作业内容:

在http://stat.ethz.ch/R-manual/R-devel/library/datasets/html/longley.html中

对数据Longley's Economic Regression Data进行了介绍,仔细阅读后做如下分析:(1) 检查复共线性;

(2) 使用主成分回归解决复共线性,选择适当个数的主成分;

(3) 使用岭回归解决复共线性,并采用不同方法估计岭参数。

我的答案(仅供参考)

#1、

kappa(cor(longley[,c(-1,-6)]))

#1746.892>1000 存在严重的复共线性

library(DAAG)

lm.reg<-lm(Employed~GNP+Unemployed+Armed.Forces+Population+Year,data=longley)

vif(lm.reg,digits=4)

# GNP Unemployed Armed.Forces Population Year

# 1034.000 23.260 3.152 225.700 732.600 膨胀因子大多大于10,存在严重的相关性

#2、

pca<-princomp(longley[,c(-1,-6)],cor=TRUE)

summary(pca,loadings=TRUE)

#Importance of components:

# Comp.1 Comp.2 Comp.3 Comp.4

#Standard deviation 1.8839994 1.0888267 0.50115614 0.110913452

#Proportion of Variance 0.7098908 0.2371087 0.05023149 0.002460359

#Cumulative Proportion 0.7098908 0.9469995 0.99723100 0.999691358

# Comp.5

#Standard deviation 0.039283711

#Proportion of Variance 0.000308642

#Cumulative Proportion 1.000000000

# Comp.1 Comp.2 Comp.3 Comp.4 Comp.5

#GNP -0.528 -0.179 -0.226 0.798

#Unemployed -0.352 -0.615 0.665 0.235

#Armed.Forces -0.235 0.779 0.577

#Population -0.527 -0.107 -0.635 -0.550

#Employed -0.514 -0.426 0.698 -0.242

#选择2-3个主成分即可

#3、

library(MASS)

result2<-lm.ridge(Employed~GNP+Unemployed+Armed.Forces+Population+Year,data=longley,data=longley,lambda=seq(0,100,0.01))

result2$lambda[which.min(result2$GCV)]

result2$coef[,which.min(result2$GCV)]

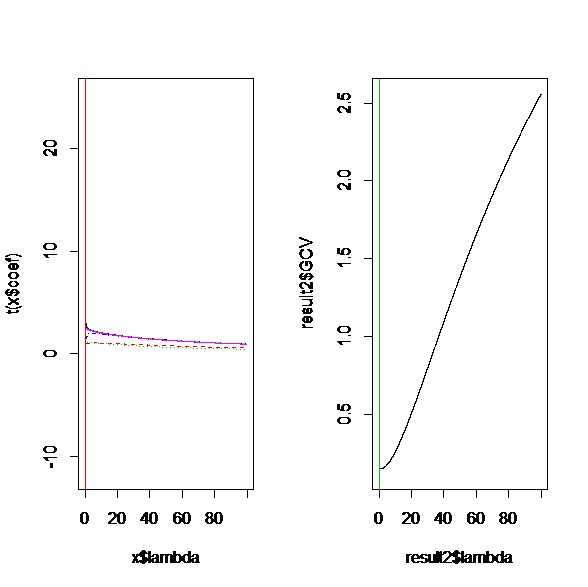

par(mfrow=c(1,2))

plot(result2)

abline(v=result2$lambda[which.min(result2$GCV)],col=2)

plot(result2$lambda,result2$GCV,type="l")

abline(v=result2$lambda[which.min(result2$GCV)],col=3)

select(result2)

# GNP Unemployed Armed.Forces Population Year

# 14.5822749 1.4631645 0.4374007 -7.8066243 2.5443023

# Employed

# -0.1067656

#使用岭际法得到的参数估计

#modified HKB estimator is 0.006836982 使用HB公式

#modified L-W estimator is 0.05267247

#smallest value of GCV at 0.01 使用岭际法得到的K值

920

920

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言