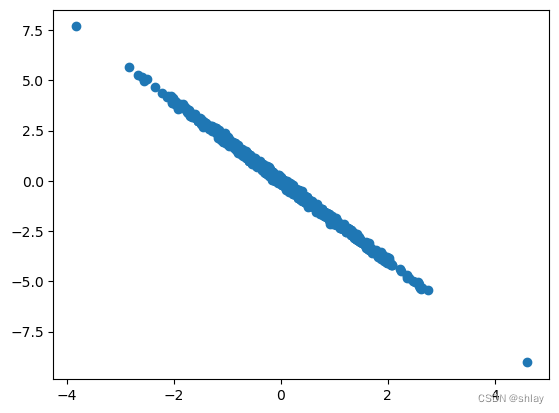

X = np.random.randn(1000)

Y = -2*X + np.random.normal(0,0.1,1000)

plt.scatter(X,Y)

plt.show()

print("correlation of X and Y is ")

np.corrcoef(X,Y)[0,1]

output

correlation of X and Y is

-0.9987776408463028

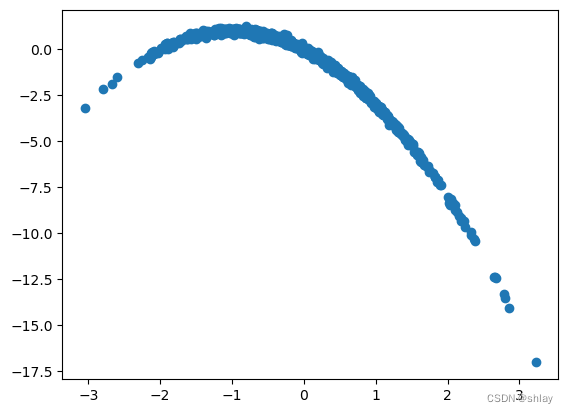

X = np.random.randn(1000)

Y = -X*X-2*X + np.random.normal(0,0.1,1000)

plt.scatter(X,Y)

plt.show()

print("correlation of X and Y is ")

np.corrcoef(X,Y)[0,1]

output

correlation of X and Y is

-0.8357355999573256

1.1.3 使用本地数据计算变量之间的相关系数和绘图

import pandas as pd

import numpy as np

import scipy.stats.stats as stats

r = ∑ ( x − m x ) ( y − m y ) ∑ ( x − m x ) 2 ∑ ( y − m y ) 2 r = \frac{\sum (x - m_x) (y - m_y)} {\sqrt{\sum (x - m_x)^2 \sum (y - m_y)^2}} r=∑(x−mx)2∑(y−my)2∑(x−mx)(y−my)

?stats.pearsonr

import numpy as np

from scipy import stats

x, y = [1, 2, 3, 4, 5, 6, 7], [10, 9, 2.5, 6, 4, 3, 2]

res = stats.pearsonr(x, y)

res

output

PearsonRResult(statistic=-0.8285038835884277, pvalue=0.021280260007523356)

数据文件“ch14_1.xls”下载

#读取数据并创建数据表,名称为data。

data=pd.DataFrame(pd.read_excel('./data/ch14_1.xls'))

#查看数据表前5行的内容

print(data.head())

#取adv和sale数据

x = np.array(data['adv'])

y = np.array(data['sale'])

r=stats.pearsonr(x,y)[0]

print(r)

output

time adv sale

0 1 35 50

1 2 50 100

2 3 56 120

3 4 68 180

4 5 70 175

0.9636816932556833

1.1.4 使用网上数据计算变量之间的相关系数和绘图

import pandas as pd

import numpy as np

# 创建一个包含10支股票的DataFrame

np.random.seed(42) # 为了可重复性设置随机种子

stock_data = pd.DataFrame(np.random.randn(100, 10), columns=[f'Stock_{i}' for i in range(1, 11)])

# 将DataFrame转换为CSV文件

stock_data.to_csv('./data/ch14_2_stock_prices.csv', index=False)

print('CSV文件已生成。')

output

CSV文件已生成。

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

df = pd.read_csv('./data/ch14_2_stock_prices.csv')

df.head()

output

| Stock_1 | Stock_2 | Stock_3 | Stock_4 | Stock_5 | Stock_6 | Stock_7 | Stock_8 | Stock_9 | Stock_10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.496714 | -0.138264 | 0.647689 | 1.523030 | -0.234153 | -0.234137 | 1.579213 | 0.767435 | -0.469474 | 0.542560 |

| 1 | -0.463418 | -0.465730 | 0.241962 | -1.913280 | -1.724918 | -0.562288 | -1.012831 | 0.314247 | -0.908024 | -1.412304 |

| 2 | 1.465649 | -0.225776 | 0.067528 | -1.424748 | -0.544383 | 0.110923 | -1.150994 | 0.375698 | -0.600639 | -0.291694 |

