文章目录

Task3 特征工程

此部分为零基础入门金融风控的 Task3 特征工程部分,带你来了解各种特征工程以及分析方法,欢迎大家后续多多交流。

赛题:零基础入门数据挖掘 - 零基础入门金融风控之贷款违约

项目地址:https://github.com/datawhalechina/team-learning-data-mining/tree/master/FinancialRiskControl

比赛地址:https://tianchi.aliyun.com/competition/entrance/531830/introduction

数据集下载地址:

https://tianchi.aliyun.com/competition/entrance/531830/information

3.1 学习目标

- 学习特征预处理、缺失值、异常值处理、数据分桶等特征处理方法

- 学习特征交互、编码、选择的相应方法

- 完成相应学习打卡任务,两个选做的作业不做强制性要求,供学有余力同学自己探索

3.2 内容介绍

- 数据预处理

- 缺失值的填充

- 时间格式处理

- 对象类型特征转换到数值

- 异常值处理

- 基于3segama原则

- 基于箱型图

- 数据分箱

- 固定宽度分箱

- 分位数分箱

- 离散数值型数据分箱

- 连续数值型数据分箱

- 卡方分箱(选做作业)

- 特征交互

- 特征和特征之间组合

- 特征和特征之间衍生

- 其他特征衍生的尝试(选做作业)

- 特征编码

- one-hot编码

- label-encode编码

- 特征选择

- 1 Filter

- 2 Wrapper (RFE)

- 3 Embedded

3.3 代码示例

3.3.1 导入包并读取数据

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import datetime

from tqdm import tqdm

from sklearn.preprocessing import LabelEncoder

from sklearn.feature_selection import SelectKBest

from sklearn.feature_selection import chi2

from sklearn.preprocessing import MinMaxScaler

import xgboost as xgb

import lightgbm as lgb

from catboost import CatBoostRegressor

import warnings

from sklearn.model_selection import StratifiedKFold, KFold

from sklearn.metrics import accuracy_score, f1_score, roc_auc_score, log_loss

warnings.filterwarnings('ignore')

data_train =pd.read_csv('../train.csv')

data_test_a = pd.read_csv('../testA.csv')

3.3.2特征预处理

- 数据EDA部分我们已经对数据的大概和某些特征分布有了了解,数据预处理部分一般我们要处理一些EDA阶段分析出来的问题,这里介绍了数据缺失值的填充,时间格式特征的转化处理,某些对象类别特征的处理。

首先我们查找出数据中的对象特征和数值特征

numerical_fea = list(data_train.select_dtypes(exclude=['object']).columns)

category_fea = list(filter(lambda x: x not in numerical_fea,list(data_train.columns)))

label = 'isDefault'

numerical_fea.remove(label)

在比赛中数据预处理是必不可少的一部分,对于缺失值的填充往往会影响比赛的结果,在比赛中不妨尝试多种填充然后比较结果选择结果最优的一种;

比赛数据相比真实场景的数据相对要“干净”一些,但是还是会有一定的“脏”数据存在,清洗一些异常值往往会获得意想不到的效果。

缺失值填充

-

把所有缺失值替换为指定的值0

data_train = data_train.fillna(0)

-

向用缺失值上面的值替换缺失值

data_train = data_train.fillna(axis=0,method=‘ffill’)

-

纵向用缺失值下面的值替换缺失值,且设置最多只填充两个连续的缺失值

data_train = data_train.fillna(axis=0,method=‘bfill’,limit=2)

#查看缺失值情况

data_train.isnull().sum()

id 0

loanAmnt 0

term 0

interestRate 0

installment 0

grade 0

subGrade 0

employmentTitle 1

employmentLength 46799

homeOwnership 0

annualIncome 0

verificationStatus 0

issueDate 0

isDefault 0

purpose 0

postCode 1

regionCode 0

dti 239

delinquency_2years 0

ficoRangeLow 0

ficoRangeHigh 0

openAcc 0

pubRec 0

pubRecBankruptcies 405

revolBal 0

revolUtil 531

totalAcc 0

initialListStatus 0

applicationType 0

earliesCreditLine 0

title 1

policyCode 0

n0 40270

n1 40270

n2 40270

n2.1 40270

n4 33239

n5 40270

n6 40270

n7 40270

n8 40271

n9 40270

n10 33239

n11 69752

n12 40270

n13 40270

n14 40270

dtype: int64

#按照中位数填充数值型特征

data_train[numerical_fea] = data_train[numerical_fea].fillna(data_train[numerical_fea].median())

data_test_a[numerical_fea] = data_test_a[numerical_fea].fillna(data_train[numerical_fea].median())

