5.0程序运行前的库

import pandas as pd

import numpy as np

import statsmodels.api as sm

import matplotlib.pyplot as plt

from statsmodels.stats.outliers_influence import variance_inflation_factor5.1引言

定性变量可以用实型变量或虚拟变量来表示,对于定性变量,其一般取值为0或1,表明观测属于两个可能类别中的一个;示性变量也可以区分3个或3个以上的类别

5.2薪水调查数据

(一)目的:明确并量化那些决定薪水差异的变量;也可用来检验公司的薪水管理制度是否得到遵行

(二)响应变量为薪水S;预测变量:工作年数X,教育E[高中1,硕士2,更高3],管理M[人在管理职位1;其他职位0]

两个示性变量表示三种教育水平,这两个变量使得我们可以衡量受教育水平对薪水差异的影响

data1=pd.read_csv('F:\linear regression\chapter 5\Table 5.1.csv')

data1.columns=['S','X','E','M']#X工作年数,E教育,M为是否为在职管理者

E=data1['E']

X=data1['X']# 我们需要对表格中的数据进行定性的表示

这样做的目的:用来区分两个管理类别的示性变量只需要一个,示性变量取值为0的类别为基础类别,因为示性变量的回归系数是相对于对照组的增量

#哑变量 示性变量

#首先我们将定性变量E转换为虚拟变量

dummies=pd.get_dummies(data1['E'],'E')

#将E列展开,对E中插入我们想要的列表的数据

#读取第1列的值

#读取第2列的值

data1.insert(2,'E_1',dummies.iloc[:,0])

data1.insert(3,'E_2',dummies.iloc[:,1])

data1.insert(1,'constant',1)

#去掉哑变量

data1=data1.drop('E',axis=1)#删除其中的E教育所在行列,用0,1来表示

data1Table 5.3 Regression Analysis of Salary Survey Data

ols_1=(sm.OLS(data1['S'],data1[data1.columns[1:6]].astype(float))).fit()

print(ols_1.summary()) OLS Regression Results

==============================================================================

Dep. Variable: S R-squared: 0.957

Model: OLS Adj. R-squared: 0.953

Method: Least Squares F-statistic: 226.8

Date: Wed, 13 Dec 2023 Prob (F-statistic): 2.23e-27

Time: 21:59:45 Log-Likelihood: -381.63

No. Observations: 46 AIC: 773.3

Df Residuals: 41 BIC: 782.4

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

constant 1.103e+04 383.217 28.787 0.000 1.03e+04 1.18e+04

X 546.1840 30.519 17.896 0.000 484.549 607.819

E_1 -2996.2103 411.753 -7.277 0.000 -3827.762 -2164.659

E_2 147.8249 387.659 0.381 0.705 -635.069 930.719

M 6883.5310 313.919 21.928 0.000 6249.559 7517.503

==============================================================================

Omnibus: 2.293 Durbin-Watson: 2.237

Prob(Omnibus): 0.318 Jarque-Bera (JB): 1.362

Skew: -0.077 Prob(JB): 0.506

Kurtosis: 2.171 Cond. No. 35.4

==============================================================================

from scipy.stats import t,f

t(41).isf(0.025)2.019540963982894

5.3 交互作用变量

模型设定问题

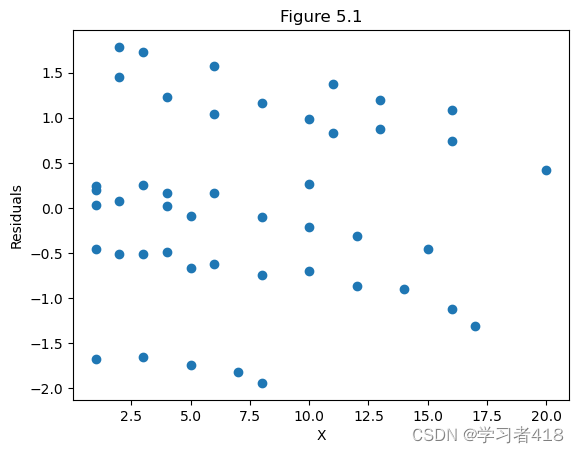

Figure 5.1 对工作年数的标准化残差图

首先这幅图存在三个或多个的残差水平。

outliers=ols_1.get_influence()

res1=outliers.resid_studentized_internal

plt.scatter(data1['X'],res1)

plt.xlabel('X')

plt.ylabel('Residuals')

plt.title('Figure 5.1')

plt.show()

