【2024-08-05更新】修正了代码注释和图标的中文格式,增加各选项下结果可视化,Excel表格格式见文末,注意要和代码放在同一文件夹下!

完整代码

首先给出完整代码:

% 运行之前注意保存已有数据

clc; clear;

close all;

% 是否强制确定ARIMA模型(不理想的情况下选择1)

% 值为0时会自动确定模型,但结果可能不理想

isKill = 1;

% 预测时间长度

PreTime = 100;

% 是否进行新时间段的预测,建议先用0再用1

isPre = 1;

% 导入数据集

data = readtable('data.xlsx');

y = data.Value;

% 拆分数据集为训练集和测试集

train_size = floor(0.8 * length(y));

train_data = y(1:train_size);

if isPre == 1

train_data = y;

end

test_data = y(train_size+1:end);

% 平稳性检验 - ADF检验

[h_adf, p_adf] = adftest(y);

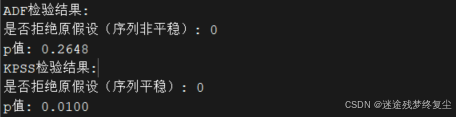

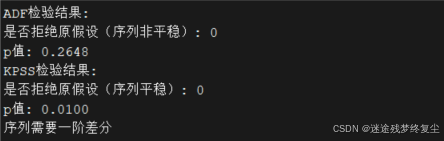

fprintf('ADF检验结果:\n');

fprintf('是否拒绝原假设(序列非平稳): %d\n', h_adf);

fprintf('p值: %.4f\n', p_adf);

% 平稳性检验 - KPSS检验

[h_kpss, p_kpss] = kpsstest(y);

fprintf('KPSS检验结果:\n');

fprintf('是否拒绝原假设(序列平稳): %d\n', ~h_kpss);

fprintf('p值: %.4f\n', p_kpss);

% 确定d参数

if isKill == 0

% 根据ADF和KPSS检验结果确定d参数

if h_adf == 1 && h_kpss == 0

d = 0;

disp('序列已经平稳')

elseif h_adf == 0 && h_kpss == 1

d = 1;

disp('序列需要一阶差分')

elseif h_adf == 1 && h_kpss == 1

d = 2;

disp('序列需要二阶差分')

else

error('无法确定d参数');

end

% 差分处理

if d > 0

y_diff = diff(train_data, d);

else

y_diff = train_data;

end

else

y_diff = train_data;

end

% 确定p和q参数

figure

subplot(2,1,1)

autocorr(y_diff)

title('自相关函数')

xlabel('滞后')

ylabel('自相关系数')

subplot(2,1,2)

parcorr(y_diff)

title('偏自相关函数')

xlabel('滞后')

ylabel('偏自相关系数')

% 训练ARIMA模型

if isKill == 0

model = arima('D', d, 'ARLags', [1 2], 'MALags', 1); % ARIMA(p, d, q) model

else

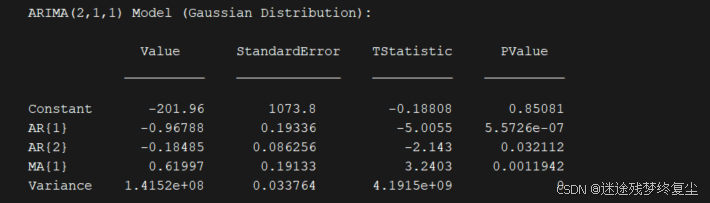

model = arima(2, 1, 1);

end

model = estimate(model, y_diff);

% 测试未来时间预测情况

if isPre == 0

horizon = length(y) - train_size;

else

horizon = PreTime;

end

[forecastTest, YMSE, forecastCI] = forecast(model, horizon, 'Y0', y_diff);

ResultScale(:, 1) = forecastTest - 1.64*sqrt(YMSE); % 90%置信区间下限

ResultScale(:, 2) = forecastTest + 1.64*sqrt(YMSE); % 90%置信区间上限

% 自动确定的可能修正方法

if isKill == 0

forecastTest = forecastTest + train_data(end) - forecastTest(1);