#按照众数填充类别型特征

data_train[category_fea] = data_train[category_fea].fillna(data_train[category_fea].mode())

data_test_a[category_fea] = data_test_a[category_fea].fillna(data_train[category_fea].mode())

data_train.isnull().sum()

id 0

loanAmnt 0

term 0

interestRate 0

installment 0

grade 0

subGrade 0

employmentTitle 0

employmentLength 46799

homeOwnership 0

annualIncome 0

verificationStatus 0

issueDate 0

isDefault 0

purpose 0

postCode 0

regionCode 0

dti 0

delinquency_2years 0

ficoRangeLow 0

ficoRangeHigh 0

openAcc 0

pubRec 0

pubRecBankruptcies 0

revolBal 0

revolUtil 0

totalAcc 0

initialListStatus 0

applicationType 0

earliesCreditLine 0

title 0

policyCode 0

n0 0

n1 0

n2 0

n2.1 0

n4 0

n5 0

n6 0

n7 0

n8 0

n9 0

n10 0

n11 0

n12 0

n13 0

n14 0

dtype: int64

#查看类别特征

category_fea

['grade', 'subGrade', 'employmentLength', 'issueDate', 'earliesCreditLine']

- category_fea:对象型类别特征需要进行预处理,其中[‘issueDate’]为时间格式特征。

时间格式处理

#转化成时间格式

for data in [data_train, data_test_a]:

data['issueDate'] = pd.to_datetime(data['issueDate'],format='%Y-%m-%d')

startdate = datetime.datetime.strptime('2007-06-01', '%Y-%m-%d')

#构造时间特征

data['issueDateDT'] = data['issueDate'].apply(lambda x: x-startdate).dt.days

data_train['employmentLength'].value_counts(dropna=False).sort_index()

1 year 52489

10+ years 262753

2 years 72358

3 years 64152

4 years 47985

5 years 50102

6 years 37254

7 years 35407

8 years 36192

9 years 30272

< 1 year 64237

NaN 46799

Name: employmentLength, dtype: int64

对象类型特征转换到数值

def employmentLength_to_int(s):

if pd.isnull(s):

return s

else:

return np.int8(s.split()[0])

for data in [data_train, data_test_a]:

data['employmentLength'].replace(to_replace='10+ years', value='10 years', inplace=True)

data['employmentLength'].replace('< 1 year', '0 years', inplace=True)

data['employmentLength'] = data['employmentLength'].apply(employmentLength_to_int)

data['employmentLength'].value_counts(dropna=False).sort_index()

0.0 15989

1.0 13182

2.0 18207

3.0 16011

4.0 11833

5.0 12543

6.0 9328

7.0 8823

8.0 8976

9.0 7594

10.0 65772

NaN 11742

Name: employmentLength, dtype: int64

- 对earliesCreditLine进行预处理

data_train['earliesCreditLine'].sample(5)

519915 Sep-2002

564368 Dec-1996

768209 May-2004

453092 Nov-1995

763866 Sep-2000

Name: earliesCreditLine, dtype: object

for data in [data_train, data_test_a]:

data['earliesCreditLine'] = data['earliesCreditLine'].apply(lambda s: int(s[-4:]))

类别特征处理

# 部分类别特征

cate_features = ['grade', 'subGrade', 'employmentTitle', 'homeOwnership', 'verificationStatus', 'purpose', 'postCode', 'regionCode', \

'applicationType', 'initialListStatus', 'title', 'policyCode']

for f in cate_features:

print(f, '类型数:', data[f].nunique())

grade 类型数: 7

subGrade 类型数: 35

employmentTitle 类型数: 79282

homeOwnership 类型数: 6

verificationStatus 类型数: 3

purpose 类型数: 14

postCode 类型数: 889

regionCode 类型数: 51

applicationType 类型数: 2

initialListStatus 类型数: 2

title 类型数: 12058

policyCode 类型数: 1

像等级这种类别特征,是有优先级的可以labelencode或者自映射

for data in [data_train, data_test_a]:

data['grade'] = data['grade'].map({'A':1,'B':2,'C':3,'D':4,'E':5,'F':6,'G':7})

# 类型数在2之上,又不是高维稀疏的,且纯分类特征

for data in [data_train, data_test_a]:

data = pd.get_dummies(data, columns=['subGrade', 'homeOwnership', 'verificationStatus', 'purpose', 'regionCode'], drop_first=True)

3.3.3 异常值处理

- 当你发现异常值后,一定要先分清是什么原因导致的异常值,然后再考虑如何处理。首先,如果这一异常值并不代表一种规律性的,而是极其偶然的现象,或者说你并不想研究这种偶然的现象,这时可以将其删除。其次,如果异常值存在且代表了一种真实存在的现象,那就不能随便删除。在现有的欺诈场景中很多时候欺诈数据本身相对于正常数据勒说就是异常的,我们要把这些异常点纳入,重新拟合模型,研究其规律。能用监督的用监督模型,不能用的还可以考虑用异常检测的算法来做。