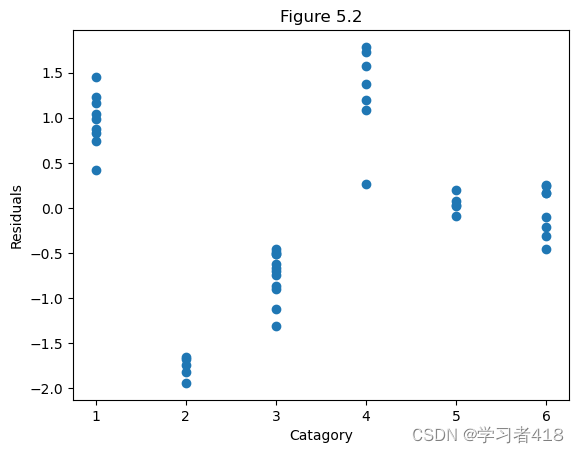

Figure 5.2 对E-M组合类别变量的标准化残差图

分为6种;从表中不难发现:残差或者几乎全为正或者几乎全为负,这表明给出的模型并未充分解释薪水和工作年数,教育,以及管理变量之间的关系【总的概括而言:数据中一些隐含的数据结构并未被挖掘出来】

em=-1+2*E+data1['M']

plt.scatter(em,res1)

plt.xlabel('Catagory')

plt.ylabel('Residuals')

plt.title('Figure 5.2')

plt.show()

Table 5.4 扩展模型

教育和管理两者不可加,但却承认两个变量有交互效应的模型

data1['E1M']=data1['E_1']*data1['M']

data1['E2M']=data1['E_2']*data1['M']

data1(一)首先,我们对扩展后的模型有一个初步的了解,先做回归分析

ols_2=(sm.OLS(data1['S'],data1[data1.columns[1:]].astype(float))).fit()

print(ols_2.summary())OLS Regression Results

==============================================================================

Dep. Variable: S R-squared: 0.999

Model: OLS Adj. R-squared: 0.999

Method: Least Squares F-statistic: 5517.

Date: Wed, 13 Dec 2023 Prob (F-statistic): 1.67e-55

Time: 21:59:53 Log-Likelihood: -298.74

No. Observations: 46 AIC: 611.5

Df Residuals: 39 BIC: 624.3

Df Model: 6

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

constant 1.12e+04 79.065 141.698 0.000 1.1e+04 1.14e+04

X 496.9870 5.566 89.283 0.000 485.728 508.246

E_1 -1730.7483 105.334 -16.431 0.000 -1943.806 -1517.690

E_2 -349.0777 97.568 -3.578 0.001 -546.427 -151.728

M 7047.4120 102.589 68.695 0.000 6839.906 7254.918

E1M -3066.0351 149.330 -20.532 0.000 -3368.084 -2763.986

E2M 1836.4879 131.167 14.001 0.000 1571.177 2101.799

==============================================================================

Omnibus: 74.761 Durbin-Watson: 2.244

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1037.873

Skew: -4.103 Prob(JB): 4.25e-226

Kurtosis: 24.776 Cond. No. 83.4

==============================================================================

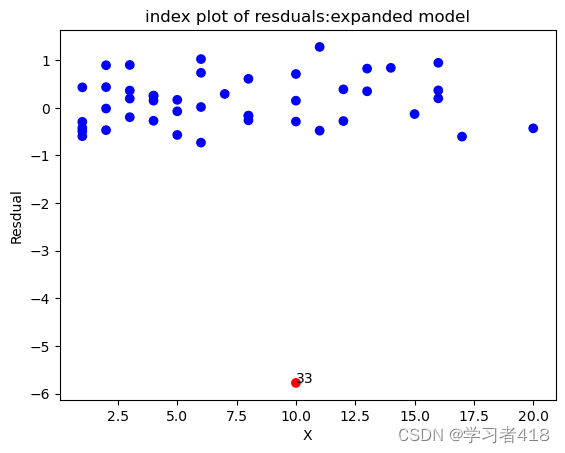

Figur 5.3 扩展模型对工作年数的标准化残差图

此模型过高预测了这一点上的薪水,检查原数据集这个观测,发现这个人比其他特征相似的人年薪低几百元,为了确保这一观测不过度影响回归估计,将它去掉重新做回归

n=len(X)

