稀疏组套索

So yesterday I launched a new package for python: asgl (the name comes from Adaptive Sparse Group Lasso) that adds a lot of features that were already available in R packages but not in python, like solving sparse group lasso models, and goes beyond that, adding extra features that improve the results that sparse group lasso can provide.

所以昨天我为python启动了一个新软件包: asgl (名称来自Adaptive Sparse Group Lasso),它添加了许多R包中已经可用但python中没有的功能,例如解决稀疏组lasso模型,并且超出了此范围,添加了额外的功能来改善稀疏组的结果套索可以提供。

This is going to be the first article on a series about state-of-the-art regularization techniques in regression, and I would like to start talking about the sparse group lasso: what is it and how to use it. Specifically, here we will see:

这将是有关回归的最新正则化技术系列的第一篇文章,我想开始谈论稀疏组套索:它是什么以及如何使用它。 具体来说,在这里我们将看到:

What is sparse group lasso

什么是稀疏组套索

How to use sparse group lasso in python

如何在python中使用稀疏组套索

How to perform k-fold cross validation

如何执行K折交叉验证

How to use grid search in order to find the optimal solution.

如何使用网格搜索以找到最佳解决方案。

什么是稀疏组套索 (What is sparse group lasso)

To understand what is sparse group lasso we need to talk (briefly) about two techniques: lasso and group lasso. Given a risk function, for example the linear regression risk,

要了解什么是稀疏组套索,我们需要(简要地)谈论两种技术: 套索和套索套索 。 给定风险函数,例如线性回归风险,

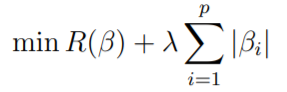

Lasso: is defined by adding a penalization on the absolute value of the β coefficients,

套索:通过对β系数的绝对值加罚分来定义,

最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

3万+

3万+

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言