- 注意test的数据不能删。

检测异常的方法一:均方差

在统计学中,如果一个数据分布近似正态,那么大约 68% 的数据值会在均值的一个标准差范围内,大约 95% 会在两个标准差范围内,大约 99.7% 会在三个标准差范围内。

def find_outliers_by_3segama(data,fea):

data_std = np.std(data[fea])

data_mean = np.mean(data[fea])

outliers_cut_off = data_std * 3

lower_rule = data_mean - outliers_cut_off

upper_rule = data_mean + outliers_cut_off

data[fea+'_outliers'] = data[fea].apply(lambda x:str('异常值') if x > upper_rule or x < lower_rule else '正常值')

return data

- 得到特征的异常值后可以进一步分析变量异常值和目标变量的关系

data_train = data_train.copy()

for fea in numerical_fea:

data_train = find_outliers_by_3segama(data_train,fea)

print(data_train[fea+'_outliers'].value_counts())

print(data_train.groupby(fea+'_outliers')['isDefault'].sum())

print('*'*10)

正常值 800000

Name: id_outliers, dtype: int64

id_outliers

正常值 159610

Name: isDefault, dtype: int64

**********

正常值 800000

Name: loanAmnt_outliers, dtype: int64

loanAmnt_outliers

正常值 159610

Name: isDefault, dtype: int64

**********

正常值 800000

Name: term_outliers, dtype: int64

term_outliers

正常值 159610

Name: isDefault, dtype: int64

**********

正常值 794259

异常值 5741

Name: interestRate_outliers, dtype: int64

interestRate_outliers

异常值 2916

正常值 156694

Name: isDefault, dtype: int64

**********

正常值 792046

异常值 7954

Name: installment_outliers, dtype: int64

installment_outliers

异常值 2152

正常值 157458

Name: isDefault, dtype: int64

**********

正常值 800000

Name: employmentTitle_outliers, dtype: int64

employmentTitle_outliers

正常值 159610

Name: isDefault, dtype: int64

**********

正常值 799701

异常值 299

Name: homeOwnership_outliers, dtype: int64

homeOwnership_outliers

异常值 62

正常值 159548

Name: isDefault, dtype: int64

**********

正常值 793973

异常值 6027

Name: annualIncome_outliers, dtype: int64

annualIncome_outliers

异常值 756

正常值 158854

Name: isDefault, dtype: int64

**********

正常值 800000

Name: verificationStatus_outliers, dtype: int64

verificationStatus_outliers

正常值 159610

Name: isDefault, dtype: int64

**********

正常值 783003

异常值 16997

Name: purpose_outliers, dtype: int64

purpose_outliers

异常值 3635

正常值 155975

Name: isDefault, dtype: int64

**********

正常值 798931

异常值 1069

Name: postCode_outliers, dtype: int64

postCode_outliers

异常值 221

正常值 159389

Name: isDefault, dtype: int64

**********

正常值 799994

异常值 6

Name: regionCode_outliers, dtype: int64

regionCode_outliers

异常值 1

正常值 159609

Name: isDefault, dtype: int64

**********

正常值 798440

异常值 1560

Name: dti_outliers, dtype: int64

dti_outliers

异常值 466

正常值 159144

Name: isDefault, dtype: int64

**********

正常值 778245

异常值 21755

Name: delinquency_2years_outliers, dtype: int64

delinquency_2years_outliers

异常值 5089

正常值 154521

Name: isDefault, dtype: int64

**********

正常值 788261

异常值 11739

Name: ficoRangeLow_outliers, dtype: int64

ficoRangeLow_outliers

异常值 778

正常值 158832

Name: isDefault, dtype: int64

**********

正常值 788261

异常值 11739

Name: ficoRangeHigh_outliers, dtype: int64

ficoRangeHigh_outliers

异常值 778

正常值 158832

Name: isDefault, dtype: int64

**********

正常值 790889

异常值 9111

Name: openAcc_outliers, dtype: int64

openAcc_outliers

异常值 2195

正常值 157415

Name: isDefault, dtype: int64

**********

正常值 792471

异常值 7529

Name: pubRec_outliers, dtype: int64

pubRec_outliers

异常值 1701

正常值 157909

