罗纳德·哈里·科斯(Ronald H. Coase),著名经济学家,新制度经济学鼻祖。科斯因发现并阐明了交易成本和产权在经济组织和制度结构中的重要性及其在经济活动中的作用而获得1991年诺贝尔经济学奖。科斯在其1937年发表的文章《企业的性质》一文中,首次创造性地提出了“交易费用”的概念,并以此来解释企业存在的原因以及企业扩展的边界问题。该篇文章也成为新制度经济学的开山之作。笔者打算通过几篇博文的内容来对《企业的性质》进行详细解读,本文是系列中的最后一篇。

IV

It would seem important to examine one further point and that is to consider the relevance of this discussion to the general question of the "cost-curve of the firm."

It has sometimes been assumed that a firm is limited in size under perfect competition if its cost curve slopes upward,43 while under imperfect competition, it is limited in size because it will not pay to produce more than the output at which marginal cost is equal to marginal revenue.« But it is clear that a firm may produce more than one product and, therefore, there appears to be no prima facie reason why this upward slope of the cost curve in the case of perfect competition or the fact that marginal cost will not always be below marginal revenue in the case of imperfect competition should limit the size of the firm.45 Mrs. Robinson46 makes the simplifying assumption that only one product is being produced. But it is clearly important to investigate how the number of products produced by a firm is determined, while no theory which assumes that only one product is in fact produced can have very great practical significance.

【译文】

①进一步说明这一点看来是重要的,那就是上述讨论与“企业成本曲线”的一般问题的相关性。②人们有时假定,如果企业的成本曲线向上倾斜,在完全竞争条件下,企业在规模上会受到限制;而在不完全竞争条件下,企业在规模上受到限制是因为当边际成本等于边际收益时,企业不愿意付出大于产出的生产代价。③但显然企业可以生产一种以上的产品,所以,没有显而易见的原因说明为什么在完全竞争的情况下成本曲线向上倾斜和在不完全竞争的情况下,边际成本通常不低于边际收益的事实会限制企业的规模。④罗宾逊夫人作出了仅生产一种产品的简单假定,但研究企业生产的产品种数是如何决定的,显然是重要的,同时,没有一种假定实际上只生产一种产品的理论会有非常大的实际意义。

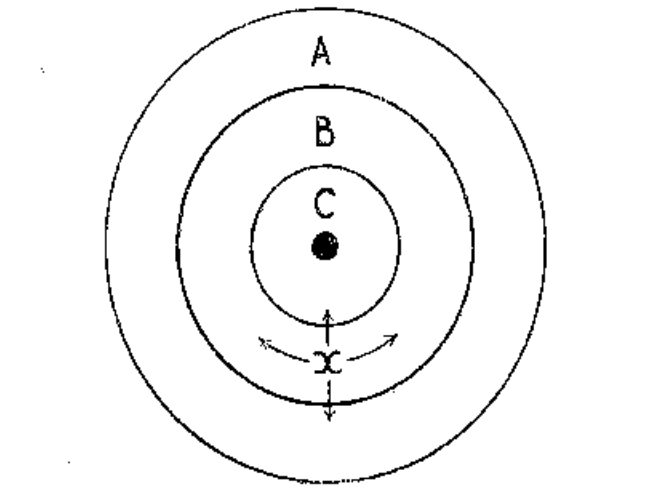

It might be replied that under perfect competition, since everything that is produced can be sold at the prevailing price, then there is no need for any other product to be produced. But this argument ignores the fact that there may be a point where it is less costly to organize the exchange transactions of a new product than to organize further exchange transactions of the old product. This point can be illustrated in the following way. Imagine, following von Thunen, that there is a town, the consuming center, and that industries are located around this central point in rings. These conditions are illustrated in the following diagram in which A, B, and C represent different industries.

Imagine an entrepreneur who starts controlling exchange transactions from x. Now as he extends his activities in the same product (B), the cost of organizing increases until at some point it becomes equal to that of a dissimilar product which is nearer. As the firm expands, it will therefore from this point include more than one product (A and C). This treatment of the problem is obviously incomplete,47 but it is necessary to show that merely proving that the cost curve turns upwards does not give a limitation to the size of the firm. So far we have only considered the case of perfect competition; the case of imperfect competition would appear to be obvious.