index=np.arange(1,46)

outliers=ols_2.get_influence()

res2=outliers.resid_studentized_internal

#找出outliers

col=[]

for i in range(0,n):

if abs(res2[i])>2:

col.append('r')

plt.annotate(index[i],xy=(X[i],res2[i]))#散点图注释

else:

col.append('b')

plt.scatter(X,res2,c=col)

plt.xlabel('X')

plt.ylabel('Resdual')

plt.title('index plot of resduals:expanded model')

plt.show()

outlier 为第33个观测值,需要删除¶

data1_1=data1.drop(32,axis=0)#第1列的第33个观测值

ols_3=(sm.OLS(data1_1['S'],data1_1[data1_1.columns[1:]].astype(float))).fit()

print(ols_3.summary())OLS Regression Results

==============================================================================

Dep. Variable: S R-squared: 1.000

Model: OLS Adj. R-squared: 1.000

Method: Least Squares F-statistic: 3.543e+04

Date: Wed, 13 Dec 2023 Prob (F-statistic): 1.30e-69

Time: 21:59:56 Log-Likelihood: -249.34

No. Observations: 45 AIC: 512.7

Df Residuals: 38 BIC: 525.3

Df Model: 6

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

constant 1.12e+04 30.533 366.802 0.000 1.11e+04 1.13e+04

X 498.4178 2.152 231.640 0.000 494.062 502.774

E_1 -1741.3359 40.683 -42.803 0.000 -1823.693 -1658.979

E_2 -357.0423 37.681 -9.475 0.000 -433.324 -280.761

M 7040.5801 39.619 177.707 0.000 6960.376 7120.785

E1M -3051.7633 57.674 -52.914 0.000 -3168.519 -2935.008

E2M 1997.5306 51.785 38.574 0.000 1892.697 2102.364

==============================================================================

Omnibus: 1.462 Durbin-Watson: 2.438

Prob(Omnibus): 0.482 Jarque-Bera (JB): 1.171

Skew: 0.177 Prob(JB): 0.557

Kurtosis: 2.293 Cond. No. 82.5

==============================================================================

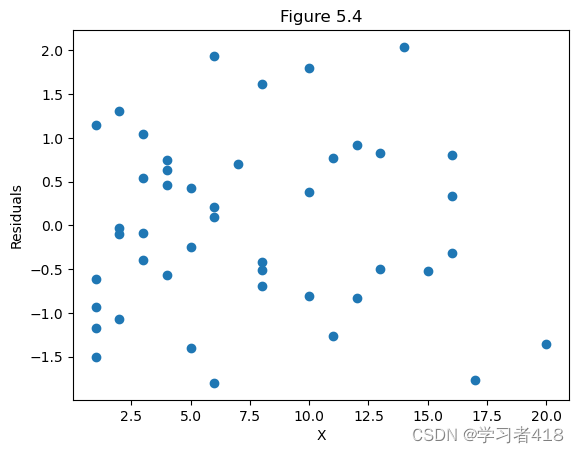

Figure 5.4

删除第33个观测值的扩展模型中对X的标准化残差 新的残差图与原可加模型类似的残差图相比更令人满意

outliers=ols_3.get_influence()

res3=outliers.resid_studentized_internal

plt.scatter(data1_1['X'],res3)

plt.xlabel('X')

plt.ylabel('Residuals')

plt.title('Figure 5.4')

plt.show()