Name: isDefault, dtype: int64

**********

正常值 794120

异常值 5880

Name: pubRecBankruptcies_outliers, dtype: int64

pubRecBankruptcies_outliers

异常值 1423

正常值 158187

Name: isDefault, dtype: int64

**********

正常值 790001

异常值 9999

Name: revolBal_outliers, dtype: int64

revolBal_outliers

异常值 1359

正常值 158251

Name: isDefault, dtype: int64

**********

正常值 799948

异常值 52

Name: revolUtil_outliers, dtype: int64

revolUtil_outliers

异常值 23

正常值 159587

Name: isDefault, dtype: int64

**********

正常值 791663

异常值 8337

Name: totalAcc_outliers, dtype: int64

totalAcc_outliers

异常值 1668

正常值 157942

Name: isDefault, dtype: int64

**********

正常值 800000

Name: initialListStatus_outliers, dtype: int64

initialListStatus_outliers

正常值 159610

Name: isDefault, dtype: int64

**********

正常值 784586

异常值 15414

Name: applicationType_outliers, dtype: int64

applicationType_outliers

异常值 3875

正常值 155735

Name: isDefault, dtype: int64

**********

正常值 775134

异常值 24866

Name: title_outliers, dtype: int64

title_outliers

异常值 3900

正常值 155710

Name: isDefault, dtype: int64

**********

正常值 800000

Name: policyCode_outliers, dtype: int64

policyCode_outliers

正常值 159610

Name: isDefault, dtype: int64

**********

正常值 782773

异常值 17227

Name: n0_outliers, dtype: int64

n0_outliers

异常值 3485

正常值 156125

Name: isDefault, dtype: int64

**********

正常值 790500

异常值 9500

Name: n1_outliers, dtype: int64

n1_outliers

异常值 2491

正常值 157119

Name: isDefault, dtype: int64

**********

正常值 789067

异常值 10933

Name: n2_outliers, dtype: int64

n2_outliers

异常值 3205

正常值 156405

Name: isDefault, dtype: int64

**********

正常值 789067

异常值 10933

Name: n2.1_outliers, dtype: int64

n2.1_outliers

异常值 3205

正常值 156405

Name: isDefault, dtype: int64

**********

正常值 788660

异常值 11340

Name: n4_outliers, dtype: int64

n4_outliers

异常值 2476

正常值 157134

Name: isDefault, dtype: int64

**********

正常值 790355

异常值 9645

Name: n5_outliers, dtype: int64

n5_outliers

异常值 1858

正常值 157752

Name: isDefault, dtype: int64

**********

正常值 786006

异常值 13994

Name: n6_outliers, dtype: int64

n6_outliers

异常值 3182

正常值 156428

Name: isDefault, dtype: int64

**********

正常值 788430

异常值 11570

Name: n7_outliers, dtype: int64

n7_outliers

异常值 2746

正常值 156864

Name: isDefault, dtype: int64

**********

正常值 789625

异常值 10375

Name: n8_outliers, dtype: int64

n8_outliers

异常值 2131

正常值 157479

Name: isDefault, dtype: int64

**********

正常值 786384

异常值 13616

Name: n9_outliers, dtype: int64

n9_outliers

异常值 3953

正常值 155657

Name: isDefault, dtype: int64

**********

正常值 788979

异常值 11021

Name: n10_outliers, dtype: int64

n10_outliers

异常值 2639

正常值 156971

Name: isDefault, dtype: int64

**********

正常值 799434

异常值 566

Name: n11_outliers, dtype: int64

n11_outliers

异常值 112

正常值 159498

Name: isDefault, dtype: int64

**********

正常值 797585

异常值 2415

Name: n12_outliers, dtype: int64

n12_outliers

异常值 545

正常值 159065

Name: isDefault, dtype: int64

**********

正常值 788907

异常值 11093

Name: n13_outliers, dtype: int64

n13_outliers

异常值 2482

正常值 157128

Name: isDefault, dtype: int64

**********

正常值 788884

异常值 11116

Name: n14_outliers, dtype: int64

n14_outliers

异常值 3364

正常值 156246

Name: isDefault, dtype: int64

**********

- 例如可以看到异常值在两个变量上的分布几乎复合整体的分布,如果异常值都属于为1的用户数据里面代表什么呢?