【译文】

⑤有人或许会说,在完全竞争条件下,既然生产的每一种产品都能按照通行的价格出售,那么就没必要生产任何其他产品了。但这一说法忽视了这样的事实,那就是可能存在这一情况:组织一种新产品的交易较之继续组织老产品的交易成本要低。⑥这一点可以用下面的方法加以说明。根据⑦冯•屠能的思路,设想有一个小镇,是消费中心,还有一些产业分布在这个中心的周围。这些情况可用下图说明,其中A,B,C表示不同的产业。设想一个企业家从X开始控制交易。现在,当他在同一种产品(B)上扩大其生产经营活动时,组织成本会增加,直到它等于邻近的其他产品的组织成本为止。随着企业的扩张,企业生产由此将从一种产品发展到多种产品(A和C)。⑧这样处理问题显然是不全面的,但对于表明仅仅论证成本曲线倾向于向上不能得出企业规模会受到限制的结论,则是必要的。至此,我们只考察了完全竞争的情况,而不完全竞争的情况似乎是显而易见的。

To determine the size of the firm, we have to consider the marketing costs (that is, the costs of using the price mechanism), and the costs of organizing the different entrepreneurs and then we can determine how many products will be produced by each firm and how much of each it will produce. It would, therefore, appear that Mr. Shove48 in his article on "Imperfect Competition" was asking questions which Mrs. Robinson's cost curve apparatus cannot answer; The factors mentioned above would seem to be the relevant ones.

【译文】

⑨为了确定企业的规模,我们不得不考虑市场成本(即使用价格机制的成本)和不同企业家的组织成本,而后我们才能确定每一个企业生产多少种产品和每一种产品生产多少。因此,⑩肖夫先生在他的关于“不完全竞争”的论义中显然提出了罗宾逊夫人的成本曲线理论所不能回答的问题。上面提到的因素似乎是与此相关的。

【注解】12:

①科斯为了证明企业的性质是因为价格机制被取代这一特性决定的,所以,在这里继续讨论和研究。

②科斯利用企业成本曲线概念继续论证他本人的观点,他认为,假设在完全竞争条件下,企业规模扩张是与企业成本曲线发生关系的,这种关系表现为企业的成本曲线向上倾斜(企业成本加大),企业规模扩张受到限制;假设在不完全竞争条件下,企业规模扩张与企业成本曲线没有关系的,而与边际成本和边际收益这两个变量发生关系,企业边际成本大于边际收益企业规模扩张就可能停止了。

③科斯认为上述情况是在企业生产一种产品条件下出现的情况,那么,如果企业不是生产一种产品,而是生产一种以上产品时,成本曲线关系和边际成本与边际效益关系并不是限制企业扩张的因素。

④科斯强调了只是研究企业生产一种产品是没有任何实际意义的,因为任何企业都不可能只是单一的生产一种产品的。

⑤科斯从另一个方面论证自己的观点,有人说在完全竞争(自由竞争)条件下,企业只生产一种产品就可以完全销售出去,何必再去生产更多的产品,科斯对这种说法进行了反驳,他继续陈述了这样一个事实:“组织一种新产品的交易较之继续组织老产品的交易成本要低。”这正是驱动企业生产更多产品的直接原因。

⑥在论证价格机制被取代是因为企业内部交易成本低于市场交易成本的原因造成的,科斯进一步研究如果企业开发新产品并投入生产时的交易成本低于继续生产老产品的交易成本是否成立。

科斯使用了企业边际概念来解释这个问题,科斯根据冯•屠能的思路,设计了一个产业圈,在这个产业圈中有A,B,C三个产业,其中企业X是在产业B上组织生产,与此同时企业X继续扩大企业规模,这将导致企业X的组织成本加大,那么,企业规模扩张到什么时候截止呢?只有企业成本加大到与A,C两个产业内企业成本相等时,企业扩张停止。

科斯在这里要说明的问题是:第一,企业规模扩张是由边际的;第二,企业规模扩张是有限制的;第三,企业规模扩受到限制的原因是企业内部的交易成本大小;交易成本越高,企业规模扩张就越慢,受到限制就越大,交易成本越低,企业规模扩张就越快,受到限制就越小;第四,企业规模扩张停止,只有企业的交易成本与其他企业交易成本相等的情况下,企业扩张就停止了。

