Qlib的代码是以一个比较“松散”的结构,每一个模块都尽量做到可以最大程度的复用。这一点很好支撑我们的量化系统。即能够最大复用它的工程能力,又可以自主发展我们想要的功能。

今天看一下Qlib的投资组合策略。

传统的量化回测策略不同在于,Qlib的策略输出是由模型输出预测好的分数,由这个分数来构建投资组合。

策略的基类是qlib.strategy.base.BaseStrategy

class BaseStrategy:

"""Base strategy for trading"""

def __init__(

self,

outer_trade_decision: BaseTradeDecision = None,

level_infra: LevelInfrastructure = None,

common_infra: CommonInfrastructure = None,

trade_exchange: Exchange = None,

):

BaseStrategy是一个抽象类,就是定义了一些基础参数。

它的一个子类是ModelStrategy,顾名思义,基于模型的预测来交易的类。

它传入两个参数,一个是模型,一个是数据集。

class ModelStrategy(BaseStrategy):

"""Model-based trading strategy, use model to make predictions for trading"""

def __init__(

self,

model: BaseModel,

dataset: DatasetH,

outer_trade_decision: BaseTradeDecision = None,

level_infra: LevelInfrastructure = None,

common_infra: CommonInfrastructure = None,

**kwargs,

):

"""

Parameters

----------

model : BaseModel

the model used in when making predictions

dataset : DatasetH

provide test data for model

kwargs : dict

arguments that will be passed into `reset` method

"""

super(ModelStrategy, self).__init__(outer_trade_decision, level_infra, common_infra, **kwargs)

self.model = model

self.dataset = dataset

self.pred_scores = convert_index_format(self.model.predict(dataset), level="datetime")

if isinstance(self.pred_scores, pd.DataFrame):

self.pred_scores = self.pred_scores.iloc[:, 0]

使用model.predict(dataset)生成预测分数pred_scores。

源码中可以看出,qlib实现了两个关于强化学习的策略类,但它们都还没有具体的实现类。

传入重要参数是policy。

class RLStrategy(BaseStrategy):

"""RL-based strategy"""

def __init__(

self,

policy,

outer_trade_decision: BaseTradeDecision = None,

level_infra: LevelInfrastructure = None,

common_infra: CommonInfrastructure = None,

**kwargs,

):

"""

Parameters

----------

policy :

RL policy for generate action

"""

super(RLStrategy, self).__init__(outer_trade_decision, level_infra, common_infra, **kwargs)

self.policy = policy

还有一个子类,带state和action的翻译器的类。

class RLIntStrategy(RLStrategy):

"""(RL)-based (Strategy) with (Int)erpreter"""

def __init__(

self,

policy,

state_interpreter: Union[dict, StateInterpreter],

action_interpreter: Union[dict, ActionInterpreter],

outer_trade_decision: BaseTradeDecision = None,

level_infra: LevelInfrastructure = None,

common_infra: CommonInfrastructure = None,

**kwargs,

):

"""

Parameters

----------

state_interpreter : Union[dict, StateInterpreter]

interpretor that interprets the qlib execute result into rl env state

action_interpreter : Union[dict, ActionInterpreter]

interpretor that interprets the rl agent action into qlib order list

start_time : Union[str, pd.Timestamp], optional

start time of trading, by default None

end_time : Union[str, pd.Timestamp], optional

end time of trading, by default None

"""

super(RLIntStrategy, self).__init__(policy, outer_trade_decision, level_infra, common_infra, **kwargs)

self.policy = policy

self.state_interpreter = init_instance_by_config(state_interpreter, accept_types=StateInterpreter)

self.action_interpreter = init_instance_by_config(action_interpreter, accept_types=ActionInterpreter)