| 3 | -0.601707 | 1.852278 | -0.013497 | -1.057711 | 0.822545 | -1.220844 | 0.208864 | -1.959670 | -1.328186 | 0.196861 |

| 4 | 0.738467 | 0.171368 | -0.115648 | -0.301104 | -1.478522 | -0.719844 | -0.460639 | 1.057122 | 0.343618 | -1.763040 |

correlation_matrix = df.corr()

plt.figure(figsize=(10, 8)) # 可以根据需要调整图形大小

sns.heatmap(correlation_matrix, annot=True, fmt=".2f", cmap='coolwarm', square=True)

plt.title('Heatmap of Stock Price Correlation')

plt.show()

output

1.2 一元回归分析

1.2.1 应用Python-statsmodels工具作一元线性回归分析

import pandas as pd

import numpy as np

import scipy.stats as ss

#读取数据并创建数据表,名称为data。

data=pd.DataFrame(pd.read_excel('./data/ch14_3.xls'))

print(data.head())

print(data.describe())

#此命令的含义是对销售额xse、人数rs等变量进行描述性统计分析。

#对数据进行相关分析

x = np.array(data['rs'])

y = np.array(data['xse'])

r=ss.pearsonr(x,y)[0]

#本命令的含义是对新产品销售额、销售人员人数等变量进行相关性分析

print ('相关系数为:',round(r,4))

print('相关系数矩阵为:\n', data.corr())

output

dq xse rs

0 1 385 17

1 2 251 10

2 3 701 44

3 4 479 30

4 5 433 22

dq xse rs

count 10.00000 10.000000 10.000000

mean 5.50000 446.600000 22.100000

std 3.02765 160.224287 12.705642

min 1.00000 217.000000 5.000000

25% 3.25000 362.500000 12.000000

50% 5.50000 422.000000 19.500000

75% 7.75000 555.500000 30.750000

max 10.00000 701.000000 44.000000

相关系数为: 0.9699

相关系数矩阵为:

dq xse rs

dq 1.000000 0.218510 0.085207

xse 0.218510 1.000000 0.969906

rs 0.085207 0.969906 1.000000

# model matrix with intercept

X = sm.add_constant(x)

#least squares fit

model = sm.OLS(y, X)

fit = model.fit()

print(fit.summary())

output

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.941

Model: OLS Adj. R-squared: 0.933

Method: Least Squares F-statistic: 126.9

Date: Wed, 12 Jun 2024 Prob (F-statistic): 3.46e-06

Time: 11:37:48 Log-Likelihood: -50.301

No. Observations: 10 AIC: 104.6

Df Residuals: 8 BIC: 105.2

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 176.2952 27.327 6.451 0.000 113.279 239.311

x1 12.2310 1.086 11.267 0.000 9.728 14.734

==============================================================================

Omnibus: 0.718 Durbin-Watson: 1.407

Prob(Omnibus): 0.698 Jarque-Bera (JB): 0.588

Skew: -0.198 Prob(JB): 0.745

Kurtosis: 1.879 Cond. No. 52.6

==============================================================================

#画线性回归图

import matplotlib.pyplot as plt

plt.scatter(x, y)

plt.plot(x, fit.fittedvalues)

1.2.2 应用Python-sklearn工具作一元线性回归分析

import numpy as np

from sklearn import linear_model

import pandas as pd

# 假设data是已经定义并包含所需列的DataFrame

data=pd.DataFrame(pd.read_excel('./data/ch14_3.xls'))

# 确保data变量已经被定义且包含'rs'和'xse'列

x = np.array(data[['rs']])

y = np.array(data[['xse']])

x

output

array([[17],

[10],

[44],

[30],

[22],

[15],

[11],

[ 5],

[31],

[36]], dtype=int64)

data['rs']

output

0 17

1 10

2 44

3 30

4 22

5 15

6 11

7 5

8 31

9 36

Name: rs, dtype: int64

# 创建线性回归模型并拟合数据

clf = linear_model.LinearRegression()

clf.fit(x, y)

# 打印回归系数和截距

print("回归系数:", clf.coef_)

print("截距:", clf.intercept_)

# 计算并打印R²分数

r_squared = clf.score(x, y)

print("R-squared:", r_squared)

# 输入自变量值进行预测

# 假设你想预测'rs'为40时的'xse'值

prediction = clf.predict([[40]])

print("预测rs = 40时xse的值为 :", prediction[0])

output

回归系数: [[12.2309863]]

截距: [176.2952027]

R-squared: 0.9407180505879883

预测rs = 40时xse的值为 : [665.53465483]

