I. Background Information

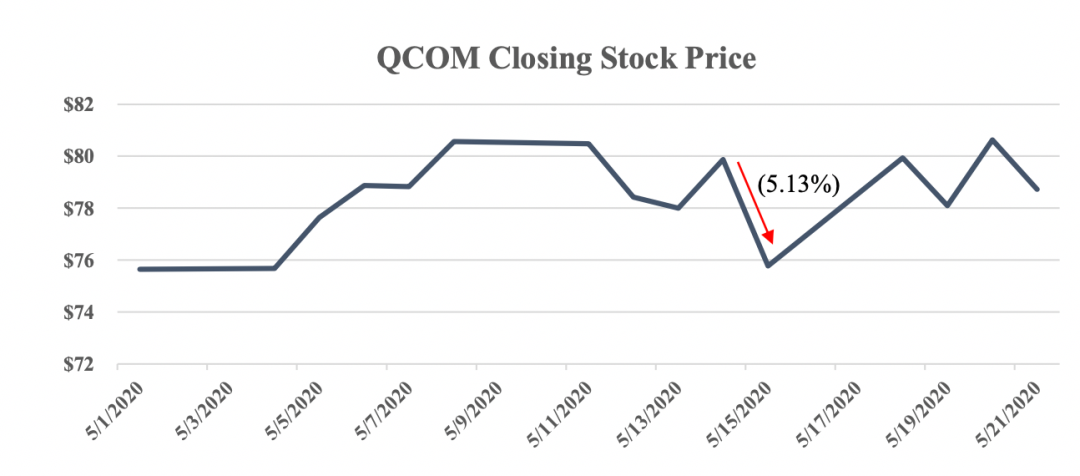

On May 15, 2020, Qualcomm (QCOM) closed at $75.77, down 5.1% from the previous day. On the same day, the S&P 500 was up 0.4%. The decline was driven by renewed China/U.S. tensions stemming from the announcement of new export restrictions placed on China-based Huawei. Since these restrictions were announced, semiconductor manufacturer TSMC has stopped taking new Huawei orders. China is expected to retaliate by placing specific U.S. companies on its unreliable entity list. This includes not only QCOM but also Apple, Cisco, and Boeing. As a result, QCOM is expected to take a significant revenue hit if China follows through on these actions. The company is relying on Chinese OEMs as part of its worldwide 5G rollout as well as the significant manufacturing processes in the country.

QCOM’s drop indicates that Wall Street took the retaliation rumors seriously and priced in the possibility of new action. Since then, QCOM has recovered the loss. While no action has been taken yet, retaliatory action may still occur sometime in the future. The Trump Administration has repeatedly blamed China for its role in the COVID-19 pandemic and is likely to pursue further action through tariffs or action against Chinese companies.

