Market Risk: The Road Ahead

Following the release of the latest Basel standard for market risk, the boundary between the trading book and the banking book allocations for financial instruments is now much clearer. But how will the future market risk highway change the way firms manage and account for different types of instruments?

-

For many years, financial institutions have had a difficult time figuring where, exactly, their financial instruments should be allocated. Whether an instrument should be accounted for in the trading book or the banking book was unclear, thanks in large part to malleable regulation on market risk. But this is about to change – dramatically.

-

The Basel Committee on Banking Supervision (BCBS) recently released its long-awaited final standard for the minimum capital requirements for market risk – complete with clear instructions of the allocation of financial instruments to either the banking book or the trading book.

-

What sets this standard apart is that it uses a new “modular format” that the BCBS will also use for future standards. The section on the boundary between the trading book and the banking book, for example, is coded as “RBC25”; the standardized approach is coded “MAR20” to “MAR23,” while the internal models approach is referred to as “MAR30” to “MAR33.” Similar codes will be applied in future BCBS standards for credit risk and operational risk, so that these all fit like pieces of a jigsaw puzzle in a future comprehensive framework.

-

Basel II’s flexible definition of the boundary left ample room for arbitrage. Indeed, the trading book/banking book allocation rules were quite open to interpretation, and firms took advantage of this weakness by moving instruments toward the book with the lowest capital requirements. The BCBS has therefore been keen to replace the Basel II trading book/banking book boundary with a more intractable one.

-

The new BCBS standard provides a clear framework for the boundary between trading book and banking book, although one probably needs to read the articles in the section RBC25 multiple times to get a proper understanding of the demarcation. For example, when trading assets are held for short-term resale while there’s a legal impediment against hedging them, should they be accounted for in the banking book or the trading book?

-

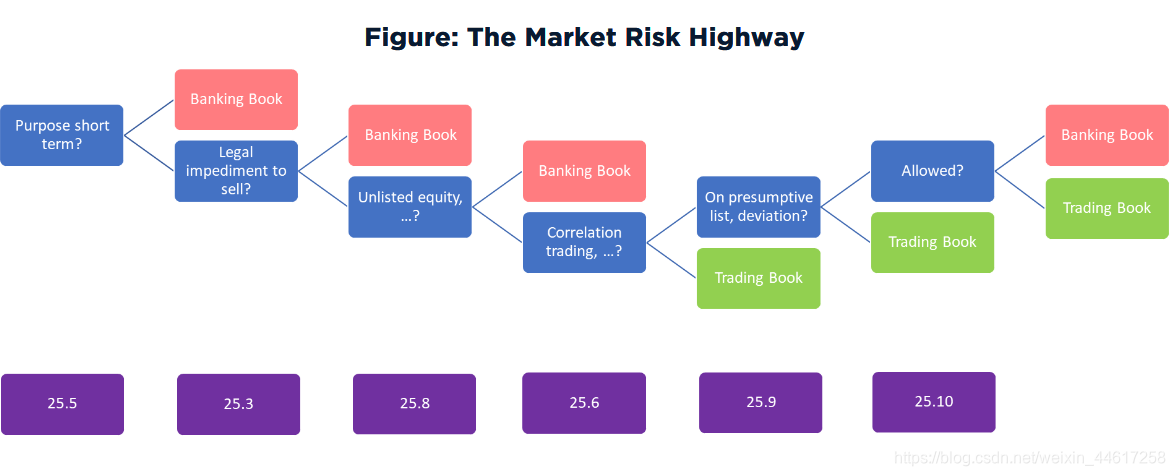

To understand the reasoning adopted by the BCBS and to provide more clarity about the trading book/ banking book criteria, take a look at the following diagram:

- In the diagram, the decision nodes are blue and the final branches either pink (for definitively banking book) or green (for definitively trading book), while references to the specific articles within the RBC25 section are purple. The exact wording of the criteria need not be fully captured on our highway, because that can be extracted from the articles referred to in the purple boxes.

- The highway is an illustration for first designation. There are separate rules (see articles 14 to 17 of RBC25) about moving instruments between trading book and banking book after initial designation.

Driving on the Market Risk Highway

- So, let’s go for a ride! The navigation works in such a way that while we’re heading for the trading book, there are several off-ramps that might take us to the banking book.

- The purpose for which a bank holds a given instrument is the main criterion (see art. RBC25.5) for determining whether it gets allocated to the trading book or the banking book. If the purpose is for short-term resale, or profiting from short-term price movements, or locking in arbitrage profits, then the instrument is, in principle, a trading book instrument. The trading book is also the destination for instruments that are used to hedge risks in any of the above scenarios. Under all other circumstances, it should be allocated to the banking book.

- There are, moreover, two off-ramps toward the banking book. For an instrument to qualify for the trading book, there must not be any legal impediment (see RBC25.3) to selling or fully hedging it. This means that, if there is any such impediment, the instrument must be allocated to the banking book – even if it is meant for short-term resale.

- The second off-ramp to the banking book presents itself if the instrument is on a product list that must be included in banking book. This list contains, among others, unlisted equities, real estate holdings, retail or SME credit, and derivatives of these instruments. This means, for example, that a credit derivative that references a portfolio of SME loans and that the bank holds for the purpose of short-term resale, will end up in the banking book – even though it is a derivative and it is held for a short-term purpose.