1.3 多元线性回归数据分析

import pandas as pd

import numpy as np

import scipy.stats as ss

#读取数据并创建数据表,名称为data。

data=pd.DataFrame(pd.read_excel('./data/ch14_4.xls'))

print(data.head())

print(data.describe())

output

TC Q PL PF PK

0 0.082 2 2.09 17.9 183

1 0.661 3 2.05 35.1 174

2 0.990 4 2.05 35.1 171

3 0.315 4 1.83 32.2 166

4 0.197 5 2.12 28.6 233

TC Q PL PF PK

count 145.000000 145.000000 145.000000 145.000000 145.000000

mean 12.976097 2133.082759 1.972069 26.176552 174.496552

std 19.794577 2931.942131 0.236807 7.876071 18.209477

min 0.082000 2.000000 1.450000 10.300000 138.000000

25% 2.382000 279.000000 1.760000 21.300000 162.000000

50% 6.754000 1109.000000 2.040000 26.900000 170.000000

75% 14.132000 2507.000000 2.190000 32.200000 183.000000

max 139.422000 16719.000000 2.320000 42.800000 233.000000

#用数组对数据做相关分析

y= np.array(data['TC'])

x1= np.array(data['Q'])

x2= np.array(data['PL'])

x3= np.array(data['PF'])

x4= np.array(data['PK'])

r1=ss.pearsonr(x1,y)[0]

r2=ss.pearsonr(x2,y)[0]

r3=ss.pearsonr(x3,y)[0]

r4=ss.pearsonr(x4,y)[0]

print(f"r1={round(r1,4)};r2={round(r2,4)};r3={round(r3,4)};r4={round(r4,4)}")

output

r1=0.9525;r2=0.2513;r3=0.0339;r4=0.0272

#用数据框对数据做相关分析

corr_matrix = data.corr()

print('相关系数矩阵为:\n', data.corr())

plt.figure(figsize=(10, 8)) # 可以根据需要调整图形大小

sns.heatmap(corr_matrix, annot=True, fmt=".2f", cmap='coolwarm', square=True)

plt.title('Heatmap of data Correlation')

plt.show()

相关系数矩阵为:

TC Q PL PF PK

TC 1.000000 0.952504 0.251338 0.033935 0.027202

Q 0.952504 1.000000 0.171450 -0.077349 0.002869

PL 0.251338 0.171450 1.000000 0.313703 -0.178145

PF 0.033935 -0.077349 0.313703 1.000000 0.125428

PK 0.027202 0.002869 -0.178145 0.125428 1.000000

1.3.1 多元回归分析的Python的statsmodels工具应用

import statsmodels.api as sm

from patsy import dmatrices

vars = ['TC','Q','PL','PF','PK']

df=data[vars]

#显示最后5条记录数据

print (df.tail())

output

TC Q PL PF PK

140 44.894 9956 1.68 28.8 203

141 67.120 11477 2.24 26.5 151

142 73.050 11796 2.12 28.6 148

143 139.422 14359 2.31 33.5 212

144 119.939 16719 2.30 23.6 162

y,X=dmatrices('TC~Q+PL+PF+PK',data=data,return_type='dataframe')

print (y.head())

print (X.head())

model = sm.OLS(y, X)

fit = model.fit()

print (fit.summary())

output

TC

0 0.082

1 0.661

2 0.990

3 0.315

4 0.197

Intercept Q PL PF PK

0 1.0 2.0 2.09 17.9 183.0

1 1.0 3.0 2.05 35.1 174.0

2 1.0 4.0 2.05 35.1 171.0

3 1.0 4.0 1.83 32.2 166.0

4 1.0 5.0 2.12 28.6 233.0

OLS Regression Results

==============================================================================

Dep. Variable: TC R-squared: 0.923

Model: OLS Adj. R-squared: 0.921

Method: Least Squares F-statistic: 418.1

Date: Wed, 12 Jun 2024 Prob (F-statistic): 9.26e-77

Time: 11:38:18 Log-Likelihood: -452.47

No. Observations: 145 AIC: 914.9

Df Residuals: 140 BIC: 929.8

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -22.2210 6.587 -3.373 0.001 -35.245 -9.197

Q 0.0064 0.000 39.258 0.000 0.006 0.007

PL 5.6552 2.176 2.598 0.010 1.352 9.958

PF 0.2078 0.064 3.242 0.001 0.081 0.335

PK 0.0284 0.027 1.073 0.285 -0.024 0.081

==============================================================================

Omnibus: 135.057 Durbin-Watson: 1.560

Prob(Omnibus): 0.000 Jarque-Bera (JB): 4737.912

Skew: 2.907 Prob(JB): 0.00

Kurtosis: 30.394 Cond. No. 5.29e+04

==============================================================================

y,X=dmatrices('TC~Q+PL+PF',data=df,return_type='dataframe')

import statsmodels.api as sm

model = sm.OLS(y, X)

fit = model.fit()

print (fit.summary())

output

OLS Regression Results

==============================================================================

Dep. Variable: TC R-squared: 0.922

Model: OLS Adj. R-squared: 0.920

Method: Least Squares F-statistic: 556.5

Date: Wed, 12 Jun 2024 Prob (F-statistic): 6.39e-78

Time: 11:38:19 Log-Likelihood: -453.06

No. Observations: 145 AIC: 914.1

Df Residuals: 141 BIC: 926.0

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -16.5443 3.928 -4.212 0.000 -24.309 -8.780