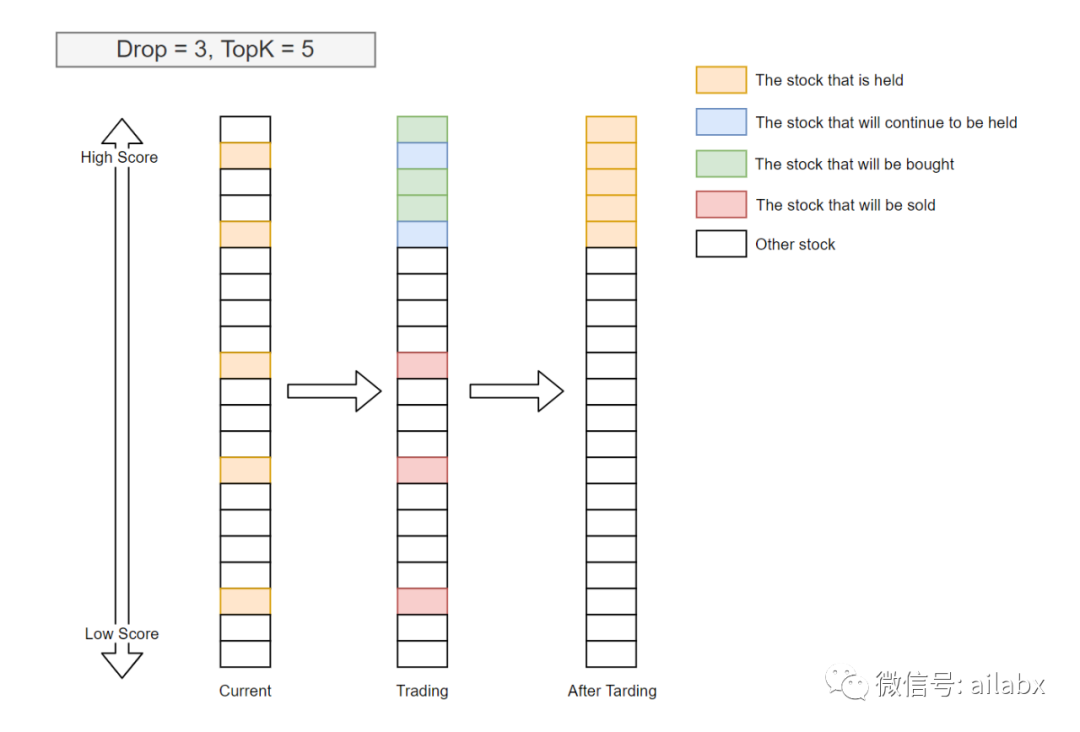

当前qlib仅有一个真正的策略实现类:TopKDropoutStrategy,继承自ModelStrategy。

class TopkDropoutStrategy(ModelStrategy):

# TODO:

# 1. Supporting leverage the get_range_limit result from the decision

# 2. Supporting alter_outer_trade_decision

# 3. Supporting checking the availability of trade decision

def __init__(

self,

model,

dataset,

topk,

n_drop,

method_sell="bottom",

method_buy="top",

risk_degree=0.95,

hold_thresh=1,

only_tradable=False,

trade_exchange=None,

level_infra=None,

common_infra=None,

**kwargs,

):

它的核心逻辑如下:

TopK=5,表示持有分数最高的前5支股票;Drop=3,TopK好理解,就是得分最高的前N个,但DropN这个有点奇怪,代码里解释是要提高换手率,这有点不符合交易逻辑,可以把这个设置成零。

它的核心函数是generate_trade_decision,类似传统回测系统里的on_bar。

传统回测系统里的on_bar会自己调api执行这些订单,而qlib只是返回这些order_list,这样倒也简洁。

def generate_trade_decision(self, execute_result=None):

# get the number of trading step finished, trade_step can be [0, 1, 2, ..., trade_len - 1]

其实,这里的逻辑,就是“轮动”策略,传统量化里的动量轮动,我们就是取动量最大的前N名持有。区别在于,根据当前的bar的指标,规则选择,但多支股票轮动最终一定会有一个排序,就是类似这个topK的逻辑。而规则就是模型给出的pred_score。

最后backtest_loop,调用strategy每一步产生交易订单,交给执行器去执行。

with tqdm(total=trade_executor.trade_calendar.get_trade_len(), desc="backtest loop") as bar:

_execute_result = None

while not trade_executor.finished():

_trade_decision: BaseTradeDecision = trade_strategy.generate_trade_decision(_execute_result)

_execute_result = yield from trade_executor.collect_data(_trade_decision, level=0)

bar.update(1)

客观讲,qlib这一块写得不好,也是我打算使用自己的回测引擎的原因。我仔细读过像Backtrader,PyalgoTrade的源码,不知为何qlib重新造了一个逻辑不太一样的轮子。

1428

1428

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言