时间序列 线性回归 区别

In the last tutorial , we saw how we could express the probabilistic form of the best linear predictor of a future observation based on the data at hand. We will see how to implement this in R later! In this article, we will study an important class of time series: linear processes. Let’s jump right into it!

在上一教程中 ,我们看到了如何基于手头的数据来表达未来观察的最佳线性预测变量的概率形式。 稍后我们将看到如何在R中实现这一点! 在本文中,我们将研究重要的时间序列类别: 线性过程。 让我们跳进去吧!

q相关和强平稳性 (q-correlation and strong stationarity)

How can more rigorously define the stationarity of time series? How about “semi-stationarity”? We use the concept of q-correlation to do this.

如何更严格地定义时间序列的平稳性? “半平稳性”怎么样? 我们使用q相关的概念来做到这一点。

A time-series process is called strictly stationary or strongly stationary if

时间序列过程称为严格平稳或强平稳,如果

that is, if the joint distribution of the observations X_{1}, …, X_{n} is the same as the one of the h-lagged set of observations.

也就是说,如果观测值X_ {1},…,X_ {n}的联合分布与h滞后观测值之一相同。

Properties

物产

All elements of a strongly stationary time series are identically distributed (but not necessarily independent!)

高度平稳的时间序列的所有元素都是相同分布的 (但不一定是独立的!)

- The distribution of any subset of observations is the same as the h-lagged set 观察的任何子集的分布与h滞后集相同

Finite second moment implies weakly stationarity

有限的第二时刻意味着平稳性较弱

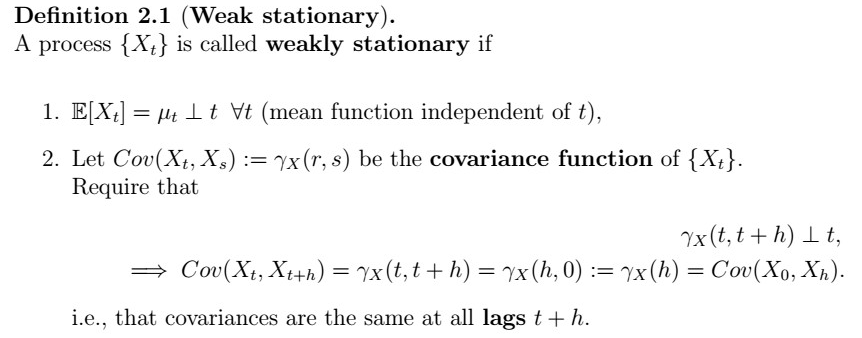

For convenience, here’s once more the definition of weak stationarity:

为了方便起见,这里再次给出弱平稳性的定义:

Note that strong stationarity is a much stronger condition! There are two important things to notice:

请注意,强烈的平稳性是更强的条件! 有两件事要注意:

Strong stationarity implies weak stationarity, but the opposite is not true!

平稳性强意味着平稳性弱 ,但事实并非如此!

The I.I.D process is strongly stationary.

IID过程是非常固定的 。

The main question is: how do we construct / how can we characterize stationary processes? In particular, if we know that the IID is stationary, perhaps there is some mapping to more general sequences. In such a case, how can we determine their “level of stationarity”? The following concepts.

主要问题是: 我们如何构建/如何表征平稳过程? 特别是,如果我们知道IID是固定的,则可能存在一些映射到更通用的序列。 在这种情况下,我们如何确定他们的“平稳程度”? 以下概念。

q相关性和q相关性 (q-dependence and q-correlation)

What the previous proposition is saying is that if we have an IID sequence, under certain conditions, we can construct a new series that is also strongly stationary, using some function g. Further, we can define q-dependence by saying that observations |t-s| lags apart are independent, but everything in between is dependent, and similarly for correlation.

