一、向量自回归模型简介

经典回归模型都存在一个强加单向关系的局限性,即被解释变量受到解释变量的影响,但反之不成立。然而,在许多情况下所有变量都相互影响。向量自回归(VAR)模型允许这类双向反馈关系,所有变量都被平等对待,即所有变量都是内生的,变量之间平等地相互影响。VAR模型将单变量自回归的思想扩展到多元时间序列回归,是单变量自回归模型的一般化。它由系统中每个变量对应一个方程组成。每个方程的等式右边都包含一个常数项和系统中所有变量的滞后项。两变量P阶VAR模型的一般表达式如下:

如果序列是平稳的,我们直接根据数据拟合 VAR 模型(称为“水平 VAR”);如果序列非平稳,则将数据进行差分使其变得平稳,在此基础上拟合 VAR 模型(称为“差分 VAR”)。在这两种情况下,模型都是利用最小二乘法对方程逐一进行估计的。对于每个方程,通过最小化平方和的值来估计参数。

二、一个实例:使用VAR模型进行短期预测

(一)数据来源

本期应用案例为:Yash P. Mehra(1994)的文章《工资增长和通货膨胀过程:一种经验方法》所使用的时间序列数据集。

原文如下:

Mehra,Yash P. "Wage growth and the inflation process: an empiricalapproach." Cointegration. Palgrave Macmillan, London, 1994. 147-159.

CSV格式的数据集可以在下面网址下载。https://raw.githubusercontent.com/selva86/datasets/master/Raotbl6.csv(二)变量该数据集是8个变量的季度时间序列,变量如下:

1. rgnp :Real GNP.

2. pgnp :Potential real GNP.

3. ulc :Unit labor cost.

4. gdfco: Fixed weight deflator for personal consumption expenditure excluding food andenergy.

5. gdf :Fixed weight GNP deflator.

6. gdfim: Fixed weight import deflator.

7. gdfcf: Fixed weight deflator for food in personal consumption expenditure.

8. gdfce: Fixed weight deflator for energy in personal consumption expenditure.

三、计算过程与Python代码

#(1)载入包

importpandas as pd

importnumpy as np

importmatplotlib.pyplot as plt

%matplotlibinline

# ImportStatsmodels

fromstatsmodels.tsa.api import VAR

fromstatsmodels.tsa.stattools import adfuller

fromstatsmodels.tools.eval_measures import rmse, aic

#(2)导入数据

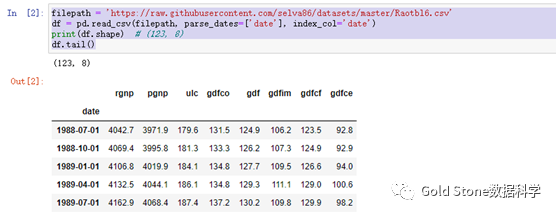

filepath= 'https://raw.githubusercontent.com/selva86/datasets/master/Raotbl6.csv'

df =pd.read_csv(filepath, parse_dates=['date'], index_col='date')

print(df.shape) # (123, 8)

df.tail()

#(3)时间序列可视化

# Plot

fig,axes = plt.subplots(nrows=4, ncols=2, dpi=120, figsize=(10,6))

for i,ax in enumerate(axes.flatten()):

data = df[df.columns[i]]

ax.plot(data, color='red', linewidth=1)

# Decorations

ax.set_ti

最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

11万+

11万+

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言