II. Business Model

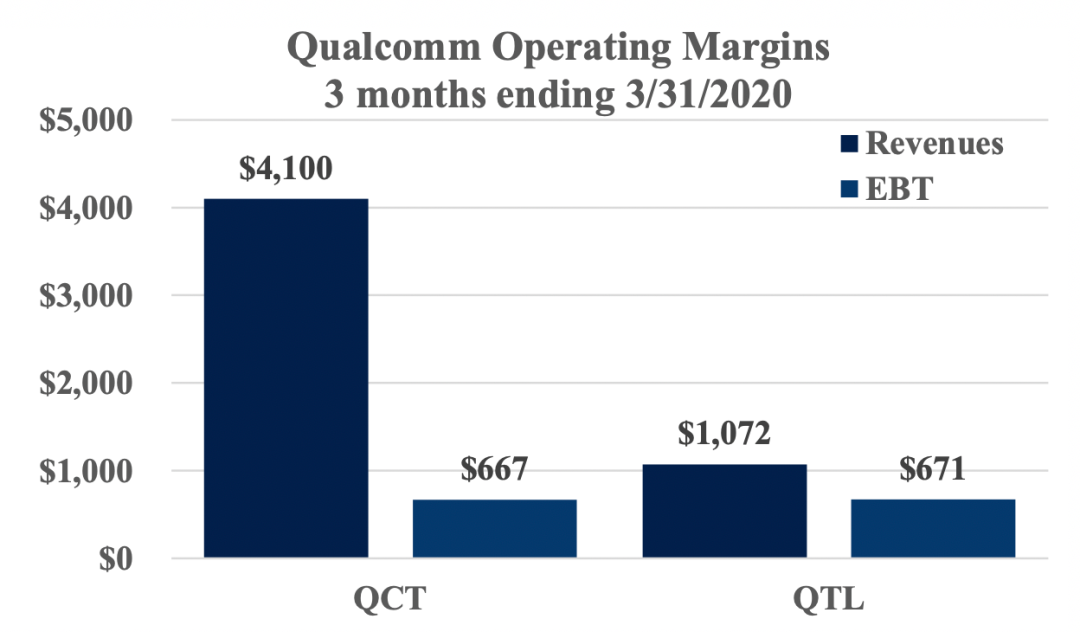

QCOM is split into 2 main divisions: QTC and QLT. QTC is responsible for design and manufacturing of chips that it sells to OEMs. QTC does not manufacture the chips themselves but contracts out to foundries such as Samsung and TSMC. QLT licenses QCOM patented technology to third-parties that use it within their devices. Most notable patents include CDMA, 3G, 4G, and 5G.

QTC is responsible for a larger share of the revenue but operates on much lower margins because it incurs costs for the production of chips. Thus, a majority of net income is attributable to QLT. The difference in the two segments is significant in how Chinese restrictions would affect QCOM. Restrictions placed on chip selling would have a large impact on revenue but a much lower impact on net income. Conversely, restrictions on license royalties would affect net income at a much higher rate.

III. Revenue-side Impact

Currently, QCOM provides chips to the majority of Chinese OEMs, excluding Huawei. This includes OPPO, vivo, Xiaomi, and others. Combined revenues from OPPO, vivo, and affiliates comprised at least 10% of total revenue in 2019. QCOM entered into a new patent agreement, effective April 1, 2020, with OPPO and vivo which covers 3G/4G/5G devices. Revenues from Xiaomi also comprised at least 10% of total revenue in 2019. In 2018, QCOM stopped supplying Huawei with chips, leading Huawei to develop their own HiSilicon chipset. QLT still licenses to Huawei, though their previous license agreement ended December 31, 2019. Due to an FTC ruling, Huawei has been allowed to continue to use QCOM patents without reaching a new agreement. It is still uncertain how restrictions will affect patent royalties but it seems expected that direct chip selling to Chinese OEMs would be disallowed. If both are affected, QCOM may lose >20% revenue from OPPO, vivo and Xiaomi. They would also be unable to recover lost revenue from Huawei.