Q 0.0064 0.000 39.384 0.000 0.006 0.007

PL 5.0978 2.115 2.411 0.017 0.917 9.278

PF 0.2217 0.063 3.528 0.001 0.097 0.346

==============================================================================

Omnibus: 142.387 Durbin-Watson: 1.590

Prob(Omnibus): 0.000 Jarque-Bera (JB): 5466.347

Skew: 3.134 Prob(JB): 0.00

Kurtosis: 32.419 Cond. No. 3.42e+04

==============================================================================

1.3.2 用scikit-learn工具作多元回归分析

import pandas as pd

print(data.shape)

print(data.head())

output

(145, 5)

TC Q PL PF PK

0 0.082 2 2.09 17.9 183

1 0.661 3 2.05 35.1 174

2 0.990 4 2.05 35.1 171

3 0.315 4 1.83 32.2 166

4 0.197 5 2.12 28.6 233

feature_cols = ['Q', 'PL', 'PF', 'PK']

# use the list to select a subset of the original DataFrame

X = data[feature_cols]

# check the type and shape of X

print (type(X))

print (X.shape)

# select a Series from the DataFrame

y = data['TC']

# print the first 5 values

print (y.head())

output

<class 'pandas.core.frame.DataFrame'>

(145, 4)

0 0.082

1 0.661

2 0.990

3 0.315

4 0.197

Name: TC, dtype: float64

# import seaborn as sns #seaborn程序包需要先安装

# #安装命令:pip install seaborn

# sns.pairplot(data, x_vars=['Q', 'PL', 'PF', 'PK'], y_vars='TC', height=7, aspect=0.8)

import seaborn as sns

import matplotlib.pyplot as plt

# 使用lmplot绘制每个自变量与因变量之间的关系

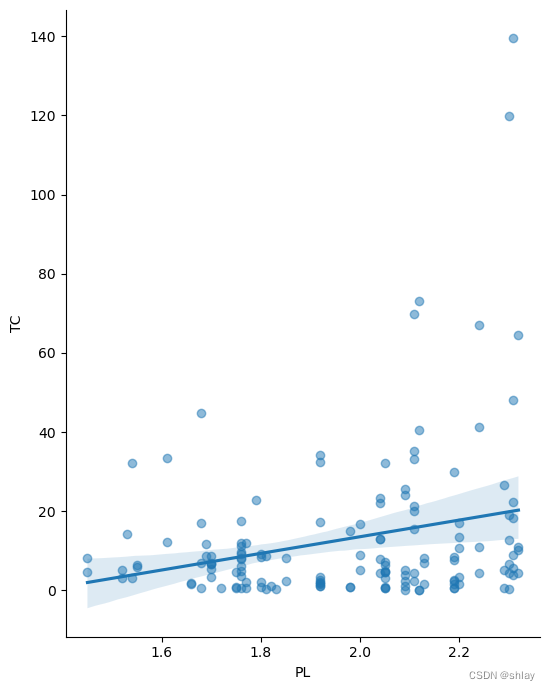

for col in ['Q', 'PL', 'PF', 'PK']:

sns.lmplot(x=col, y='TC', data=data, height=7, aspect=0.8, scatter_kws={'alpha':0.5})

plt.show()

1.4 线性回归模型

#构造训练集和测试集

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, random_state=1)

# default split is 75% for training and 25% for testing

print(X_train.shape)

print(y_train.shape)

print(X_test.shape)

print(y_test.shape)

#线性回归分析的Scikit-learn工具应用

from sklearn.linear_model import LinearRegression

linreg = LinearRegression()

linreg.fit(X_train, y_train)

LinearRegression(copy_X=True, fit_intercept=True, n_jobs=1)

print(linreg.intercept_)

print(linreg.coef_)

# pair the feature names with the coefficients

zip(feature_cols, linreg.coef_)

#预测

y_pred = linreg.predict(X_test)

print(y_pred.round(decimals=4))

output

(108, 4)

(108,)

(37, 4)

(37,)

-15.546621299685215

[5.98807135e-03 5.68597073e+00 1.69334275e-01 9.00966074e-05]

[ 0.4819 4.1567 2.1491 32.6262 6.6678 1.4221 1.9241 17.8204 0.7097

9.0636 4.1637 8.5665 5.6732 8.2366 3.96 25.3146 -0.9507 3.0294

4.5084 2.7402 31.2073 12.9369 2.1043 3.8415 12.741 55.895 26.3795

18.7322 6.7021 0.5052 1.4885 18.4282 13.5925 10.1431 2.7995 7.1969

89.2625]

1.5 回归问题的评价测度

from sklearn import metrics

import numpy as np

# calculate MAE by hand

print("MAE by hand:",(10 + 0 + 20 + 10)/4)

# calculate MAE using scikit-learn

print ("MAE:",metrics.mean_absolute_error(y_test, y_pred))

# calculate MSE by hand

print ("MSE by hand:",(10**2 + 0**2 + 20**2 + 10**2)/4.)