#删除异常值

for fea in numerical_fea:

data_train = data_train[data_train[fea+'_outliers']=='正常值']

data_train = data_train.reset_index(drop=True)

检测异常的方法二:箱型图

- 总结一句话:四分位数会将数据分为三个点和四个区间,IQR = Q3 -Q1,下触须=Q1 − 1.5x IQR,上触须=Q3 + 1.5x IQR;

3.3.4 数据分桶

-

特征分箱的目的:

- 从模型效果上来看,特征分箱主要是为了降低变量的复杂性,减少变量噪音对模型的影响,提高自变量和因变量的相关度。从而使模型更加稳定。

-

数据分桶的对象:

- 将连续变量离散化

- 将多状态的离散变量合并成少状态

-

分箱的原因:

- 数据的特征内的值跨度可能比较大,对有监督和无监督中如k-均值聚类它使用欧氏距离作为相似度函数来测量数据点之间的相似度。都会造成大吃小的影响,其中一种解决方法是对计数值进行区间量化即数据分桶也叫做数据分箱,然后使用量化后的结果。

-

分箱的优点:

- 处理缺失值:当数据源可能存在缺失值,此时可以把null单独作为一个分箱。

- 处理异常值:当数据中存在离群点时,可以把其通过分箱离散化处理,从而提高变量的鲁棒性(抗干扰能力)。例如,age若出现200这种异常值,可分入“age > 60”这个分箱里,排除影响。

- 业务解释性:我们习惯于线性判断变量的作用,当x越来越大,y就越来越大。但实际x与y之间经常存在着非线性关系,此时可经过WOE变换。

-

特别要注意一下分箱的基本原则:

- (1)最小分箱占比不低于5%

- (2)箱内不能全部是好客户

- (3)连续箱单调

- 固定宽度分箱

当数值横跨多个数量级时,最好按照 10 的幂(或任何常数的幂)来进行分组:09、1099、100999、10009999,等等。固定宽度分箱非常容易计算,但如果计数值中有比较大的缺口,就会产生很多没有任何数据的空箱子。

# 通过除法映射到间隔均匀的分箱中,每个分箱的取值范围都是loanAmnt/1000

data['loanAmnt_bin1'] = np.floor_divide(data['loanAmnt'], 1000)

## 通过对数函数映射到指数宽度分箱

data['loanAmnt_bin2'] = np.floor(np.log10(data['loanAmnt']))

- 分位数分箱

data['loanAmnt_bin3'] = pd.qcut(data['loanAmnt'], 10, labels=False)

- 卡方分箱及其他分箱方法的尝试

- 这一部分属于进阶部分,学有余力的同学可以自行搜索尝试。

3.3.5 特征交互

- 交互特征的构造非常简单,使用起来却代价不菲。如果线性模型中包含有交互特征对,那它的训练时间和评分时间就会从 O(n) 增加到 O(n2),其中 n 是单一特征的数量。

for col in ['grade', 'subGrade']:

temp_dict = data_train.groupby([col])['isDefault'].agg(['mean']).reset_index().rename(columns={'mean': col + '_target_mean'})

temp_dict.index = temp_dict[col].values

temp_dict = temp_dict[col + '_target_mean'].to_dict()

data_train[col + '_target_mean'] = data_train[col].map(temp_dict)

data_test_a[col + '_target_mean'] = data_test_a[col].map(temp_dict)

# 其他衍生变量 mean 和 std

for df in [data_train, data_test_a]:

for item in ['n0','n1','n2','n2.1','n4','n5','n6','n7','n8','n9','n10','n11','n12','n13','n14']:

df['grade_to_mean_' + item] = df['grade'] / df.groupby([item])['grade'].transform('mean')

df['grade_to_std_' + item] = df['grade'] / df.groupby([item])['grade'].transform('std')

这里给出一些特征交互的思路,但特征和特征间的交互衍生出新的特征还远远不止于此,抛砖引玉,希望大家多多探索。请学习者尝试其他的特征交互方法。

3.3.6 特征编码

labelEncode 直接放入树模型中

#label-encode:subGrade,postCode,title

# 高维类别特征需要进行转换

for col in tqdm(['employmentTitle', 'postCode', 'title','subGrade']):

le = LabelEncoder()

le.fit(list(data_train[col].astype(str).values) + list(data_test_a[col].astype(str).values))

data_train[col] = le.transform(list(data_train[col].astype(str).values))

data_test_a[col] = le.transform(list(data_test_a[col].astype(str).values))

print('Label Encoding 完成')

100%|██████████| 4/4 [00:08<00:00, 2.04s/it]

Label Encoding 完成

逻辑回归等模型要单独增加的特征工程

- 对特征做归一化,去除相关性高的特征

- 归一化目的是让训练过程更好更快的收敛,避免特征大吃小的问题

- 去除相关性是增加模型的可解释性,加快预测过程。

# 举例归一化过程

#伪代码

for fea in [要归一化的特征列表]:

data[fea] = ((data[fea] - np.min(data[fea])) / (np.max(data[fea]) - np.min(data[fea])))

3.3.7 特征选择

- 特征选择技术可以精简掉无用的特征,以降低最终模型的复杂性,它的最终目的是得到一个简约模型,在不降低预测准确率或对预测准确率影响不大的情况下提高计算速度。特征选择不是为了减少训练时间(实际上,一些技术会增加总体训练时间),而是为了减少模型评分时间。

