本文介绍概率论中的可选停止定理,该定理指出,在特定条件下,鞅过程在停止时刻的期望值等于其初始期望值。文章强调了这一结果对于数学金融和资产定价基本定理的重要性。

本文介绍概率论中的可选停止定理,该定理指出,在特定条件下,鞅过程在停止时刻的期望值等于其初始期望值。文章强调了这一结果对于数学金融和资产定价基本定理的重要性。

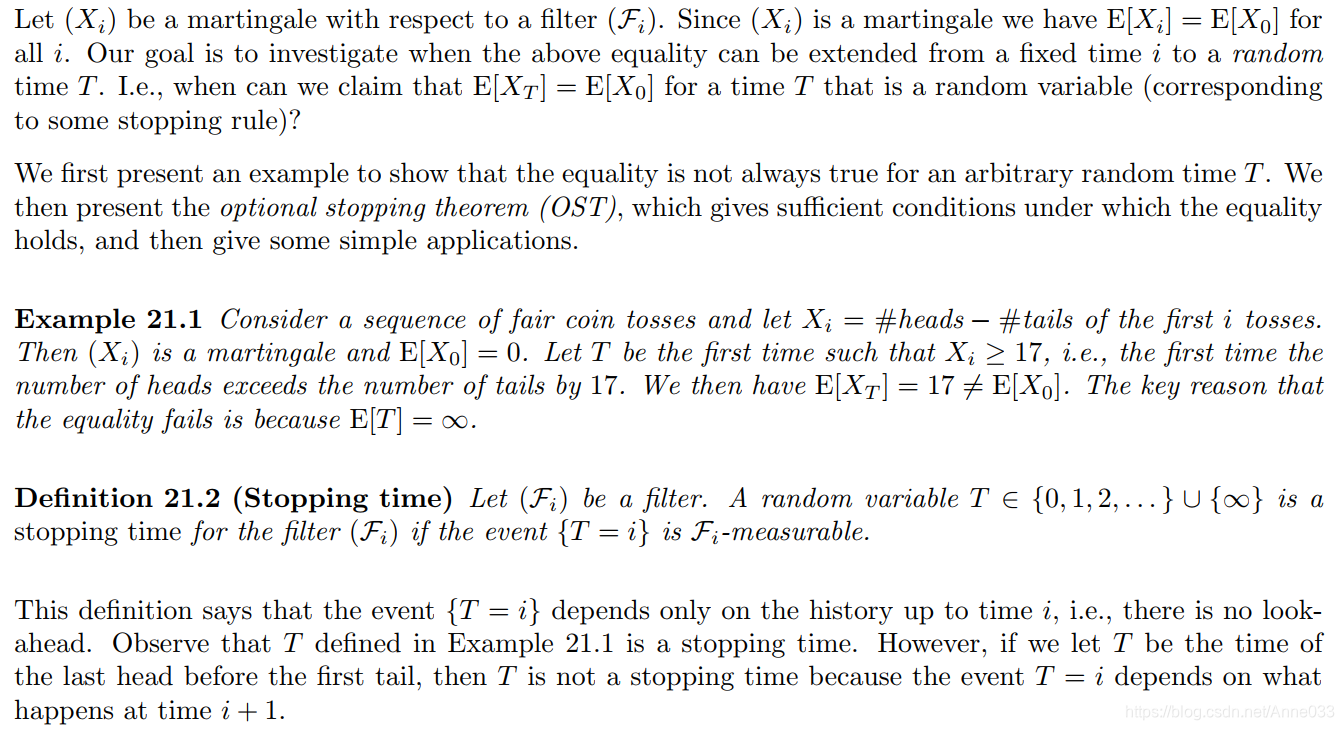

In probability theory, the optional stopping theorem (or Doob’s optional sampling theorem) says that, under certain conditions, the expected value of a martingale at a stopping time is equal to its initial expected value. Since martingales can be used to model the wealth of a gambler participating in a fair game, the optional stopping theorem says that, on average, nothing can be gained by stopping play based on the information obtainable so far (i.e., without looking into the future). Certain conditions are necessary for this result to hold true. In particular, the theorem applies to doubling strategies.

The optional stopping theorem is an important tool of mathematical finance in the context of the fundamental theorem of asset pricing.

https://en.wikipedia.org/wiki/Optional_stopping_theorem

https://people.eecs.berkeley.edu/~sinclair/cs271/n21.pdf

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言