# calculate MSE using scikit-learn

print ("MSE:",metrics.mean_squared_error(y_test, y_pred))

# calculate RMSE by hand

print ("RMSE by hand:",np.sqrt((10**2 + 0**2 + 20**2 + 10**2)/4.))

# calculate RMSE using scikit-learn

print ("RMSE:",np.sqrt(metrics.mean_squared_error(y_test, y_pred)))

output

MAE by hand: 10.0

MAE: 3.559135213796553

MSE by hand: 150.0

MSE: 77.98080985164937

RMSE by hand: 12.24744871391589

RMSE: 8.830674371283846

2. Ch15–python 时间序列分析

2.1 准备工作

2.1.1 加载包

# 加载包

import warnings

warnings.filterwarnings('ignore')

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import statsmodels.api as sm

from statsmodels.tsa.arima.model import ARIMA

from sklearn.metrics import mean_squared_error, mean_absolute_error

from datetime import datetime

#全局配置

#中文字符设定 plt.rcParams属性总结

plt.rcParams['font.sans-serif']=['SimHei']

plt.rcParams['axes.unicode_minus']=False

2.1.2 数据读取及预处理

数据文件“csh601318_processed.csv”下载

df = pd.read_csv('./data/sh601318_processed.csv',index_col='Date')

df.head()

output

| Close | |

|---|---|

| Date | |

| 2015-01-05 | 76.16 |

| 2015-01-06 | 73.73 |

| 2015-01-07 | 73.41 |

| 2015-01-08 | 71.08 |

| 2015-01-09 | 72.84 |

#读取已处理好的数据

df_601318 = df[['Close']]

df_601318.index = pd.to_datetime(df_601318.index, format='%Y-%m-%d') # 将Date列转换为datetime格式

# 查看数据的基本信息

print(df_601318.head())

output

Close

Date

2015-01-05 76.16

2015-01-06 73.73

2015-01-07 73.41

2015-01-08 71.08

2015-01-09 72.84

print(df_601318.info())

output

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 2033 entries, 2015-01-05 to 2023-05-15

Data columns (total 1 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Close 2033 non-null float64

dtypes: float64(1)

memory usage: 31.8 KB

None

print(df_601318.describe())

output

Close

count 2033.000000

mean 59.039838

std 18.942363

min 25.110000

25% 42.840000

50% 58.380000

75% 76.520000

max 93.380000

2.2 可视化股票价格

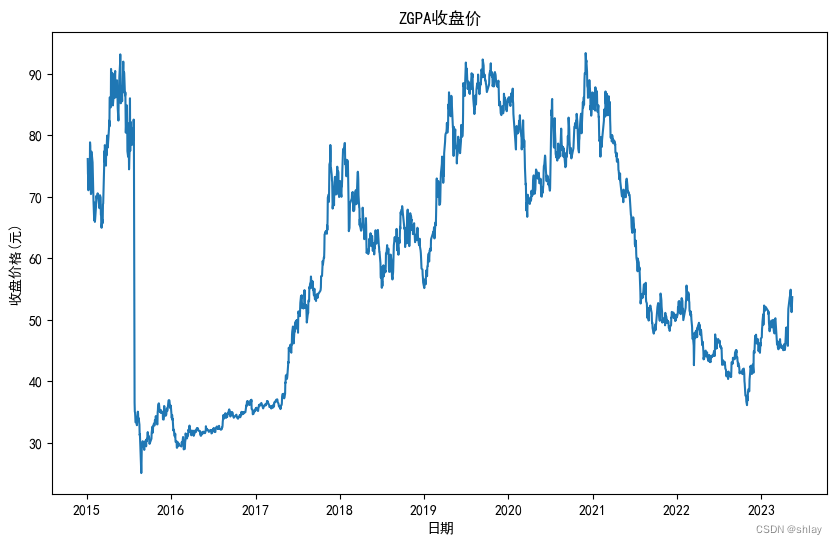

#对数据进行可视化,以了解股票价格的趋势和变化。

plt.figure(figsize=(10, 6))

plt.plot(df_601318['Close'])

plt.title('ZGPA收盘价')

plt.xlabel('日期')

plt.ylabel('收盘价格(元)')

plt.show()

2.3 单位根检验

# 进行ADF检验

result = sm.tsa.stattools.adfuller(df_601318['Close'])

print('ADF Statistic: %f' % result[0])

print('p-value: %f' % result[1])

print('Critical Values:')

for key, value in result[4].items():

print('\t%s: %.3f' % (key, value))

output

ADF Statistic: -1.894778

p-value: 0.334522

Critical Values:

1%: -3.434

5%: -2.863

10%: -2.568

无法拒绝原假设,认为数据是非平稳的。

2.4 差分

2.4.1 一阶差分

# 进行一阶差分

diff1 = df_601318['Close'].diff().dropna()

