OLS估计

import statsmodels.api as sm

import numpy as np

import matplotlib.pyplot as plt

from statsmodels.sandbox.regression.predstd import wls_prediction_std

%matplotlib inline

np.random.seed(9876789)

#生成实验数据

nsample = 100

x = np.linspace(0, 10, 100)

X = np.column_stack((x, x**2))

beta = np.array([1, 0.1, 10])

e = np.random.normal(size=nsample)

#ols模型需要的X矩阵需要加入常数项

X = sm.add_constant(X)

y = np.dot(X, beta)+e

#OLS拟合实验数据

model = sm.OLS(y, X)

results = model.fit()

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 1.000

Model: OLS Adj. R-squared: 1.000

Method: Least Squares F-statistic: 4.020e+06

Date: Thu, 19 Dec 2019 Prob (F-statistic): 2.83e-239

Time: 17:33:16 Log-Likelihood: -146.51

No. Observations: 100 AIC: 299.0

Df Residuals: 97 BIC: 306.8

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 1.3423 0.313 4.292 0.000 0.722 1.963

x1 -0.0402 0.145 -0.278 0.781 -0.327 0.247

x2 10.0103 0.014 715.745 0.000 9.982 10.038

==============================================================================

Omnibus: 2.042 Durbin-Watson: 2.274

Prob(Omnibus): 0.360 Jarque-Bera (JB): 1.875

Skew: 0.234 Prob(JB): 0.392

Kurtosis: 2.519 Cond. No. 144.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

#OLS模型中含有的属性和方法

print(dir(results))

['HC0_se', 'HC1_se', 'HC2_se', 'HC3_se', '_HCCM', '__class__', '__delattr__', '__dict__', '__dir__', '__doc__', '__eq__', '__format__', '__ge__', '__getattribute__', '__gt__', '__hash__', '__init__', '__init_subclass__', '__le__', '__lt__', '__module__', '__ne__', '__new__', '__reduce__', '__reduce_ex__', '__repr__', '__setattr__', '__sizeof__', '__str__', '__subclasshook__', '__weakref__', '_cache', '_data_attr', '_get_robustcov_results', '_is_nested', '_wexog_singular_values', 'aic', 'bic', 'bse', 'centered_tss', 'compare_f_test', 'compare_lm_test', 'compare_lr_test', 'condition_number', 'conf_int', 'conf_int_el', 'cov_HC0', 'cov_HC1', 'cov_HC2', 'cov_HC3', 'cov_kwds', 'cov_params', 'cov_type', 'df_model', 'df_resid', 'diagn', 'eigenvals', 'el_test', 'ess', 'f_pvalue', 'f_test', 'fittedvalues', 'fvalue', 'get_influence', 'get_prediction', 'get_robustcov_results', 'initialize', 'k_constant', 'llf', 'load', 'model', 'mse_model', 'mse_resid', 'mse_total', 'nobs', 'normalized_cov_params', 'outlier_test', 'params', 'predict', 'pvalues', 'remove_data', 'resid', 'resid_pearson', 'rsquared', 'rsquared_adj', 'save', 'scale', 'ssr', 'summary', 'summary2', 't_test', 't_test_pairwise', 'tvalues', 'uncentered_tss', 'use_t', 'wald_test', 'wald_test_terms', 'wresid']

#这里只看看系数和R2

print('Parameters: ', results.params)

print('R2: ', results.rsquared)

Parameters: [ 1.1875799 0.06751355 10.00087227]

R2: 0.9999904584846492

OLS非线性曲线,但参数是线性的

nsample = 50

sig = 0.5

x = np.linspace(0, 20, nsample)

X = np.column_stack((x, np.sin(x), (x-5)**2, np.ones(nsample)))

beta = [0.5, 0.5, -0.02, 5.]

y_true = np.dot(X, beta)

y = y_true + sig * np.random.normal(size=nsample)

res = sm.OLS(y, X).fit()

print(res.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.946

Model: OLS Adj. R-squared: 0.942

Method: Least Squares F-statistic: 267.0

Date: Thu, 19 Dec 2019 Prob (F-statistic): 4.28e-29

Time: 17:39:35 Log-Likelihood: -29.585

No. Observations: 50 AIC: 67.17

Df Residuals: 46 BIC: 74.82

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.5031 0.024 20.996 0.000 0.455 0.551

x2 0.5805 0.094 6.162 0.000 0.391 0.770

x3 -0.0208 0.002 -9.908 0.000 -0.025 -0.017

const 5.0230 0.155 32.328 0.000 4.710 5.336

==============================================================================

Omnibus: 3.931 Durbin-Watson: 2.004

Prob(Omnibus): 0.140 Jarque-Bera (JB): 2.119

Skew: -0.235 Prob(JB): 0.347

Kurtosis: 2.108 Cond. No. 221.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

print('Parameters: ', res.params)

print('Standard errors: ', res.bse)

print('Predicted values: ', res.predict())