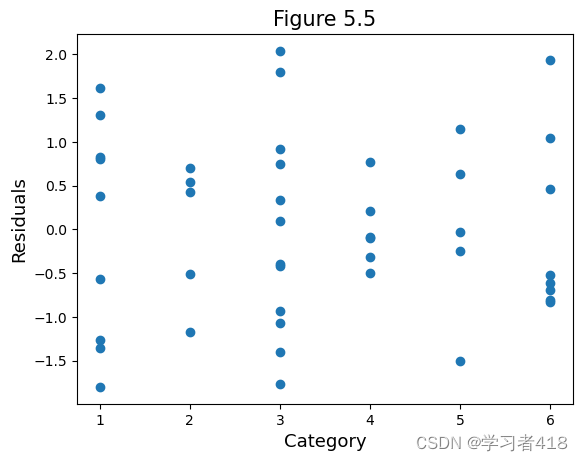

对EM组合变量的标准化残差(扩展,删33)

每个组合类的残差关于0的分布对称

E=E.drop(32)

EM=-1+2*E+data1_1['M']

plt.scatter(EM,res3)

plt.xlabel('Category',size=13)

plt.ylabel('Residuals',size=13)

plt.title('Figure 5.5',size=15)

plt.show()

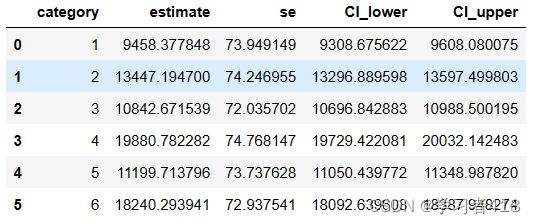

求取对应的t值

from scipy.stats import t,f

t(38).isf(0.025)2.0243941645751367

beta=ols_3.params

x0=np.vstack([[1,1,1,1,1,1],[0,0,0,0,0,0],[1,1,0,0,0,0],[0,0,1,1,0,0],[0,1,0,1,0,1],[0,1,0,0,0,0],[0,0,0,1,0,0]]).T

yuce=x0.dot(beta)

#计算标准误

X=data1_1[['constant','X','E_1','E_2','M','E1M','E2M']].values

fit=ols_3.fittedvalues

sigma=((np.sum((data1_1['S']-fit)**2))/38)**0.5

s_e=[]

for i in range(6):

x01=x0[i,:].reshape(7,1)

se=x01.T.dot(np.linalg.inv(X.T.dot(X))).dot(x01)

se=((se+1)**0.5)*sigma

s_e.insert(i,float(se))

#计算预测值的预测区间

upper=[]

lower=[]

for i in range(6):

upper.insert(i,yuce[i]+t.isf(0.025,38)*s_e[i])

lower.insert(i,yuce[i]-t.isf(0.025,38)*s_e[i])

table=pd.DataFrame()

table['category']=[1,2,3,4,5,6]

table['estimate']=yuce

table['se']=s_e

table['CI_lower']=lower

table['CI_upper']=upper

table

5.4 回归方程系统:两个组的比较

5.4.0数据导入以及需要用到的库

import pandas as pd

import numpy as np

import statsmodels.api as sm

import matplotlib.pyplot as plt

from statsmodels.stats.outliers_influence import variance_inflation_factor

data2=pd.read_csv('F:\linear regression\chapter 5\Table 5.7.csv')

data2.columns=['TEST','RACE','JPERF']

RACE=data2['RACE']

JPERF=data2['JPERF']data2.insert(1,'constant',1)

ols_4=(sm.OLS(data2['JPERF'],data2[['constant','TEST']].astype(float))).fit()

print(ols_4.summary())OLS Regression Results

==============================================================================

Dep. Variable: JPERF R-squared: 0.517

Model: OLS Adj. R-squared: 0.490

Method: Least Squares F-statistic: 19.25

Date: Wed, 13 Dec 2023 Prob (F-statistic): 0.000356

Time: 22:09:05 Log-Likelihood: -36.614

No. Observations: 20 AIC: 77.23

Df Residuals: 18 BIC: 79.22

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

constant 1.0350 0.868 1.192 0.249 -0.789 2.859

TEST 2.3605 0.538 4.387 0.000 1.230 3.491

==============================================================================

Omnibus: 0.324 Durbin-Watson: 2.896

Prob(Omnibus): 0.850 Jarque-Bera (JB): 0.483

Skew: -0.186 Prob(JB): 0.785

Kurtosis: 2.336 Cond. No. 5.26

==============================================================================

from prettytable import PrettyTable#创建表格

label1=['Source','Sum of Squares','d.f.','Mean Square']

table=PrettyTable(label1)

table.add_row(['Regression',ols_4.df_model*ols_4.mse_model,ols_4.df_model,ols_4.mse_model])

table.add_row(['Residuals',ols_4.ssr,ols_4.df_resid,ols_4.mse_resid])

table.add_column('F',[ols_4.fvalue,'--'])

print(table)