特征选择的方法:

- 1 Filter

- 方差选择法

- 相关系数法(pearson 相关系数)

- 卡方检验

- 互信息法

- 2 Wrapper (RFE)

- 递归特征消除法

- 3 Embedded

- 基于惩罚项的特征选择法

- 基于树模型的特征选择

Filter

- 基于特征间的关系进行筛选

方差选择法

- 方差选择法中,先要计算各个特征的方差,然后根据设定的阈值,选择方差大于阈值的特征

from sklearn.feature_selection import VarianceThreshold

#其中参数threshold为方差的阈值

VarianceThreshold(threshold=3).fit_transform(train,target_train)

相关系数法

- Pearson 相关系数

皮尔森相关系数是一种最简单的,可以帮助理解特征和响应变量之间关系的方法,该方法衡量的是变量之间的线性相关性。

结果的取值区间为 [-1,1] , -1 表示完全的负相关, +1表示完全的正相关,0 表示没有线性相关。

from sklearn.feature_selection import SelectKBest

from scipy.stats import pearsonr

#选择K个最好的特征,返回选择特征后的数据

#第一个参数为计算评估特征是否好的函数,该函数输入特征矩阵和目标向量,

#输出二元组(评分,P值)的数组,数组第i项为第i个特征的评分和P值。在此定义为计算相关系数

#参数k为选择的特征个数

SelectKBest(k=5).fit_transform(train,target_train)

卡方检验

- 经典的卡方检验是用于检验自变量对因变量的相关性。 假设自变量有N种取值,因变量有M种取值,考虑自变量等于i且因变量等于j的样本频数的观察值与期望的差距。 其统计量如下: χ2=∑(A−T)2T,其中A为实际值,T为理论值

- (注:卡方只能运用在正定矩阵上,否则会报错Input X must be non-negative)

from sklearn.feature_selection import SelectKBest

from sklearn.feature_selection import chi2

#参数k为选择的特征个数

SelectKBest(chi2, k=5).fit_transform(train,target_train)

互信息法

- 经典的互信息也是评价自变量对因变量的相关性的。 在feature_selection库的SelectKBest类结合最大信息系数法可以用于选择特征,相关代码如下:

from sklearn.feature_selection import SelectKBest

from minepy import MINE

#由于MINE的设计不是函数式的,定义mic方法将其为函数式的,

#返回一个二元组,二元组的第2项设置成固定的P值0.5

def mic(x, y):

m = MINE()

m.compute_score(x, y)

return (m.mic(), 0.5)

#参数k为选择的特征个数

SelectKBest(lambda X, Y: array(map(lambda x:mic(x, Y), X.T)).T, k=2).fit_transform(train,target_train)

Wrapper (Recursive feature elimination,RFE)

- 递归特征消除法 递归消除特征法使用一个基模型来进行多轮训练,每轮训练后,消除若干权值系数的特征,再基于新的特征集进行下一轮训练。 在feature_selection库的RFE类可以用于选择特征,相关代码如下(以逻辑回归为例):

from sklearn.feature_selection import RFE

from sklearn.linear_model import LogisticRegression

#递归特征消除法,返回特征选择后的数据

#参数estimator为基模型

#参数n_features_to_select为选择的特征个数

RFE(estimator=LogisticRegression(), n_features_to_select=2).fit_transform(train,target_train)

Embedded

- 基于惩罚项的特征选择法 使用带惩罚项的基模型,除了筛选出特征外,同时也进行了降维。 在feature_selection库的SelectFromModel类结合逻辑回归模型可以用于选择特征,相关代码如下:

from sklearn.feature_selection import SelectFromModel

from sklearn.linear_model import LogisticRegression

#带L1惩罚项的逻辑回归作为基模型的特征选择

SelectFromModel(LogisticRegression(penalty="l1", C=0.1)).fit_transform(train,target_train)

- 基于树模型的特征选择 树模型中GBDT也可用来作为基模型进行特征选择。 在feature_selection库的SelectFromModel类结合GBDT模型可以用于选择特征,相关代码如下:

from sklearn.feature_selection import SelectFromModel

from sklearn.ensemble import GradientBoostingClassifier

#GBDT作为基模型的特征选择

SelectFromModel(GradientBoostingClassifier()).fit_transform(train,target_train)