Parameters: [ 0.50314123 0.58047691 -0.02084597 5.02303139]

Standard errors: [0.02396328 0.09420248 0.00210399 0.15537883]

Predicted values: [ 4.50188223 5.01926399 5.49184506 5.88798995 6.18748025 6.38483648

6.49021831 6.52775537 6.53158285 6.54023313 6.59030507 6.7104509

6.91666871 7.20967408 7.57478245 7.98432176 8.40217892 8.78973307

9.11220088 9.34435135 9.47465119 9.50715972 9.46086192 9.36654926

9.26176075 9.18461538 9.16754929 9.23198657 9.3848194 9.61727563

9.90636005 10.21863244 10.51570167 10.7605333 10.92353419 10.98741461

10.95002886 10.82472782 10.63816544 10.42591956 10.22664657 10.0757303

9.99946853 10.01075234 10.10694816 10.27033045 10.47099394 10.67176702

10.83431887 10.92545718]

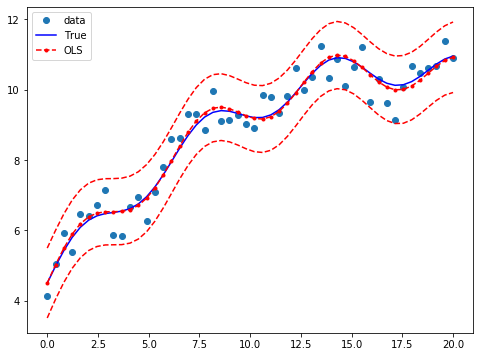

为了对比 真实值与OLS预测值,使用 wls_prediction_std

from statsmodels.sandbox.regression.predstd import wls_prediction_std

#标准差预测值, 置信区间下界限, 置信区间上界限

prstd, iv_l, iv_u = wls_prediction_std(res)

fig, ax = plt.subplots(figsize=(8,6))

ax.plot(x, y, 'o', label="data")

ax.plot(x, y_true, 'b-', label="True")

ax.plot(x, res.predict(), 'r--.', label="OLS")

ax.plot(x, iv_u, 'r--')

ax.plot(x, iv_l, 'r--')

ax.legend(loc='best');

虚拟变量处理

dummy = sm.categorical(groups, drop=True)

import numpy as np

import statsmodels.api as sm

groups = np.array(['a', 'b', 'a', 'a', 'c'])

sm.categorical(groups)

array([['a', '1.0', '0.0', '0.0'],

['b', '0.0', '1.0', '0.0'],

['a', '1.0', '0.0', '0.0'],

['a', '1.0', '0.0', '0.0'],

['c', '0.0', '0.0', '1.0']], dtype='<U32')

sm.categorical(groups, drop=True)

array([[1., 0., 0.],

[0., 1., 0.],

[1., 0., 0.],

[1., 0., 0.],

[0., 0., 1.]])

x = np.array([1, 2, 3, 4, 5])

dummy = sm.categorical(groups, drop=True)

np.column_stack((x, dummy))

array([[1., 1., 0., 0.],

[2., 0., 1., 0.],

[3., 1., 0., 0.],

[4., 1., 0., 0.],

[5., 0., 0., 1.]])