+------------+--------------------+------+--------------------+------------------+ | Source | Sum of Squares | d.f. | Mean Square | F | +------------+--------------------+------+--------------------+------------------+ | Regression | 48.7229581716978 | 1.0 | 48.7229581716978 | 19.2461274204537 | | Residuals | 45.568296828302195 | 18.0 | 2.5315720460167888 | -- | +------------+--------------------+------+--------------------+------------------+

data2['RACE*TEST']=data2['RACE']*data2['TEST']

ols_5=(sm.OLS(data2['JPERF'],data2[['constant','TEST','RACE','RACE*TEST']].astype(float))).fit()

print(ols_5.summary()) OLS Regression Results

==============================================================================

Dep. Variable: JPERF R-squared: 0.664

Model: OLS Adj. R-squared: 0.601

Method: Least Squares F-statistic: 10.55

Date: Wed, 13 Dec 2023 Prob (F-statistic): 0.000451

Time: 22:09:06 Log-Likelihood: -32.971

No. Observations: 20 AIC: 73.94

Df Residuals: 16 BIC: 77.92

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

constant 2.0103 1.050 1.914 0.074 -0.216 4.236

TEST 1.3134 0.670 1.959 0.068 -0.108 2.735

RACE -1.9132 1.540 -1.242 0.232 -5.179 1.352

RACE*TEST 1.9975 0.954 2.093 0.053 -0.026 4.021

==============================================================================

Omnibus: 3.377 Durbin-Watson: 3.015

Prob(Omnibus): 0.185 Jarque-Bera (JB): 1.330

Skew: 0.120 Prob(JB): 0.514

Kurtosis: 1.760 Cond. No. 13.8

==============================================================================

label2=['Source','Sum of Squares','d.f.','Mean Square']

table=PrettyTable(label2)

table.add_row(['Regression',ols_5.df_model*ols_5.mse_model,ols_5.df_model,ols_5.mse_model])

table.add_row(['Residuals',ols_5.ssr,ols_5.df_resid,ols_5.mse_resid])

table.add_column('F',[ols_5.fvalue,'--'])

print(table)+------------+-------------------+------+-------------------+-------------------+ | Source | Sum of Squares | d.f. | Mean Square | F | +------------+-------------------+------+-------------------+-------------------+ | Regression | 62.63578183766151 | 3.0 | 20.87859394588717 | 10.55291454406796 | | Residuals | 31.65547316233848 | 16.0 | 1.978467072646155 | -- | +------------+-------------------+------+-------------------+-------------------+

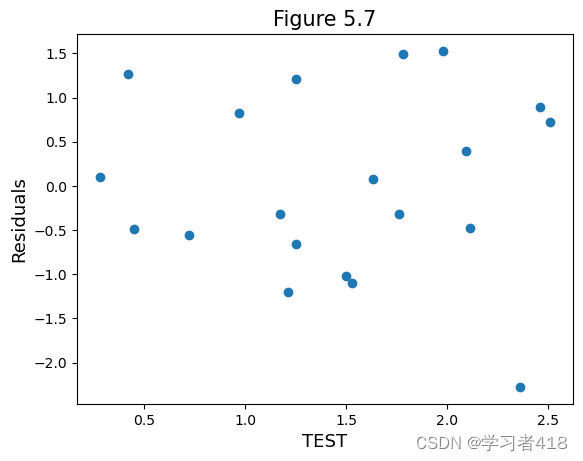

Figure 5.7 Model 1 对测试得分的标准化残差图

outliers=ols_4.get_influence()

res4=outliers.resid_studentized_internal

plt.scatter(data2['TEST'],res4)

plt.xlabel('TEST',size=13)

plt.ylabel('Residuals',size=13)

plt.title('Figure 5.7',size=15)

plt.show()