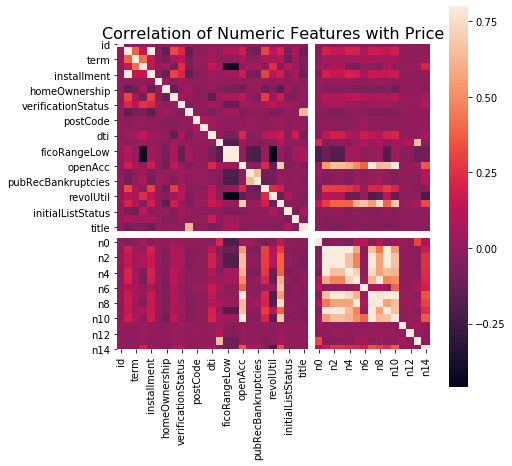

本数据集中我们删除非入模特征后,并对缺失值填充,然后用计算协方差的方式看一下特征间相关性,然后进行模型训练

# 删除不需要的数据

for data in [data_train, data_test_a]:

data.drop(['issueDate','id'], axis=1,inplace=True)

"纵向用缺失值上面的值替换缺失值"

data_train = data_train.fillna(axis=0,method='ffill')

x_train = data_train.drop(['isDefault','id'], axis=1)

#计算协方差

data_corr = x_train.corrwith(data_train.isDefault) #计算相关性

result = pd.DataFrame(columns=['features', 'corr'])

result['features'] = data_corr.index

result['corr'] = data_corr.values

# 当然也可以直接看图

data_numeric = data_train[numerical_fea]

correlation = data_numeric.corr()

f , ax = plt.subplots(figsize = (7, 7))

plt.title('Correlation of Numeric Features with Price',y=1,size=16)

sns.heatmap(correlation,square = True, vmax=0.8)

<matplotlib.axes._subplots.AxesSubplot at 0x12d88ad10>

features = [f for f in data_train.columns if f not in ['id','issueDate','isDefault'] and '_outliers' not in f]

x_train = data_train[features]

x_test = data_test_a[features]

y_train = data_train['isDefault']

def cv_model(clf, train_x, train_y, test_x, clf_name):

folds = 5

seed = 2020

kf = KFold(n_splits=folds, shuffle=True, random_state=seed)

train = np.zeros(train_x.shape[0])

test = np.zeros(test_x.shape[0])

cv_scores = []

for i, (train_index, valid_index) in enumerate(kf.split(train_x, train_y)):

print('************************************ {} ************************************'.format(str(i+1)))

trn_x, trn_y, val_x, val_y = train_x.iloc[train_index], train_y[train_index], train_x.iloc[valid_index], train_y[valid_index]

if clf_name == "lgb":

train_matrix = clf.Dataset(trn_x, label=trn_y)

valid_matrix = clf.Dataset(val_x, label=val_y)

params = {

'boosting_type': 'gbdt',

'objective': 'binary',

'metric': 'auc',

'min_child_weight': 5,

'num_leaves': 2 ** 5,

'lambda_l2': 10,

'feature_fraction': 0.8,

'bagging_fraction': 0.8,

'bagging_freq': 4,

'learning_rate': 0.1,

'seed': 2020,

'nthread': 28,

'n_jobs':24,

'silent': True,

'verbose': -1,

}

model = clf.train(params, train_matrix, 50000, valid_sets=[train_matrix, valid_matrix], verbose_eval=200,early_stopping_rounds=200)

val_pred = model.predict(val_x, num_iteration=model.best_iteration)

test_pred = model.predict(test_x, num_iteration=model.best_iteration)

# print(list(sorted(zip(features, model.feature_importance("gain")), key=lambda x: x[1], reverse=True))[:20])

if clf_name == "xgb":

train_matrix = clf.DMatrix(trn_x , label=trn_y)

valid_matrix = clf.DMatrix(val_x , label=val_y)

params = {'booster': 'gbtree',

'objective': 'binary:logistic',

'eval_metric': 'auc',

'gamma': 1,

'min_child_weight': 1.5,

'max_depth': 5,

'lambda': 10,

'subsample': 0.7,

'colsample_bytree': 0.7,

'colsample_bylevel': 0.7,

'eta': 0.04,

'tree_method': 'exact',

'seed': 2020,

'nthread': 36,

"silent": True,

}

watchlist = [(train_matrix, 'train'),(valid_matrix, 'eval')]

model = clf.train(params, train_matrix, num_boost_round=50000, evals=watchlist, verbose_eval=200, early_stopping_rounds=200)

val_pred = model.predict(valid_matrix, ntree_limit=model.best_ntree_limit)

test_pred = model.predict(test_x , ntree_limit=model.best_ntree_limit)

if clf_name == "cat":

params = {'learning_rate': 0.05, 'depth': 5, 'l2_leaf_reg': 10, 'bootstrap_type': 'Bernoulli',

