参考博客:https://xueqiu.com/8287840120/75542824

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

aapl = web.get_data_yahoo('AAPL', '2000-01-01')['Adj Close']

msft = web.get_data_yahoo('MSFT', '2000-01-01')['Adj Close']

msft = web.get_data_yahoo('MSFT', '2000-01-01')['Adj Close']

aapl_rets = aapl.pct_change()

msft_rets = msft.pct_change()

msft_rets = msft.pct_change()

plt.figure()

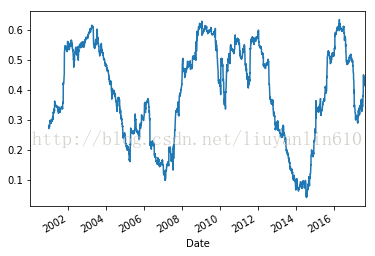

aapl_rets.rolling( 250).corr( msft_rets).plot()

aapl_rets.rolling( 250).corr( msft_rets).plot()

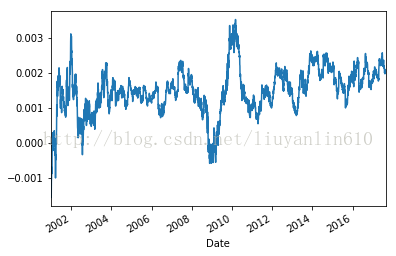

mm = msft_rets.rolling(250).mean()

results = smf.ols('aapl_rets~MSFT', data=pd.DataFrame({'MSFT': mm}))

results.fit().fittedvalues.plot()

1056

1056

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言