2.4.2 一阶差分ADF检验

# 进行ADF检验

result = sm.tsa.stattools.adfuller(diff1)

print('ADF Statistic: %f' % result[0])

print('p-value: %f' % result[1])

print('Critical Values:')

for key, value in result[4].items():

print('\t%s: %.3f' % (key, value))

output

ADF Statistic: -8.640510

p-value: 0.000000

Critical Values:

1%: -3.434

5%: -2.863

10%: -2.568

一阶差分后序列平稳

2.4.3 绘制一阶差分后的时序图

# 绘制差分后的时间序列图

fig, ax = plt.subplots(2, 1, figsize=(8, 12))

ax[0].plot(df_601318.index, df_601318['Close'])

ax[0].set_title('原始数据')

ax[1].plot(diff1.index, diff1)

ax[1].set_title('一阶差分')

# ax[2].plot(diff2.index, diff2)

# ax[2].set_title('二阶差分')

plt.show()

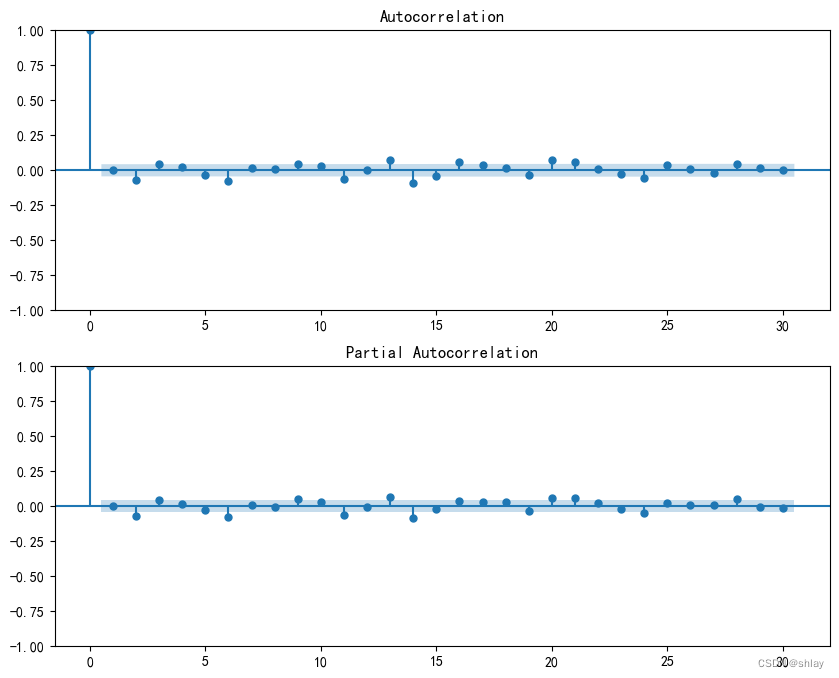

2.5 绘制自相关图和偏自相关图

2.5.1 绘制原序列自相关图和偏自相关图

# 绘制自相关图和偏自相关图

fig, axes = plt.subplots(2, 1, figsize=(10,8))

sm.graphics.tsa.plot_acf(df_601318['Close'], lags=50, ax=axes[0])

sm.graphics.tsa.plot_pacf(df_601318['Close'], lags=30, ax=axes[1])

plt.show()

2.5.2 绘制一阶差分后自相关图和偏自相关图

# 绘制自相关图和偏自相关图

fig, axes = plt.subplots(2, 1, figsize=(10,8))

sm.graphics.tsa.plot_acf(diff1, lags=30, ax=axes[0])

sm.graphics.tsa.plot_pacf(diff1, lags=30, ax=axes[1])

plt.show()

2.6 划分训练集和测试集

2.6.1 按照指定的百分比划分,如:8:2,7:3等

# 假设df是处理好的股票数据

train_size = int(len(df_601318) * 0.8)

train_df = df_601318[:train_size]

test_df = df_601318[train_size:]

# 输出训练集和测试集的数据量

print("训练集数据量:", len(train_df))

print("测试集数据量:", len(test_df))

output

训练集数据量: 1626

测试集数据量: 407

2.6.2 按照指定的日期划分,如:2022-12-31

# 假设df是处理好的股票数据

split_date = datetime(2021, 12, 31)

train_df = df_601318[df_601318.index <= split_date]

test_df = df_601318[df_601318.index > split_date]