'od_type': 'Iter', 'od_wait': 50, 'random_seed': 11, 'allow_writing_files': False}

model = clf(iterations=20000, **params)

model.fit(trn_x, trn_y, eval_set=(val_x, val_y),

cat_features=[], use_best_model=True, verbose=500)

val_pred = model.predict(val_x)

test_pred = model.predict(test_x)

train[valid_index] = val_pred

test = test_pred / kf.n_splits

cv_scores.append(roc_auc_score(val_y, val_pred))

print(cv_scores)

print("%s_scotrainre_list:" % clf_name, cv_scores)

print("%s_score_mean:" % clf_name, np.mean(cv_scores))

print("%s_score_std:" % clf_name, np.std(cv_scores))

return train, test

def lgb_model(x_train, y_train, x_test):

lgb_train, lgb_test = cv_model(lgb, x_train, y_train, x_test, "lgb")

return lgb_train, lgb_test

def xgb_model(x_train, y_train, x_test):

xgb_train, xgb_test = cv_model(xgb, x_train, y_train, x_test, "xgb")

return xgb_train, xgb_test

def cat_model(x_train, y_train, x_test):

cat_train, cat_test = cv_model(CatBoostRegressor, x_train, y_train, x_test, "cat")

lgb_train, lgb_test = lgb_model(x_train, y_train, x_test)

************************************ 1 ************************************

Training until validation scores don't improve for 200 rounds

[200] training's auc: 0.749225 valid_1's auc: 0.729679

[400] training's auc: 0.765075 valid_1's auc: 0.730496

[600] training's auc: 0.778745 valid_1's auc: 0.730435

Early stopping, best iteration is:

[455] training's auc: 0.769202 valid_1's auc: 0.730686

[0.7306859913754798]

************************************ 2 ************************************

Training until validation scores don't improve for 200 rounds

[200] training's auc: 0.749221 valid_1's auc: 0.731315

[400] training's auc: 0.765117 valid_1's auc: 0.731658

[600] training's auc: 0.778542 valid_1's auc: 0.731333

Early stopping, best iteration is:

[407] training's auc: 0.765671 valid_1's auc: 0.73173

[0.7306859913754798, 0.7317304414673989]

************************************ 3 ************************************

Training until validation scores don't improve for 200 rounds

[200] training's auc: 0.748436 valid_1's auc: 0.732775

[400] training's auc: 0.764216 valid_1's auc: 0.733173

Early stopping, best iteration is:

[386] training's auc: 0.763261 valid_1's auc: 0.733261

[0.7306859913754798, 0.7317304414673989, 0.7332610441015461]

************************************ 4 ************************************

Training until validation scores don't improve for 200 rounds

[200] training's auc: 0.749631 valid_1's auc: 0.728327

[400] training's auc: 0.765139 valid_1's auc: 0.728845

Early stopping, best iteration is:

[286] training's auc: 0.756978 valid_1's auc: 0.728976

[0.7306859913754798, 0.7317304414673989, 0.7332610441015461, 0.7289759386807912]

************************************ 5 ************************************

Training until validation scores don't improve for 200 rounds

[200] training's auc: 0.748414 valid_1's auc: 0.732727

[400] training's auc: 0.763727 valid_1's auc: 0.733531

[600] training's auc: 0.777489 valid_1's auc: 0.733566

Early stopping, best iteration is:

[524] training's auc: 0.772372 valid_1's auc: 0.733772

[0.7306859913754798, 0.7317304414673989, 0.7332610441015461, 0.7289759386807912, 0.7337723979789789]

lgb_scotrainre_list: [0.7306859913754798, 0.7317304414673989, 0.7332610441015461, 0.7289759386807912, 0.7337723979789789]

lgb_score_mean: 0.7316851627208389

lgb_score_std: 0.0017424259863954693

testA_result = pd.read_csv('../testA_result.csv')

roc_auc_score(testA_result['isDefault'].values, lgb_test)

0.7290917729487896

3.4 总结

特征工程是机器学习,甚至是深度学习中最为重要的一部分,在实际应用中往往也是所花费时间最多的一步。各种算法书中对特征工程部分的讲解往往少得可怜,因为特征工程和具体的数据结合的太紧密,很难系统地覆盖所有场景。本章主要是通过一些常用的方法来做介绍,例如缺失值异常值的处理方法详细对任何数据集来说都是适用的。但对于分箱等操作本章给出了具体的几种思路,需要读者自己探索。在特征工程中比赛和具体的应用还是有所不同的,在实际的金融风控评分卡制作过程中,由于强调特征的可解释性,特征分箱尤其重要。学有余力同学可以自行多尝试,希望大家在本节学习中有所收获。

1262

1262

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言