⑦冯•屠能:约翰·海因利希·冯·屠能(Johann Heinrich von Thünen,1783—1850)是德国著名农业经济学家,也是边际学派的先驱者。在其《在农业和国民经济方面的孤立国家》有的称为《孤立国》(1826)著作中,详细地论述了农地与城市中心市场的距离与土地利用的关系和土地的位置对其利用的影响。依据他的经济区位理论,距经济中心的距离越远,则经济价值就越小,经济比较优势就越小。他的观点被后来的人们称作“屠能圈(Thünen Kreise)”。

⑧科斯认为这样的分析还是不全面的,这种分析只能说明利用“企业成本曲线”变动解释企业规模扩张受到限制是十分必要的。

⑨科斯在上述讨论的基础上,引申出了利用市场成本和企业成本之间的关系,来分析企业规模扩张的问题。

【评注】

Part 4:企业与市场交易成本的差异

- 第四部分主要是为搞清楚前面的分析与企业成本曲线一般问题的相关性。科斯认为,“要决定企业规模,必须考虑利用价格机制的成本和组织各个企业家的成本。之后才能决定每个企业生产产品的种类和每种产品的生产数量”。

- 企业交易成本小于市场交易成本,增加产品的数量和品种

- 企业交易成本大于市场交易成本,减少产品的数量和品种

- 企业交易成本等于市场交易成本,保持原有的数量和品种

V

Only one task now remains; and that is, to see whether the concept of a firm which has been developed fits in with that existing in the real world. We can best approach the question of what constitutes a firm in practice by considering the legal relationship normally called that of "master and servant" or "employer and employee."49 The essentials of this relationship have been given as follows:

“(1) the servant must be under the duty of rendering personal services to the master or to others on behalf of the master, otherwise the contract is a con-tract for sale of goods or the like.

(2) The master must have the right to control the servant's work, either personally or by another servant or agent. It is this right of control or interference, of being entitled to tell the servant when to work (within the hours of service) and when not to work, and what work to do and how to do it (within the terms of such service) which is the dominant characteristic in this relation and marks off the servant from an independent contractor, or from one employed merely to give to his employer the fruits of his labour. In the latter case, the contractor or performer is not under the employer's control in doing the work or effecting the service; he has to shape and manage his work 50 as to give the result he has contracted to effect.”50

【译文】

①现在唯一剩下的问题是,看一看已经发展起来的企业概念是不是与现实世界中的情况相一致。②通过考虑通常被称为“主人与仆人”或“雇主与雇员”的法律关系,我们能很好地研究现实中企业的构成问题。这种关系的实质列举如下:

“(1)仆人必须向主人或主人的其他代理人承担提供个人劳务的义务,而契约就是有关物品或类似物品的出售的契约。

(2)主人必须有权亲自或者通过另一个仆人或代理人控制仆人的工作。有权告诉仆人何时工作(在服务时间内)和何时不工作,以及做什么工作和如何去做(在服务范围内),这种控制和干预的权利就是这种关系的性质特征,它从独立的缔约人或从仅向其雇主提供其劳动成果的雇员中区分出了仆人。在后一种情形中,缔约人或执行人不是在雇主的控制下做工作和提供劳务,而是他必须计划和设法完成他的工作,以便实现他答应提供的结果。”

We thus see that it is the fact of direction which is the essence of the legal concept of "employer and employee," just as it was in the economic concept which was developed above. It is interesting to note that Professor Batt says further:

“That which distinguishes an agent from a servant is not the absence or presence of a fixed wage or the payment only of commission on business done, but rather the freedom with which an agent may carry out his employment.”51

We can therefore conclude that the definition we have given is one which approximates closely to the firm as it is considered in the real world.

Our definition is, therefore, realistic. Is it manageable? This ought to be clear; When we are considering how large a firm will be the principle of marginalism works smoothly. The question always is, will it pay to bring an extra exchange transaction under the organizing authority? At the margin, the costs of organizing within the firm will be equal either to the costs of organizing in another firm or to the costs involved in leaving the transaction to be "organized" by the price mechanism. Business men will be constantly experimenting, controlling more or less, and in this way, equilibrium will be maintained. This gives the position of equilibrium for static analysis. But it is clear that the dynamic factors are also of considerable importance, and an investigation of the effect changes have on the cost of organizing within the firm and on marketing costs generally will enable one to explain why firms get larger and smaller; We thus have a theory of moving equilibrium. The above analysis would also appear to have clarified the relationship between initiative or enterprise and management. Initiative means forecasting and operates through the price mechanism by the making of new contracts. Management proper merely reacts to price changes, rearranging the factors of production under its control. That the business man normally combines both functions is an obvious result of the marketing costs which were discussed above. Finally, this analysis enables us to state more exactly what is meant by the "marginal product" of the entrepreneur. But an elaboration of this point would take us far from our comparatively simple task of definition and clarification.