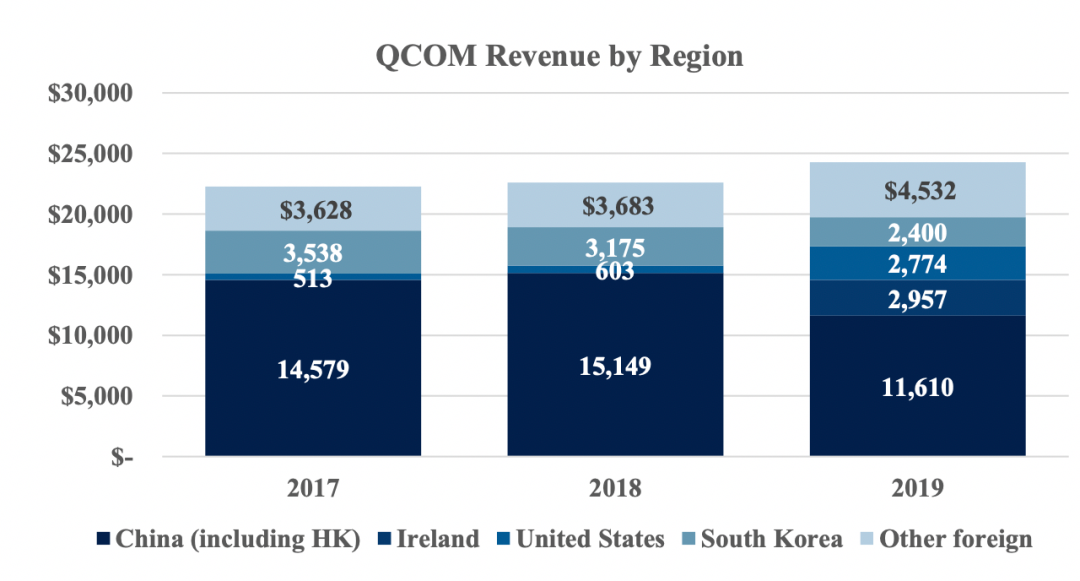

Since 2018, QCOM has significantly reduced China exposure after initial restrictions were placed on Huawei, moving processes previously in China to the U.S. and Ireland. In FY2019, China accounted for approximately 49% of total QCOM revenue. This figure includes products that were manufactured in China and royalty revenues from licensees with invoice addresses in China. However, since this figure includes products that are manufactured in China but not sold within the country, it overestimates real China demand by Chinese OEMs.

A revenue decrease of 49% presents a worst case scenario for QCOM, but actual impact to revenue would likely be between around 32% . Since foreign companies such as Apple and Samsung manufacture in China, they are included in China revenue to QCOM. However, they would not switch away from QCOM chips. For Chinese OEMs, it is unlikely that domestic chips designers would be able to match the quality of QCOM. To compete with Huawei, many of these companies have no choice but to use QCOM. Huawei is the only notable Chinese competitor to QCOM but its manufacturing capacity is limited by new U.S. restrictions. However, a large impact revenue does not translate to a large impact on net income. Since QLT operates on much higher margins than QTC, impacts on QCOM’s chip selling business would not have a large impact on net income.

IV. Supply-side Impact

QCOM lists its main manufacturers as Global Foundries (GF), Samsung Electronics, Semiconductor Manufacturing International (SMIC), Taiwan Semiconductor Manufacturing Company (TSMC) and United Microelectronics (UMC) with a majority of foundries located in the Asia/Pacific Region. Currently, most of QCOM’s chips are manufactured by Samsung and TSMC. Samsung operates 3 foundries, 2 located in South Korea and a third in Austin, Texas. TSMC operates 17 total foundries with 2 located in China. Since supply lines are located largely outside mainland China, there will probably be minimal impact on QCOM’s ability to supply chips. QCOM’s low reliance on China makes it more vulnerable to retaliation compared to other U.S. companies such as Apple and Tesla.

V. Future Outlook

Qualcomm is resilient to future impacts because of the significant portion of net income that is derived from its licensing business. The technology that it has developed in 4G and now 5G is not easily replaced and manufacturers will rely on the company. Its competitors are still limited, allowing QCOM to maintain its market share. While Huawei has developed a 5G modem, it is limited by the production capabilities of Chinese semiconductor manufacturers. Smartphone 5G is complicated and even established companies may not find success. In 2019, Intel exited the smartphone 5G business after finding little success, focusing its efforts on other 5G infrastructure. Companies like Apple are beginning to develop their own 5G technology but those efforts are still years away. Until then, they will all have to rely on QCOM.

VI. Conclusion

While the worst case scenario could lead to a 32% decrease in revenue, actual impact would be much lower. QCOM stock has already recovered the 5% it lost on May 15, pricing in a lower probability of China action as well as a smaller expected impact to net income. Since QCOM has decreased reliance on China significantly in the last 2 years, it is in a much better position to weather China/U.S. tensions. Despite recent tensions, QCOM is in a position for growth in the near term.

-- END -- 图片 :图片来自网络,侵删 大叔观点时间作品 | 尽情分享朋友圈

92

92

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言