- Content

(1) Calculate the vector of mean returns and covariance matrix of returns for the ten industry portfolios. Create a table showing the mean returns and standard deviation of returns for the ten industry portfolios.

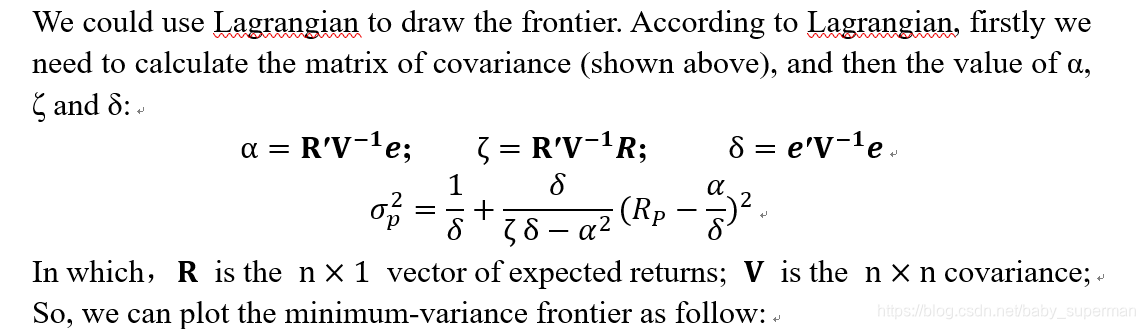

(2) Plot the minimum-variance frontier generated by the ten industry portfolios (x: standard deviation of return, range from 0% to 2%; y: mean return)

(3) Plot the efficient frontier (with the riskless asset) on the same plot

(4) Calculate the weights of the ten industry portfolios at the tangency portfolio

- code

file = 'Industry_Portfolios.xlsx'

df = pd.read_excel(file)

# describe df

df=DataFrame.drop(df,'Date',axis=1)

des=DataFrame.describe(df)

# caculate mean returns and covariance matrix of returns

table=des[1:3]

mean_return=np.mean(df,axis=0)

mean_return = np.array(mean_return/100)

covariance=np.cov(df/100,rowvar=0)

covariance=np.array(covariance)

e= np.ones(10)

rp=np.linspace(0.0013,0.02,100)

a = np.dot(np.dot(np.transpose(mean_return),(np.linalg.inv(covariance))),e)

b= np.dot(np.dot(np.transpose(mean_return),(np.linalg.inv(covariance))),mean_return)

c= np.dot(np.dot(np.transpose(e),(np.linalg.inv(covariance))),e)

minVariance =np.sqrt(1/c+c/(b*c-a**2)*(rp-a/c)**2)

#with riskless asset

rf=0.0013

minVariance1=np.sqrt((rp-rf)**2/(b-2*a*rf+c*rf**2))

plt.plot(minVariance,rp)

plt.plot(minVariance1,rp)

plt.xlabel("variance")

plt.ylabel("Rp")

plt.legend()

plt.show

plt.savefig('tupian.png')

# Calculate the weights of the ten industry portfolios at tangency portfolio

r_tg=(a*rf-b)/(c*rf-a)

lamda=(r_tg-rf)/(b-2*a*rf+c*rf**2)

weight=lamda*np.dot(np.linalg.inv(covariance),(mean_return-rf*e))

print(weight)

result:

3080

3080

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言