ResultScale(:, 1) = forecastTest - 1.64*sqrt(YMSE); % 90%置信区间下限

ResultScale(:, 2) = forecastTest + 1.64*sqrt(YMSE); % 90%置信区间上限

end

% 可视化预测结果

figure

plot(y, 'ko-')

hold on

if isPre == 0

% 如果是测试数据预测,绘制测试集部分的预测值和置信区间

time_axis = (train_size+1:length(y))';

plot(time_axis, forecastTest, 'b-', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 1), 'r--', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 2), 'r--', 'LineWidth', 1.5)

fill([time_axis; flipud(time_axis)], [ResultScale(:, 1); flipud(ResultScale(:, 2))], 'r', 'FaceAlpha', 0.3)

else

% 如果是新时间段预测,绘制新时间段的预测值和置信区间

time_axis = (length(y)+1:length(y)+PreTime)';

plot(time_axis, forecastTest, 'b-', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 1), 'r--', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 2), 'r--', 'LineWidth', 1.5)

fill([time_axis; flipud(time_axis)], [ResultScale(:, 1); flipud(ResultScale(:, 2))], 'r', 'FaceAlpha', 0.3)

end

xlabel('时间')

ylabel('值')

legend('观察值', '预测值', '下置信界限', '上置信界限')

title('ARIMA预测结果及置信区间')

% 误差分析和残差检验(仅当isPre == 0时)

if isPre == 0

% 误差分析

error = y(train_size+1:end) - forecastTest;

mse = mean(error.^2);

rmse = sqrt(mse);

mae = mean(abs(error));

fprintf('均方误差 (MSE): %.4f\n', mse);

fprintf('均方根误差 (RMSE): %.4f\n', rmse);

fprintf('平均绝对误差 (MAE): %.4f\n', mae);

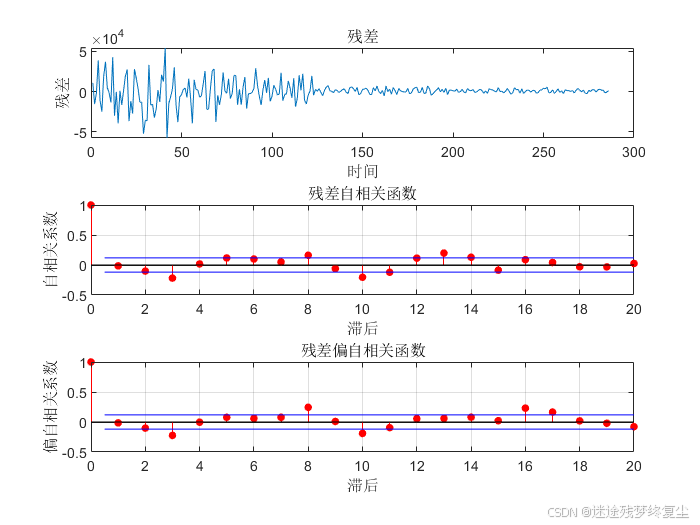

% 残差检验

residuals = infer(model, y_diff);

figure

subplot(3,1,1)

plot(residuals)

xlabel('时间')

ylabel('残差')

title('残差')

% 残差自相关检验

subplot(3,1,2)

autocorr(residuals)

xlabel('滞后')

ylabel('自相关系数')

title('残差自相关函数')

% 残差偏自相关检验

subplot(3,1,3)

parcorr(residuals)

xlabel('滞后')

ylabel('偏自相关系数')

title('残差偏自相关函数')

end

代码分段解释

平稳性检验

- ADF检验:用于检测时间序列是否具有单位根,即是否非平稳。如果拒绝原假设(即h_adf=1),则认为序列平稳。

- KPSS检验:用于检测时间序列是否平稳。如果拒绝原假设(即h_kpss=0),则认为序列非平稳。

% 平稳性检验 - ADF检验

[h_adf, p_adf] = adftest(y);

fprintf('ADF检验结果:\n');

fprintf('是否拒绝原假设(序列非平稳): %d\n', h_adf);

fprintf('p值: %.4f\n', p_adf);