先前的命题是说,如果我们有一个IID序列,则在某些条件下,我们可以使用某些函数g构造一个也非常平稳的新序列。 此外,我们可以通过说| ts |来定义q-依赖性 。 滞后是独立的,但是介于两者之间的所有事物都是相关的,并且类似地进行相关。

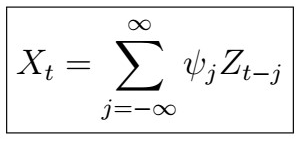

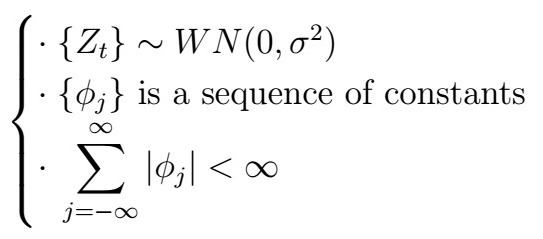

线性过程 (Linear Processes)

Now we finally get to one of the most important parts of Time Series Analysis: linear processes.

现在,我们终于可以了解时间序列分析中最重要的部分之一: 线性过程。

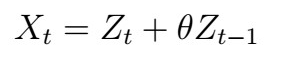

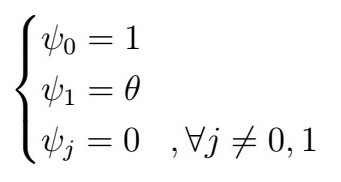

Example: MA(1)

示例:MA(1)

The MA(1) process

MA(1)过程

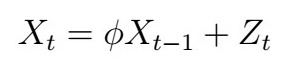

Example: AR(1)

示例:AR(1)

The AR(1) process

AR(1)流程

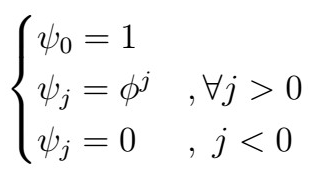

and we have that

而且我们有

If you are curious about why the coefficients are that way, you can attempt to solve the recursion by plugging back the definition of X_{t} substituting {t-1}. Note that we have to play the restriction on the AR(1) coefficients so that it satisfies the conditions of a linear process as we described above.

如果您对为什么采用这种系数感到好奇,则可以尝试通过插入X_ {t}代替{t-1}的定义来解决递归问题。 请注意,我们必须对AR(1)系数进行限制,以使其满足如上所述的线性过程的条件。

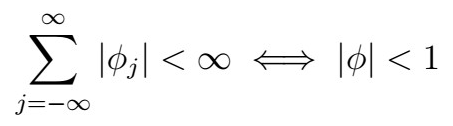

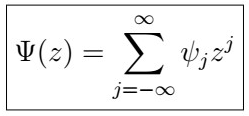

关于后向运算符的线性过程 (Linear processes in terms of the backward operator)

Remember the backward shift operator that we saw back in the differencing section? We can also use it to represent linear processes.

还记得我们在微分部分中看到的向后移位运算符吗? 我们还可以使用它来表示线性过程。

That is, we define the Psi operator as the infinite polynomial above, in which each term is exponentiated accordingly. If we plug in the backward shift operator, we then have a concrete way to represent the linear process briefly! This will become very useful to represent a more complex process without having to write down everything explicitly. Another way to see it is that we can see a linear process as an operation applied to the noise at time t.

也就是说,我们将Psi运算符定义为上面的无穷多项式,其中每个项相应地取幂。 如果我们插入后移运算符,那么我们就有一种具体的方法来简要表示线性过程! 这对于表示更复杂的过程而不必显式写下所有内容将非常有用。 另一种看待它的方式是,我们可以将线性过程视为在时间t处应用于噪声的运算。

下次 (Next time)

That’s it for today! Next time, we will continue studying some more properties of the linear process, along with some interesting propositions, and other useful operators commonly used when dealing with Time Series. Until then!

今天就这样! 下次,我们将继续研究线性过程的更多属性,以及一些有趣的主张,以及在处理时间序列时常用的其他有用的运算符。 直到那时!

上次 (Last time)

Prediction 1 → Best Linear Predictors II

主页 (Main page)

跟我来 (Follow me at)

时间序列 线性回归 区别

2872

2872

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言