共线性问题

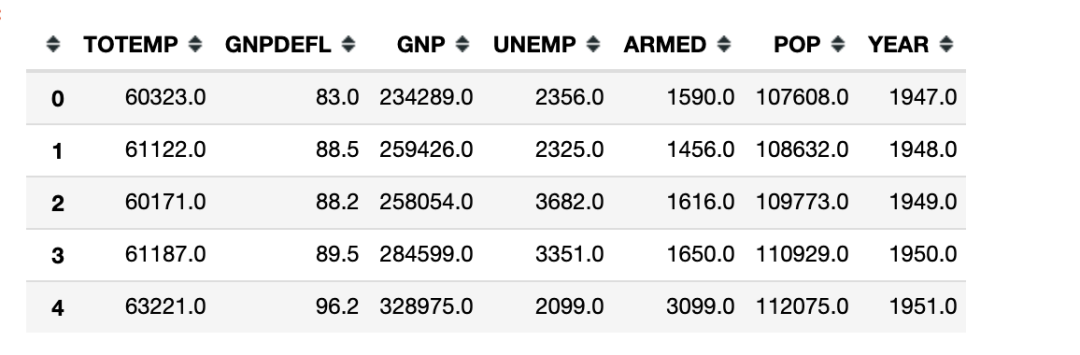

数据集Longley是众所周知的拥有强共线性现象的数据集,也就是自变量之间拥有较高的相关性。

因变量TOTEMP

自变量

GNPDEFL

GNP

UNEMP

ARMED

POP

YEAR

共线性问题会影响ols参数估计的稳定性。

import pandas as pd

df = pd.read_csv('data/longley.csv')

df.head()

import statsmodels.api as sm

import pandas as pd

df = pd.read_csv('data/longley.csv')

X = df[df.columns[1:]]

X = sm.add_constant(X)

y = df[df.columns[0]]

ols = sm.OLS(y, X)

ols_results = ols.fit()

print(ols_results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: TOTEMP R-squared: 0.995

Model: OLS Adj. R-squared: 0.992

Method: Least Squares F-statistic: 330.3

Date: Thu, 19 Dec 2019 Prob (F-statistic): 4.98e-10

Time: 19:52:43 Log-Likelihood: -109.62

No. Observations: 16 AIC: 233.2

Df Residuals: 9 BIC: 238.6

Df Model: 6

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -3.482e+06 8.9e+05 -3.911 0.004 -5.5e+06 -1.47e+06

GNPDEFL 15.0619 84.915 0.177 0.863 -177.029 207.153

GNP -0.0358 0.033 -1.070 0.313 -0.112 0.040

UNEMP -2.0202 0.488 -4.136 0.003 -3.125 -0.915

ARMED -1.0332 0.214 -4.822 0.001 -1.518 -0.549

POP -0.0511 0.226 -0.226 0.826 -0.563 0.460

YEAR 1829.1515 455.478 4.016 0.003 798.788 2859.515

==============================================================================

Omnibus: 0.749 Durbin-Watson: 2.559

Prob(Omnibus): 0.688 Jarque-Bera (JB): 0.684

Skew: 0.420 Prob(JB): 0.710

Kurtosis: 2.434 Cond. No. 4.86e+09

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 4.86e+09. This might indicate that there are

strong multicollinearity or other numerical problems.

summary末尾Warnings提醒我们模型的condition number很大,可能存在很强的多重共线性问题或者其他问题

Condition number

condition number可以用来评估多重共线性问题的大小。

当该值大于20, 基本可以确定是存在多重共线性问题(参考Greene 4.9)

import numpy as np

np.linalg.cond(ols.exog)

4859257015.454868

删除观测值

Greene也指出即使移除一个观测值,也可能会对ols估计产生巨大的影响

#保留了前14个观测值

ols_results2 = sm.OLS(y[:14], X[:14]).fit()

print("Percentage change %4.2f%%\n"*7 % tuple([i for i in (ols_results2.params - ols_results.params)/ols_results.params*100]))

