本文介绍了一种名为“长剑射天,股价落地”的股票卖出策略。该策略通过特定K线形态识别股价高位反转信号,适用于上升行情的价格顶部。文章详细解释了形态特征及操作原则,并提供了策略实现代码。

本文介绍了一种名为“长剑射天,股价落地”的股票卖出策略。该策略通过特定K线形态识别股价高位反转信号,适用于上升行情的价格顶部。文章详细解释了形态特征及操作原则,并提供了策略实现代码。

写在前面:

1. 本文中提到的“股票策略校验工具”的具体使用操作请查看该博文;

2. 文中知识内容来自书籍《同花顺炒股软件从入门到精通》

3. 本系列文章是用来学习技法,文中所得内容都仅仅只是作为演示功能使用

目录

解说

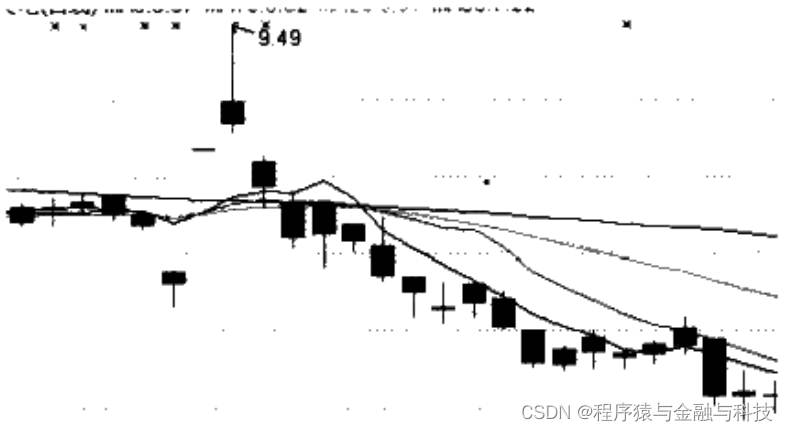

所谓“长剑射天,股价落地”,是指股价进入高位后,出现一条长上影小实体K线,该形态具备如下特征。

1)应是上影较长的星形小阳或小阴线,而且长影长度是实体的2倍以上。

2)当天成交量有较大幅度的提升。

3)必须是处于股价高位或者波段顶部。

出现“长剑射天,股价落地”的形态后,股票投资者需遵循以下操作原则。

1)此形态出现在上升行情的价格顶部是强烈卖出信号。

2)本形态出现频率相当高,能在任何部位形成,但只有在高位出现时,方为可信卖出信号。

策略代码

def excute_strategy(base_data,data_dir):

'''

卖出口诀 - 长箭射天,股价落地

解析:

1. 出现一条长上影小实体K线

2. 长影长度是实体的2倍以上

3. 成交量有较大幅度的提升

4. 上影线要高于前一日高点

自定义:

1. 较大幅度的提升 =》 前一日的两倍

2. 小实体 =》 K线实体是前一日收盘价的1.5%以下0.5%以上

3. 卖出时点 =》 形态出现后下一交易日

4. 胜 =》 卖出后第三个交易日收盘价下跌,为胜

只计算最近两年的数据

:param base_data:股票代码与股票简称 键值对

:param data_dir:股票日数据文件所在目录

:return:

'''

import pandas as pd

import numpy as np

import talib,os

from datetime import datetime

from dateutil.relativedelta import relativedelta

from tools import stock_factor_caculate

def res_pre_two_year_first_day():

pre_year_day = (datetime.now() - relativedelta(years=2)).strftime('%Y-%m-%d')

return pre_year_day

caculate_start_date_str = res_pre_two_year_first_day()

dailydata_file_list = os.listdir(data_dir)

total_count = 0

total_win = 0

check_count = 0

list_list = []

detail_map = {}

factor_list = ['VOL']

ma_list = []

for item in dailydata_file_list:

item_arr = item.split('.')

ticker = item_arr[0]

secName = base_data[ticker]

file_path = data_dir + item

df = pd.read_csv(file_path,encoding='utf-8')

# 删除停牌的数据

df = df.loc[df['openPrice'] > 0].copy()

df['o_date'] = df['tradeDate']

df['o_date'] = pd.to_datetime(df['o_date'])

df = df.loc[df['o_date'] >= caculate_start_date_str].copy()

# 保存未复权收盘价数据

df['close'] = df['closePrice']

# 计算前复权数据

df['openPrice'] = df['openPrice'] * df['accumAdjFactor']

df['closePrice'] = df['closePrice'] * df['accumAdjFactor']

df['highestPrice'] = df['highestPrice'] * df['accumAdjFactor']

df['lowestPrice'] = df['lowestPrice'] * df['accumAdjFactor']

if len(df)<=0:

continue

# 开始计算

for item in factor_list:

df = stock_factor_caculate.caculate_factor(df,item)

for item in ma_list:

df = stock_factor_caculate.caculate_factor(df,item)

df.reset_index(inplace=True)

df['i_row'] = [i for i in range(len(df))]

df['three_chg'] = round(((df['close'].shift(-3) - df['close']) / df['close']) * 100, 4)

df['three_after_close'] = df['close'].shift(-3)

df['body_length'] = abs(df['closePrice']-df['openPrice'])

df['up_shadow'] = 0

df.loc[df['closePrice']>df['openPrice'],'up_shadow'] = df['highestPrice'] - df['closePrice']

df.loc[df['closePrice']<df['openPrice'],'up_shadow'] = df['highestPrice'] - df['openPrice']

df['target_yeah'] = 0

df.loc[(df['body_length']/df['closePrice'].shift(1)>0.005) & (df['body_length']/df['closePrice'].shift(1)<0.015) & (df['highestPrice']>df['highestPrice'].shift(1)) & (df['up_shadow']>2*df['body_length']) & (df['turnoverVol']>=2*df['turnoverVol'].shift(1)),'target_yeah'] = 1

df_target = df.loc[df['target_yeah']==1].copy()

# 临时 start

# df.to_csv('D:/temp006/'+ticker + '.csv',encoding='utf-8')

# 临时 end

node_count = 0

node_win = 0

duration_list = []

table_list = []

i_row_list = df_target['i_row'].values.tolist()

for i,row0 in enumerate(i_row_list):

row = row0 + 1

if row >= len(df):

continue

date_str = df.iloc[row]['tradeDate']

cur_close = df.iloc[row]['close']

three_after_close = df.iloc[row]['three_after_close']

three_chg = df.iloc[row]['three_chg']

table_list.append([

i,date_str,cur_close,three_after_close,three_chg

])

duration_list.append([row-2,row+3])

node_count += 1

if three_chg<0:

node_win +=1

pass

list_list.append({

'ticker':ticker,

'secName':secName,

'count':node_count,

'win':0 if node_count<=0 else round((node_win/node_count)*100,2)

})

detail_map[ticker] = {

'table_list': table_list,

'duration_list': duration_list

}

total_count += node_count

total_win += node_win

check_count += 1

pass

df = pd.DataFrame(list_list)

results_data = {

'check_count':check_count,

'total_count':total_count,

'total_win':0 if total_count<=0 else round((total_win/total_count)*100,2),

'start_date_str':caculate_start_date_str,

'df':df,

'detail_map':detail_map,

'factor_list':factor_list,

'ma_list':ma_list

}

return results_data结果

本文校验的数据是随机抽取的81个股票

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言