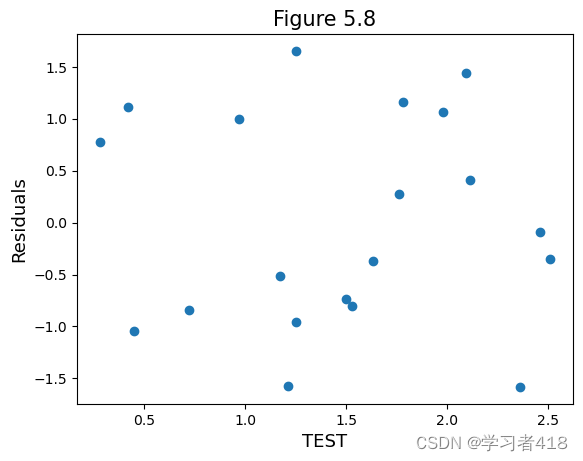

Figure 5.8 Model 3 对测试得分的标准化残差图

outliers=ols_5.get_influence()

res5=outliers.resid_studentized_internal

plt.scatter(data2['TEST'],res5)

plt.xlabel('TEST',size=13)

plt.ylabel('Residuals',size=13)

plt.title('Figure 5.8',size=15)

plt.show()

Figure 5.9 对Model 1 种族的标准化残差图

plt.scatter(data2['RACE'],res4)

plt.xlabel('RACE')

plt.ylabel('Residuals')

plt.title('Figure 5.9')

plt.show()

from scipy.stats import t,f

f.isf(0.05,2,16)3.63372346759163

SSE_4=sum(res4**2)

SSE_5=sum(res5**2)

print(SSE_4)

print(SSE_5)20.02709825217295 19.806440174731453

results_1=(sm.OLS(data2.iloc[0:10,3],data2.iloc[0:10,0:2])).fit()

print(results_1.summary())

results_2=(sm.OLS(data2.iloc[10:20,3],data2.iloc[10:20,0:2])).fit()

print(results_2.summary())OLS Regression Results

==============================================================================

Dep. Variable: JPERF R-squared: 0.779

Model: OLS Adj. R-squared: 0.751

Method: Least Squares F-statistic: 28.14

Date: Wed, 13 Dec 2023 Prob (F-statistic): 0.000724

Time: 22:20:37 Log-Likelihood: -15.637

No. Observations: 10 AIC: 35.27

Df Residuals: 8 BIC: 35.88

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

TEST 3.3109 0.624 5.305 0.001 1.872 4.750

constant 0.0971 1.035 0.094 0.928 -2.290 2.484

==============================================================================

Omnibus: 0.635 Durbin-Watson: 2.411

Prob(Omnibus): 0.728 Jarque-Bera (JB): 0.554

Skew: -0.161 Prob(JB): 0.758

Kurtosis: 1.893 Cond. No. 5.55

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: JPERF R-squared: 0.293

Model: OLS Adj. R-squared: 0.205

Method: Least Squares F-statistic: 3.320

Date: Wed, 13 Dec 2023 Prob (F-statistic): 0.106

Time: 22:20:37 Log-Likelihood: -17.211

No. Observations: 10 AIC: 38.42

Df Residuals: 8 BIC: 39.03

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

TEST 1.3134 0.721 1.822 0.106 -0.349 2.976

constant 2.0103 1.129 1.780 0.113 -0.593 4.614

==============================================================================

Omnibus: 2.077 Durbin-Watson: 2.880

Prob(Omnibus): 0.354 Jarque-Bera (JB): 0.932

Skew: 0.294 Prob(JB): 0.627

Kurtosis: 1.624 Cond. No. 5.01

==============================================================================

Figure 5.10

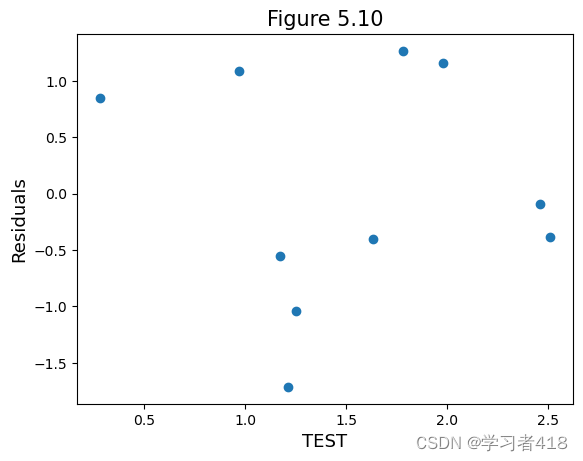

#图5.10

outliers=results_1.get_influence()