# 输出训练集和测试集的数据量

print("训练集数据量:", len(train_df))

print("测试集数据量:", len(test_df))

output

训练集数据量: 1705

测试集数据量: 328

test_df.head()

output

| Close | |

|---|---|

| Date | |

| 2022-01-04 | 51.00 |

| 2022-01-05 | 52.07 |

| 2022-01-06 | 51.30 |

| 2022-01-07 | 52.94 |

| 2022-01-10 | 53.08 |

2.7 模型拟合

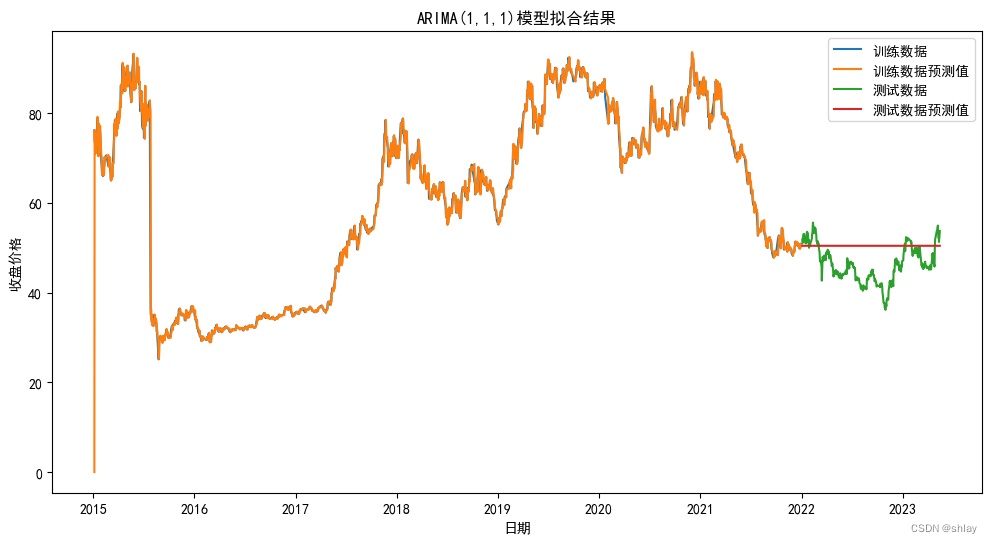

我们可以使用 ARIMA 函数来拟合 ARIMA 模型并进行预测。首先,需要确定 ARIMA 模型的参数。可以通过观察 ACF 和 PACF 图来初步选择参数。在这里,我们将选择 ARIMA(1,1,1) 模型。

# 拟合ARIMA(1,1,1)模型并预测训练集数据

model = ARIMA(train_df, order=(1, 1, 1))

model_fit = model.fit()

# 模型概述

print(model_fit.summary())

output

SARIMAX Results

==============================================================================

Dep. Variable: Close No. Observations: 1705

Model: ARIMA(1, 1, 1) Log Likelihood -3295.505

Date: Wed, 12 Jun 2024 AIC 6597.010

Time: 11:41:15 BIC 6613.333

Sample: 0 HQIC 6603.052

- 1705

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 -0.7986 0.117 -6.807 0.000 -1.029 -0.569

ma.L1 0.8396 0.105 8.020 0.000 0.634 1.045

sigma2 2.8013 0.017 160.271 0.000 2.767 2.836

===================================================================================

Ljung-Box (L1) (Q): 2.02 Jarque-Bera (JB): 5344375.75

Prob(Q): 0.16 Prob(JB): 0.00

Heteroskedasticity (H): 0.29 Skew: -10.32

Prob(H) (two-sided): 0.00 Kurtosis: 276.58

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

train_pred = model_fit.predict(typ='levels')

# 预测测试集数据

test_pred = model_fit.forecast(steps=len(test_df))

# 输出训练集和测试集的预测数据

print("训练集预测数据:\n", train_pred)

print("测试集预测数据:\n", test_pred)

output

训练集预测数据:

Date

2015-01-05 0.000000

2015-01-06 76.160008

2015-01-07 73.639795

2015-01-08 73.473245

2015-01-09 70.935963

...

2021-12-27 49.766963

2021-12-28 50.031091

2021-12-29 50.863590

2021-12-30 50.812922

2021-12-31 50.391148

Name: predicted_mean, Length: 1705, dtype: float64

测试集预测数据:

1705 50.425828

1706 50.413187

1707 50.423283

1708 50.415220

1709 50.421659

...

2028 50.418800

2029 50.418800

2030 50.418800

2031 50.418800

2032 50.418800

Name: predicted_mean, Length: 328, dtype: float64

# 可视化训练集和测试集的实际数据和预测数据

plt.figure(figsize=(12,6))

plt.plot(train_df.index, train_df.values, label='训练数据')

plt.plot(train_df.index, train_pred.values, label='训练数据预测值')

plt.plot(test_df.index, test_df.values, label='测试数据')

plt.plot(test_df.index, test_pred.values, label='测试数据预测值')

plt.legend()

plt.title('ARIMA(1,1,1)模型拟合结果')

plt.xlabel('日期')

plt.ylabel('收盘价格')

plt.show()

思考:ARIMA在训练集上拟合的比较好,但在测试集上,所有的预测值几乎都相等,为什么?问题出在哪?怎么解决?