% 平稳性检验 - KPSS检验

[h_kpss, p_kpss] = kpsstest(y);

fprintf('KPSS检验结果:\n');

fprintf('是否拒绝原假设(序列平稳): %d\n', ~h_kpss);

fprintf('p值: %.4f\n', p_kpss);强制确定模型

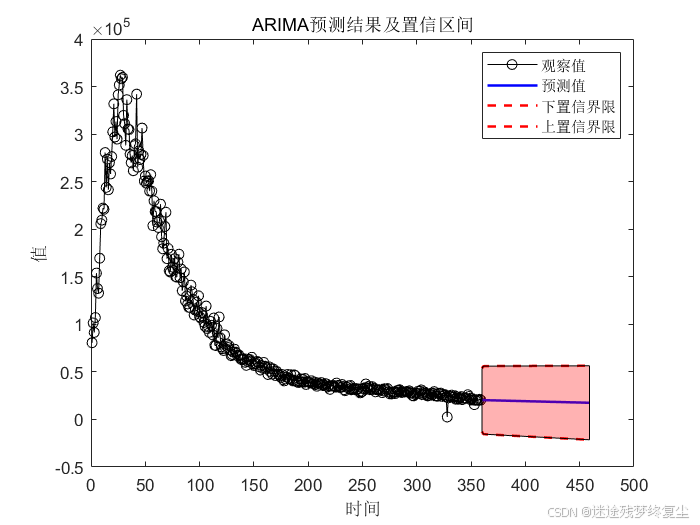

当强制确定模型,即isKill = 1时结果如下图所示:

自动确定模型

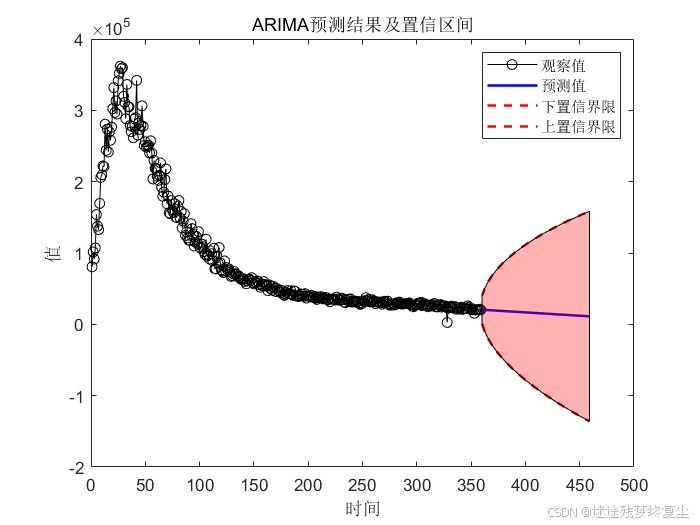

当非强制确定模型时,会给出推荐的差分阶数,如下图所示:

差分(仅非强制确定模型时有效)

根据ADF和KPSS检验结果,确定差分阶数d。如果序列非平稳,则需要进行差分处理以使其平稳。

% 确定d参数

if isKill == 0

% 根据ADF和KPSS检验结果确定d参数

if h_adf == 1 && h_kpss == 0

d = 0;

disp('序列已经平稳')

elseif h_adf == 0 && h_kpss == 1

d = 1;

disp('序列需要一阶差分')

elseif h_adf == 1 && h_kpss == 1

d = 2;

disp('序列需要二阶差分')

else

error('无法确定d参数');

end

% 差分处理

if d > 0

y_diff = diff(train_data, d);

else

y_diff = train_data;

end

else

y_diff = train_data;

end模型选择

通过自相关函数(ACF)和偏自相关函数(PACF)图确定ARIMA模型的p和q参数。这里假设p=2和q=1。

% 确定p和q参数

figure

subplot(2,1,1)

autocorr(y_diff)

title('自相关函数')

xlabel('滞后')

ylabel('自相关系数')

subplot(2,1,2)

parcorr(y_diff)

title('偏自相关函数')

xlabel('滞后')

ylabel('偏自相关系数')自动确定模型

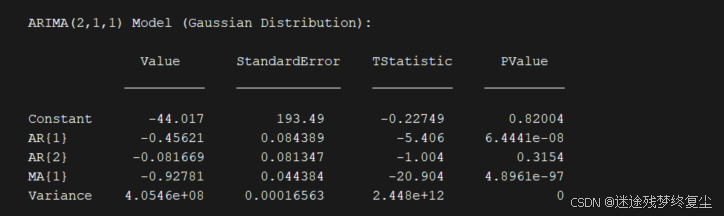

运行结果如下图所示:

强制确定模型

运行结果如下图所示:

模型训练和预测

训练ARIMA模型并进行未来数据的预测,计算预测值的置信区间。

% 训练ARIMA模型

if isKill == 0

model = arima('D', d, 'ARLags', [1 2], 'MALags', 1); % ARIMA(p, d, q) model

else

model = arima(2, 1, 1);

end

model = estimate(model, y_diff);

% 测试未来时间预测情况

if isPre == 0

horizon = length(y) - train_size;

else

horizon = PreTime;

end

[forecastTest, YMSE, forecastCI] = forecast(model, horizon, 'Y0', y_diff);

ResultScale(:, 1) = forecastTest - 1.64*sqrt(YMSE); % 90%置信区间下限

ResultScale(:, 2) = forecastTest + 1.64*sqrt(YMSE); % 90%置信区间上限

% 自动确定的可能修正方法

if isKill == 0

forecastTest = forecastTest + train_data(end) - forecastTest(1);

ResultScale(:, 1) = forecastTest - 1.64*sqrt(YMSE); % 90%置信区间下限

ResultScale(:, 2) = forecastTest + 1.64*sqrt(YMSE); % 90%置信区间上限

end

% 可视化预测结果

figure

plot(y, 'ko-')

hold on

if isPre == 0

% 如果是测试数据预测,绘制测试集部分的预测值和置信区间

time_axis = (train_size+1:length(y))';

plot(time_axis, forecastTest, 'b-', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 1), 'r--', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 2), 'r--', 'LineWidth', 1.5)

fill([time_axis; flipud(time_axis)], [ResultScale(:, 1); flipud(ResultScale(:, 2))], 'r', 'FaceAlpha', 0.3)

else

% 如果是新时间段预测,绘制新时间段的预测值和置信区间

time_axis = (length(y)+1:length(y)+PreTime)';

plot(time_axis, forecastTest, 'b-', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 1), 'r--', 'LineWidth', 1.5)

plot(time_axis, ResultScale(:, 2), 'r--', 'LineWidth', 1.5)

fill([time_axis; flipud(time_axis)], [ResultScale(:, 1); flipud(ResultScale(:, 2))], 'r', 'FaceAlpha', 0.3)

end

xlabel('时间')

ylabel('值')

legend('观察值', '预测值', '下置信界限', '上置信界限')

title('ARIMA预测结果及置信区间')

% 误差分析和残差检验(仅当isPre == 0时)

if isPre == 0

% 误差分析

error = y(train_size+1:end) - forecastTest;

mse = mean(error.^2);

rmse = sqrt(mse);

mae = mean(abs(error));

fprintf('均方误差 (MSE): %.4f\n', mse);

fprintf('均方根误差 (RMSE): %.4f\n', rmse);

fprintf('平均绝对误差 (MAE): %.4f\n', mae);

% 残差检验

residuals = infer(model, y_diff);

figure

subplot(3,1,1)

plot(residuals)

xlabel('时间')

ylabel('残差')

title('残差')

% 残差自相关检验

subplot(3,1,2)

autocorr(residuals)

xlabel('滞后')

ylabel('自相关系数')

title('残差自相关函数')

% 残差偏自相关检验

subplot(3,1,3)

parcorr(residuals)

xlabel('滞后')

ylabel('偏自相关系数')

title('残差偏自相关函数')

end自动确定模型

强制确定模型

非预测模式

在非预测模式下,会给出相关参数的检验及可视化结果,如下图所示:

数据表格格式

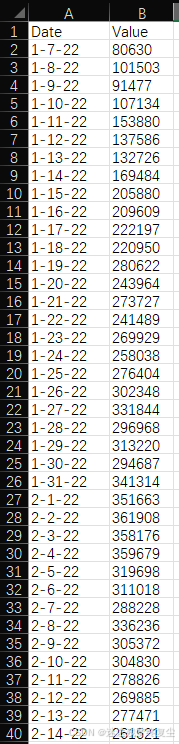

【2024-08-05更新】数据表格格式如下:

5098

5098

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言