- There are several clear-cut cases (see article RBC25.6) in which instruments will end up in the trading book. Instruments in the correlation-trading portfolio, for example, will be accounted for in the trading book.

- However, if an instrument is not on this list of clear-cut cases, but rather on the “presumptive list,” there is still a chance that it will end up in the banking book. Items on this presumptive list include instruments held as accounting trading assets and liabilities, instruments resulting from market-making activities, and listed equities.

- That said, if a firm wants to designate any of these instruments to the banking book, it first must pass an important toll-gate: supervisory approval. Article RBCS25.10 states that a bank must submit a request to its supervisor, and receive explicit approval for a banking book designation, for instruments on the presumptive list.

Parting Thoughts

- The publication of the BCBS standard #d457 is an important step forwards toward the review of the trading book treatment. An important issue – the demarcation of the boundary between trading book and banking book – has been clarified.

- The standard will come into effect on January 1, 2022, and banks will need a roadmap to implement the new market risk treatment. Understanding the “highway” outlined in this article is a good first step.

市场风险:前方的路

主旨:随着最近刚刚公布的最新巴塞尔市场风险标准,金融产品在banking book 以及 trading book的界定逐渐地清晰起来。但是未来的市场风险的高速发展又将如何改变公司对不同种类金融工具的管理呢?

-

金融机构对于自身的金融工具应该如何匹配存在多年的困扰。到底是属于banking book 还是 trading book 并不能明确区分,幸好关于市场风险的规定弹性比较大,但是这种情况戏剧性地将要改变。

-

巴塞尔委员会银行业监管分部最近公布了市场风险最小资本要求的最终标准,明确了金融工具的划分问题

-

这个最终标准使用了新的“模块化格式”区别于以往,并将此应用于未来的标准。比如说,MAR20 到 MAR23规定了SA标准法,RBC25部分规定了trading book 和 banking book 的区分,IMA 内部模型法在MAR30 到 MAR33之间。相类似的代号也将会应用在BCBS未来的信用风险标准以及操作风险标准,因此在未来全面的框架下将是如智力拼图一样的模块。

-

当然最重要的是新的最终标准明确了标准法以及内部模型法计算市场风险最低要求资本的方法,以及明确区分banking book 以及trading book的界限

-

巴塞尔 2的弹性定义放大了监管套利的空间。确实,交易帐与银行账有开放性诠释的空间,许多公司利用这种弱点,把银行账转到交易帐用来降低资本要求。BCBS一直尝试替代巴塞尔2中的界定,用一种更明确的方式

-

新的BCBS标准为交易站与银行账的界限提供了更明确的框架,尽管必须反复阅读RBC25部分文章很多遍才能正确理解界限框架。举例来说,当交易资产短期持有预备转售的情况下,然而对冲该种资产又存在法律上的阻碍,那么,这样的资产到底是属于交易帐还是银行账呢?

-

为了更进一步理解BCBS制度设计意图以及提供更明确的银行账交易帐标准,看下下面的图:

-

在上图中,决策点为蓝色,而终分支要么是粉色(银行账),要么是绿色(交易帐),在RBC25中各个条款为紫色。具体的描述就不在本文当中赘述了,因为可以直接从巴塞尔的文章中找到。

-

这仅仅只是首次定义的举例而已,首次定义后还有更多的分支关于在交易帐还是银行账之间区分的工具

行走在市场风险的高速路上

- 那么,让我们来一场兜风吧!导航的工作机制是,当我们往交易帐出发的时候,总有一些岔道将我们引向银行账。

- 银行持有金融工具的目的是主要的标准,用来决定到底划分到银行账还是交易帐。如果目的是短期斥候转售的,或者是意图从短期价格波动中获利的,原则上来说,是一个交易帐工具。那些用来对冲风险目的持有的工具也应当划分在交易帐中。在其他的目的下,都应该划分在银行账之中。

- 这其中存在两个岔道,有可能该工具会被划分到银行账。首先如果一个交易帐工具的卖出以及全对冲存在法律合规上的阻碍时,那么该工具将被划分到银行账之中去。

- 其次,第二的岔道会导致该工具划分到银行账中去的是,该工具被明确写在必须包含在银行账之中的工具名单中。该名单包括,未列明股票,实体资产持有,零售或者中小企业信用,以及上述这些工具的衍生工具。这意味着,举例来说,一个关于中小企业贷款的投资组合的信用衍生品,银行为了转售而短期持有,将被记录在银行账之中,尽管是衍生品,同时也是短期持有的目的。

- 存在几个明确的案例,某些资产应当被划分为交易帐的。相关性交易投资组合的工具应当被划分在交易书当中。

- 然而,一个不在名单上的明确案例,而是在假定名单,其依然有一定可能被划分到银行账中去。这个假设名单中的金融工具包括交易资产负债审计工具,因做市商行为而持有的工具,未列明股票等等。

- 因此说,如果一家机构想要让这些“待定的工具“被划分到银行账上,首先必须通过一个重要的关卡,监管审核。RBC25.1说明了,一个银行必须提交其监管者请求,并受到明确的同意答复,才可以把工具划分到银行账中去

一些想法:

- BCBS 标准 #d457的出版是对交易帐划分重新审视的重要一步。交易帐与银行账的划分被明确下来。

- 这个标准即将在2022年1月1日产生效果,而在此之前,银行必须寻找到途径完成新的市场风险监管。理解本文提出的高速公路概念将是一个好开始。

1266

1266

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言