2.8 模型评价

2.8.1 计算评估指标

为了评估模型的预测效果,我们需要计算一些常用的评估指标,包括均方误差(Mean Squared Error,MSE)、均方根误差(Root Mean Squared Error,RMSE)、平均绝对误差(Mean Absolute Error,MAE)和平均绝对百分误差(Mean Absolute Percentage Error,MAPE)等。

这些指标的计算公式如下:

M S E = 1 n ∑ i = 1 n ( y i − y ^ i ) 2 MSE = \frac{1}{n} \sum_{i=1}^{n}(y_i - \hat{y}_i)^2 MSE=n1i=1∑n(yi−y^i)2

R M S E = M S E RMSE = \sqrt{MSE} RMSE=MSE

M A E = 1 n ∑ i = 1 n ∣ y i − y ^ i ∣ MAE = \frac{1}{n} \sum_{i=1}^{n}|y_i - \hat{y}_i| MAE=n1i=1∑n∣yi−y^i∣

M A P E = 1 n ∑ i = 1 n ∣ y _ i − y ^ i y i ∣ × 100 MAPE = \frac{1}{n} \sum_{i=1}^{n}|\frac{y\_i - \hat{y}_i}{y_i}| \times 100% MAPE=n1i=1∑n∣yiy_i−y^i∣×100

其中, y i y_i yi 表示真实值, y ^ i \hat{y}_i y^i 表示预测值, n n n 表示样本数量。

代码如下:

# 计算评估指标

mse = mean_squared_error(test_df.values, test_pred.values)

rmse = np.sqrt(mse)

mae = mean_absolute_error(test_df.values, test_pred.values)

mape = np.mean(np.abs((test_df.values - test_pred.values) / test_df.values)) * 100

# 打印评估指标

print('MSE: %.2f' % mse)

print('RMSE: %.2f' % rmse)

print('MAE: %.2f' % mae)

print('MAPE: %.2f%%' % mape)

output

MSE: 33.86

RMSE: 5.82

MAE: 4.92

MAPE: 11.28%

- 接下来,我们可以

绘制模型的残差图(Residual Plot),来评估模型是否存在系统性误差。如果模型的残差是随机的、没有规律性,那么说明模型拟合得比较好;如果残差呈现出一定的规律性,那么说明模型还存在一些问题。

2.8.2 残差检验

(1) 绘制残差图

# 计算训练集和测试集的残差

train_resid = train_df['Close'] - train_pred.values

test_resid = test_df['Close'] - test_pred.values

# 绘制训练集和测试集的残差图

plt.figure(figsize=(12,10))

plt.subplot(211)

plt.plot(train_resid)

plt.title('训练数据残差图')

plt.xlabel('年份')

plt.ylabel('残差')

plt.subplot(212)

plt.plot(test_resid)

plt.title('测试数据残差图')

plt.xlabel('年份')

plt.ylabel('残差')

plt.show()

(2) 对残差进行平稳性检验

# 对训练集残差进行平稳性检验

result3 = sm.tsa.stattools.adfuller(train_resid)

print('训练集残差ADF检验结果:')

print('ADF Statistic: %f' % result3[0])

print('p-value: %f' % result3[1])

print('Critical Values:')

for key, value in result3[4].items():

print('\t%s: %.3f' % (key, value))

# 对测试集残差进行平稳性检验

result4 = sm.tsa.stattools.adfuller(test_resid)

print("")

print('测试集残差ADF检验结果:')

print('ADF Statistic: %f' % result4[0])

print('p-value: %f' % result4[1])

print('Critical Values:')

for key, value in result4[4].items():

print('\t%s: %.3f' % (key, value))

output

训练集残差ADF检验结果:

ADF Statistic: -7.788862

p-value: 0.000000

Critical Values:

1%: -3.434

5%: -2.863

10%: -2.568

测试集残差ADF检验结果:

ADF Statistic: -1.734568

p-value: 0.413396

Critical Values:

1%: -3.451

5%: -2.870

10%: -2.572

根据结果,训练集残差ADF 统计量为-8.386454,远小于 1% 的临界值-3.616,因此我们可以拒绝原假设(序列具有单位根非平稳性),接受备择假设,即序列是平稳的。 P 值为 0,说明序列的单位根非常显著地低于 5% 的显著性水平,进一步支持序列的平稳性。

2.9 小结

对某股票的历史股价数据进行时序分析和预测,具体步骤如下:

-

1.首先加载相应的包

-

2.数据的读取和初步探索

-

3.平稳性检验

-

4.确定差分阶数

-

5.通过自相关图和偏自相关图来确定拟合模型

-

6.拟合ARIMA模型并进行预测

-

7.对预测结果进行评估

本次分析表明,ARIMA模型可以用于股票价格的预测。但是,在实际应用中需要注意,股票价格受到多种因素的影响,仅使用历史价格数据进行预测是不够准确的,需要考虑其他因素的影响。此外,ARIMA模型的预测精度也会受到模型参数的选择和数据质量的影响,需要进行不断的调整和优化。

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言