Percentage change 4.55%

Percentage change -105.20%

Percentage change -3.43%

Percentage change 2.92%

Percentage change 3.32%

Percentage change 97.06%

Percentage change 4.64%

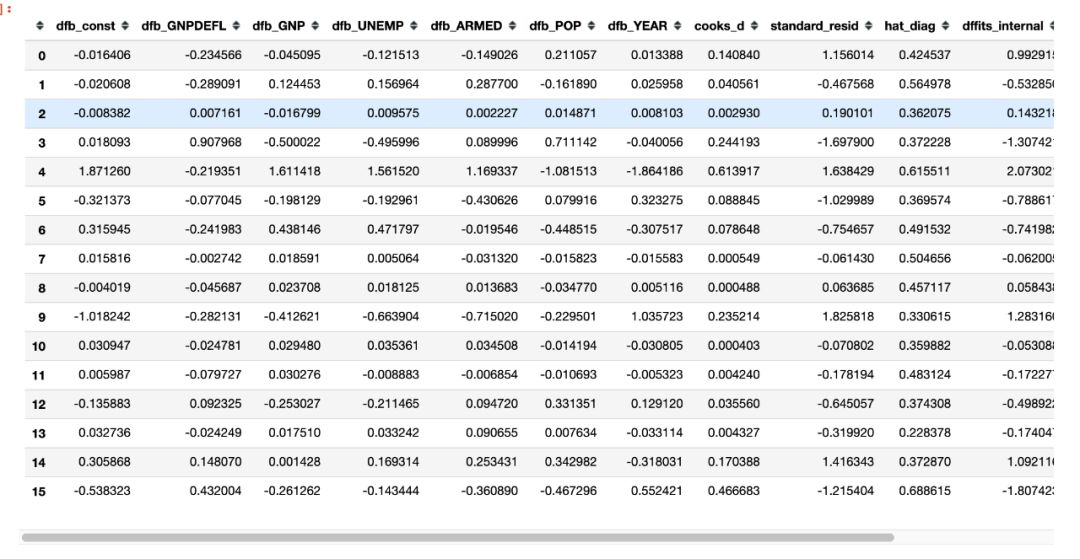

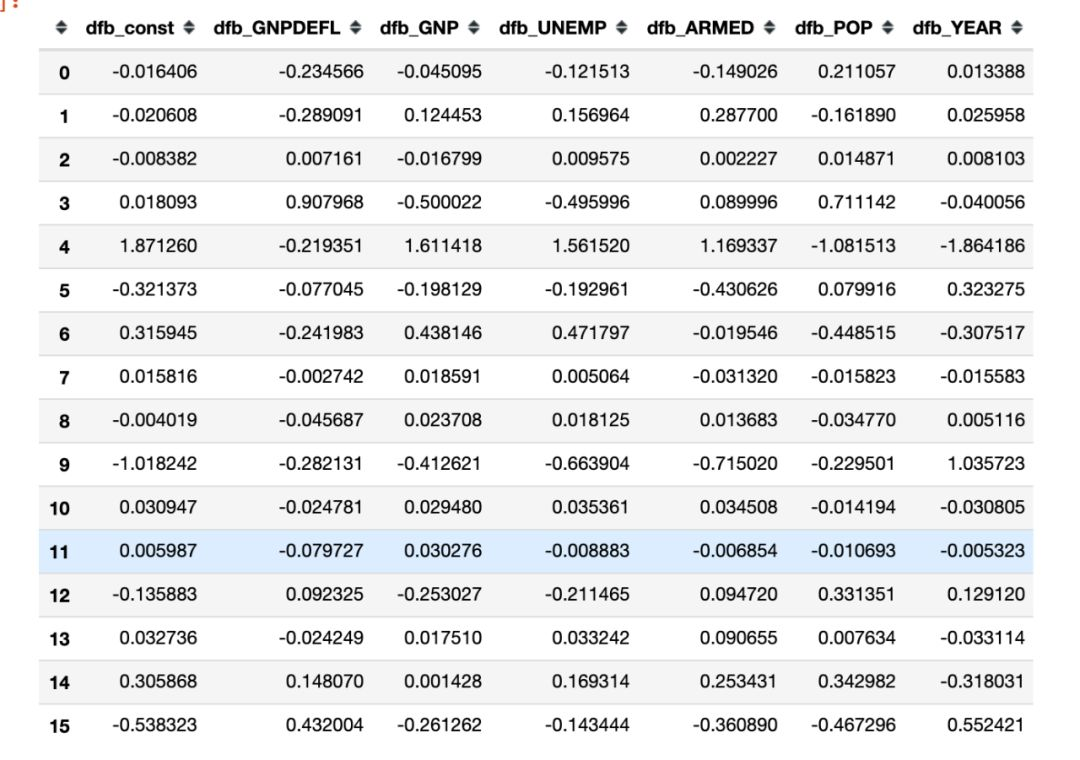

我们也可以查看DFBETAS,即当移除某个观测值后,每个参数的会因此发生的改变(标准化)

We can also look at formal statistics for this such as the DFBETAS – a standardized measure of how much each coefficient changes when that observation is left out.

influence = ols_results.get_influence()

influence.summary_frame()

大致上,我们可以认为DBETAS的绝对值大于

2./(len(X)**.5)

0.5

# 保留含有dfb的字段名

influence.summary_frame().filter(regex="dfb")

现在statsmodels正在持续开发中,未来python的计量分析方面的应用会越来越好用,期待ing

近期文章

情绪及色彩词典获取方式,请在公众号后台回复关键词“20191220” ,

如果想做文本分析

4009

4009

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言