res1=outliers.resid_studentized_internal

plt.scatter(data2.loc[data2['RACE']==1,'TEST'],res1)

plt.xlabel('TEST',size=13)

plt.ylabel('Residuals',size=13)

plt.title('Figure 5.10',size=15)

plt.show()

Figure 5.11

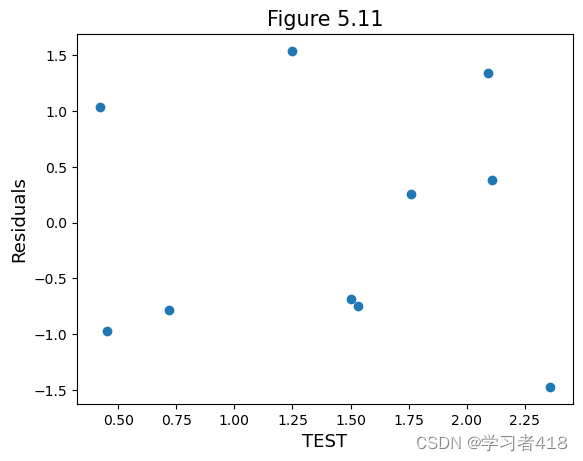

#图5.11

outliers=results_2.get_influence()

res2=outliers.resid_studentized_internal

plt.scatter(data2.loc[data2['RACE']==0,'TEST'],res2)

plt.xlabel('TEST',size=13)

plt.ylabel('Residuals',size=13)

plt.title('Figure 5.11',size=15)

plt.show()

ols_6=(sm.OLS(data2['JPERF'],data2[['constant','TEST','RACE']].astype(float))).fit()

print(ols_6.summary()) OLS Regression Results

==============================================================================

Dep. Variable: JPERF R-squared: 0.572

Model: OLS Adj. R-squared: 0.522

Method: Least Squares F-statistic: 11.38

Date: Sun, 17 Dec 2023 Prob (F-statistic): 0.000731

Time: 19:18:40 Log-Likelihood: -35.390

No. Observations: 20 AIC: 76.78

Df Residuals: 17 BIC: 79.77

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

constant 0.6120 0.887 0.690 0.500 -1.260 2.483

TEST 2.2988 0.522 4.400 0.000 1.197 3.401

RACE 1.0276 0.691 1.487 0.155 -0.430 2.485

==============================================================================

Omnibus: 0.251 Durbin-Watson: 3.028

Prob(Omnibus): 0.882 Jarque-Bera (JB): 0.437

Skew: -0.059 Prob(JB): 0.804

Kurtosis: 2.286 Cond. No. 5.72

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

label3=['Source','Sum of Squares','d.f.','Mean Square']

table=PrettyTable(label3)

table.add_row(['Regression',ols_6.df_model*ols_6.mse_model,ols_6.df_model,ols_6.mse_model])

table.add_row(['Residuals',ols_6.ssr,ols_6.df_resid,ols_6.mse_resid])

table.add_column('F',[ols_6.fvalue,'--'])

print(table)+------------+--------------------+------+-------------------+--------------------+ | Source | Sum of Squares | d.f. | Mean Square | F | +------------+--------------------+------+-------------------+--------------------+ | Regression | 53.96970908443848 | 2.0 | 26.98485454221924 | 11.377106626278483 | | Residuals | 40.321545915561515 | 17.0 | 2.371855642091854 | -- | +------------+--------------------+------+-------------------+--------------------+

from scipy.stats import t,f

f.isf(0.05,2,16)3.63372346759163

2270

2270

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言