matlab

by lqx

预测模型的原理和方法

偏最小二乘回归模型

plsregress 函数

% 示例数据

X = [4.0 2.0 0.6;

4.2 2.1 0.59;

3.9 2.0 0.58;

4.3 2.1 0.62];

Y = [1.0 0.8;

0.9 0.7;

1.2 0.95;

1.1 0.78];

% 设置主成分数目

ncomp = 2;

% 构建 PLSR 模型并进行预测

[XL, YL, XS, YS, BETA, PCTVAR, MSE, stats] = plsregress(X, Y, ncomp);

% 进行预测

Xnew = [4.1 2.05 0.6];

Ypred = [1, Xnew] * BETA;

disp('预测结果:');

disp(Ypred);

% 示例数据集

X = [1500, 3, 1; % 特征矩阵 X

2000, 4, 2;

1200, 2, 1;

1800, 3, 1;

2500, 4, 2];

Y = [200000; 250000; 180000; 220000; 280000]; % 因变量 Y

% 拟合偏最小二乘回归模型

num_components = 2; % 提取的偏最小二乘回归系数的数量

[XL, YL, XS, YS, BETA, PCTVAR, MSE, stats] = plsregress(X, Y, num_components);

% 输出结果

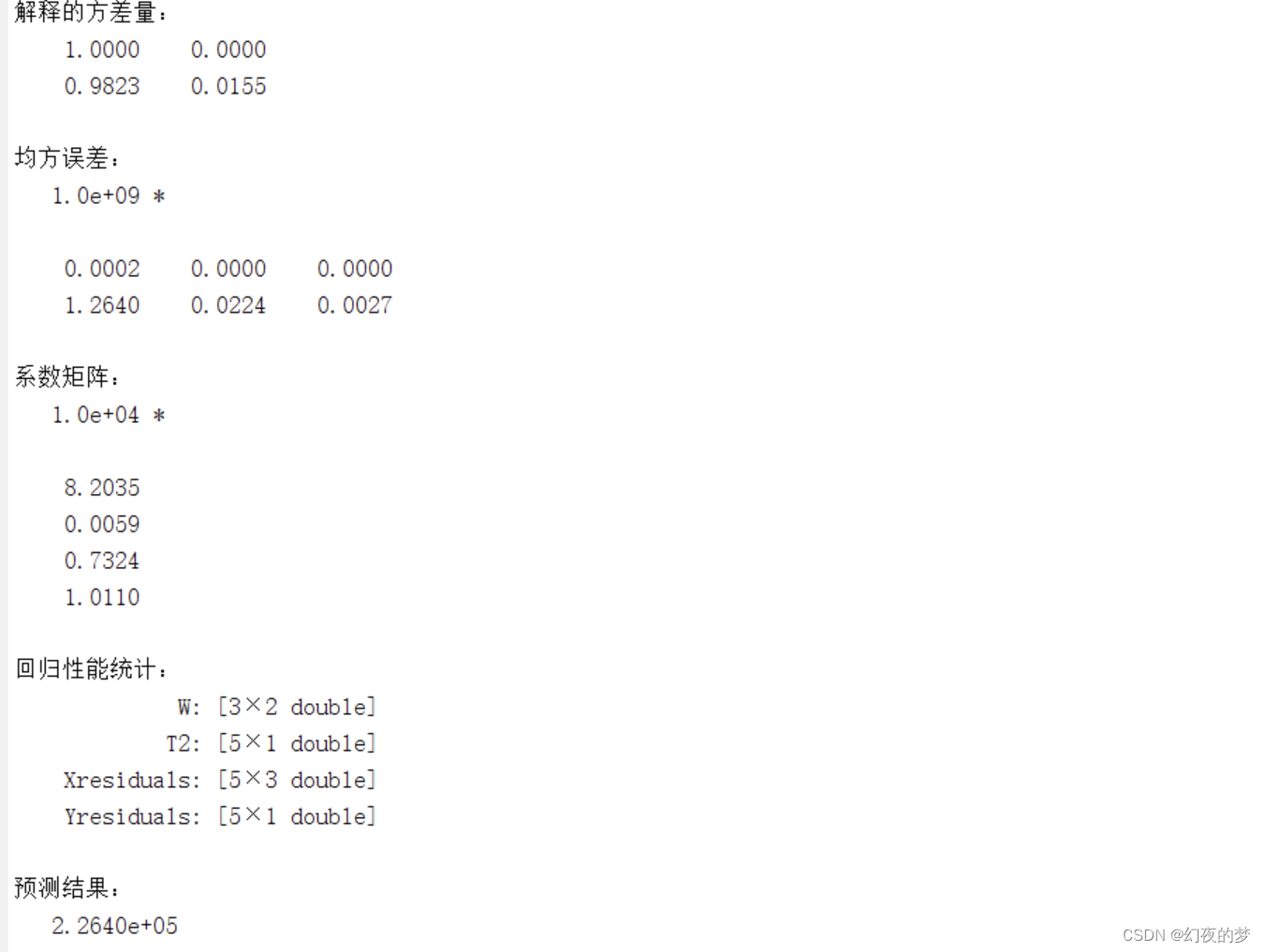

disp('解释的方差量:');

disp(PCTVAR);

disp('均方误差:');

disp(MSE);

disp('系数矩阵:');

disp(BETA);

disp('回归性能统计:');

disp(stats);

% 使用模型进行预测

newX = [1900, 3, 1]; % 新样本特征

pred = [1, newX] * BETA; % 预测因变量值

disp('预测结果:');

disp(pred);

4131

4131

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言