【译文】

③由此可见,指挥是“雇主与雇员”这种法律关系的实质,这正是上文所提出的经济概念。巴特教授的话是值得注意的

“代理人与仆人的区别并不是存在或不存在固定工资或由企业专门委员会决定的报酬,而是代理人有就业的自由。”

④由此我们可以得出结论,我们给出的定义与现实世界中的企业是非常接近的。因此,我们的定义是现实的。⑤那么,我们的定义能应用吗?答案显然是肯定的。⑥当我们考虑企业应多大时,边际原理就会顺利地发挥作用。⑦这个问题始终是,在组织权威下增加额外交易要付出代价吗?在边际点上,在企业内部组织交易的成本或是等于在另一个企业中的组织成本,或是等于由价格机制“组织”这笔交易所包含的成本。实业家们不断地进行实验,多控制一点或少控制一点交易,用这个办法来维持均衡。这就为静态分析提供了均衡状态。⑧但显然,动态因素也是相当重要的。一般只有对引起企业内部组织成本和市场成本的变化作了调查,才能说明企业规模为什么扩大或缩小。我们因此有了滚动均衡理论。⑨上面的分析也似乎澄清了经营和管理之间的关系。经营意味着预测和通过签订新的契约、利用价格机制进行操作。管理则恰恰意味着仅仅对价格变化作出反应,并在其控制下重新安排生产要素。实业家们通常具有这两种功能是上面所讨论的市场成本的明显结果。⑩最后,这样的分析就使我们更准确地叙述企业家的“边际产品”的含义。但对这一点的详细描述会使我们远远超出相形之下较为简单的定义和分类的任务。

【注解】13:

①科斯对企业性质的研究按照罗宾逊夫人关于“假设”的两个条件,其一,这种假设是否容易解释;其二,这种假设是否与现实世界相符。科斯在基本完成了“假设”条件中的第一个条件基础上,继续论述符合“假设”条件中的第二个条件,即,这种假设是否与现实世界吻合。

②在这里我们看看关于企业的性质课题科斯是怎样解释的:

第一,企业组织中雇主与雇员之间的法律关系是企业性质在现实世界中具体体现;

第二,企业组织中雇主与雇员之间的法律关系是依靠契约固定下来的;

第三,这种契约明确了雇主与雇员之间的权利和义务,雇主依靠他的权利支配和指挥雇员,雇员则依靠他的义务服从雇主的控制和支配;

③透过雇主与雇员之间的法律关系,科斯看出它们的实质就是指挥,(当然也包括组织、协调和控制),那么,指挥不属于法律范畴而是经济范畴。

④进而科斯得出了结论:关于企业的性质的论证是与现实世界相吻合的。

⑤科斯继续论证关于企业性质的结论在现实世界中是否能使用,其答案是肯定的:

⑥利用这个结论在解释企业规模扩大时,企业边际原理就会发挥作用

⑦利用这个结论在企业与企业家们可以有效地控制企业内部的成本,维持成本与效益之间的静态平衡。

⑧利用这个结论企业在动态状况下,企业内部交易成本与市场交易成本经过比较,决定企业规模是否扩大或缩小,进而形成了滚动均衡理论。

⑨利用这个结论可以解释企业的经营与管理之间的关系,即:“经营意味着预测和通过签订新的契约、利用价格机制进行操作。管理则恰恰意味着仅仅对价格变化作出反应,并在其控制下重新安排生产要素。”

⑩利用这个结论可以“使我们更准确地叙述企业家的“边际产品”的含义。”

【评注】

Part 5:考察理论在现实中的解释力

- 此部分主要说明了论文中给出的企业概念与真实存在的企业的一致性。

- 科斯说:“我们给出的企业定义与现实中的企业定义十分相近。而且,这个定义当然可行。当思考企业的规

模应该多大时,边际原理就会很好地发挥作用……在边际上,企业内部组织交易的成本,或者与另一企业组

织此交易成本相等,或者与价格机制组织此交易的成本相等……一般来说,只有研究企业内部组织成本和市

场交易成本变化的影响,才能解释企业扩大或缩小的原因。因此我们获得了移动均衡理论”。

(全文完)

1413

1413

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言