写在前面:

1. 本文中提到的“K线形态查看工具”的具体使用操作请查看该博文;

2. K线形体所处背景,诸如处在上升趋势、下降趋势、盘整等,背景内容在K线形态策略代码中没有体现;

3. 文中知识内容来自书籍《K线技术分析》by邱立波。

目录

解说

长十字线是上下影线都很长的同价位线。至于影线多长才算是长十字线,市场上没有一个统一的标准,交易者凭感觉很容易就能区分。

出现长十字线是转势信号。上影线越长,表示卖盘越重;下影线越长,表明买盘越强。

长十字线的收盘价和开盘价相同,表明多空双方最终握手言和,谁也没能以绝对优势压倒对方。但长长的上下影线告诉交易者,平静的开盘和收盘之间曾经经历了一场极其残酷的拉锯战,双方的阵地都曾经易手,甚至有可能数度出现攻防互换。无论是战争还是交易,平衡从来都是短暂的,僵局马上就会打破。谁会取得最终的胜利呢?在此之前,如果其中一方一直在乘胜追击,那么现在突然遭遇如此激烈的抵抗,很显然多空双方的力量对比正在发生变化。因此,长十字线出现在高价位或低价位区域,常常意味着趋势即将出现反转。

技术特征

1)开盘价和收盘价相同。

2)上下影线很长。

3)上涨和下跌过程中都会出现。

技术含义

1)在股价已有较大涨幅后出现,为见顶信号。

2)在股价有较大跌幅后出现长十字线为见底信号。

3)在上涨途中出现长十字线,继续看涨。持仓不动。

4)在下跌途中出现长十字线,继续看跌。持币观望。

K线形态策略代码

def excute_strategy(daily_file_path):

'''

名称:长十字线

识别:上下影线都很长, 同价位

自定义:

1. 影线很长=》超过上一交易日价格2%;

前置条件:计算时间区间 2021-01-01 到 2022-01-01

:param daily_file_path: 股票日数据文件路径

:return:

'''

import pandas as pd

import os

start_date_str = '2021-01-01'

end_date_str = '2022-01-01'

df = pd.read_csv(daily_file_path,encoding='utf-8')

# 删除停牌的数据

df = df.loc[df['openPrice'] > 0].copy()

df['o_date'] = df['tradeDate']

df['o_date'] = pd.to_datetime(df['o_date'])

df = df.loc[(df['o_date'] >= start_date_str) & (df['o_date']<=end_date_str)].copy()

# 保存未复权收盘价数据

df['close'] = df['closePrice']

# 计算前复权数据

df['openPrice'] = df['openPrice'] * df['accumAdjFactor']

df['closePrice'] = df['closePrice'] * df['accumAdjFactor']

df['highestPrice'] = df['highestPrice'] * df['accumAdjFactor']

df['lowestPrice'] = df['lowestPrice'] * df['accumAdjFactor']

# 开始计算

df.loc[df['closePrice']>=df['openPrice'],'type'] = 1

df.loc[df['closePrice']<df['openPrice'],'type'] = -1

df['body_length'] = abs(df['closePrice'] - df['openPrice'])

df.loc[df['type']==1,'top_shadow_length'] = df['highestPrice'] - df['closePrice']

df.loc[df['type']==-1,'top_shadow_length'] = df['highestPrice'] - df['openPrice']

df.loc[df['type']==1,'bottom_shadow_length'] = df['openPrice'] - df['lowestPrice']

df.loc[df['type']==-1,'bottom_shadow_length'] = df['closePrice'] - df['lowestPrice']

df['signal'] = 0

df['signal_name'] = ''

long_len = 0.02

df.loc[(df['body_length']==0) & (df['top_shadow_length']/df['closePrice'].shift(1)>=long_len) & (df['bottom_shadow_length']/df['closePrice'].shift(1)>=long_len),'signal'] = 1

df.loc[(df['body_length']==0) & (df['top_shadow_length']/df['closePrice'].shift(1)>=long_len) & (df['bottom_shadow_length']/df['closePrice'].shift(1)>=long_len),'ext_0'] = (df['top_shadow_length']/df['closePrice'].shift(1))*100

df.loc[(df['body_length']==0) & (df['top_shadow_length']/df['closePrice'].shift(1)>=long_len) & (df['bottom_shadow_length']/df['closePrice'].shift(1)>=long_len),'ext_1'] = (df['bottom_shadow_length']/df['closePrice'].shift(1))*100

df = df.round({'ext_0':5,'ext_1':5})

df['signal_name'] = df['ext_0'].astype('str') + ';' + df['ext_1'].astype('str')

file_name = os.path.basename(daily_file_path)

title_str = file_name.split('.')[0]

line_data = {

'title_str':title_str,

'whole_header':['日期','收','开','高','低'],

'whole_df':df,

'whole_pd_header':['tradeDate','closePrice','openPrice','highestPrice','lowestPrice'],

'start_date_str':start_date_str,

'end_date_str':end_date_str,

'signal_type':'line'

}

return line_data

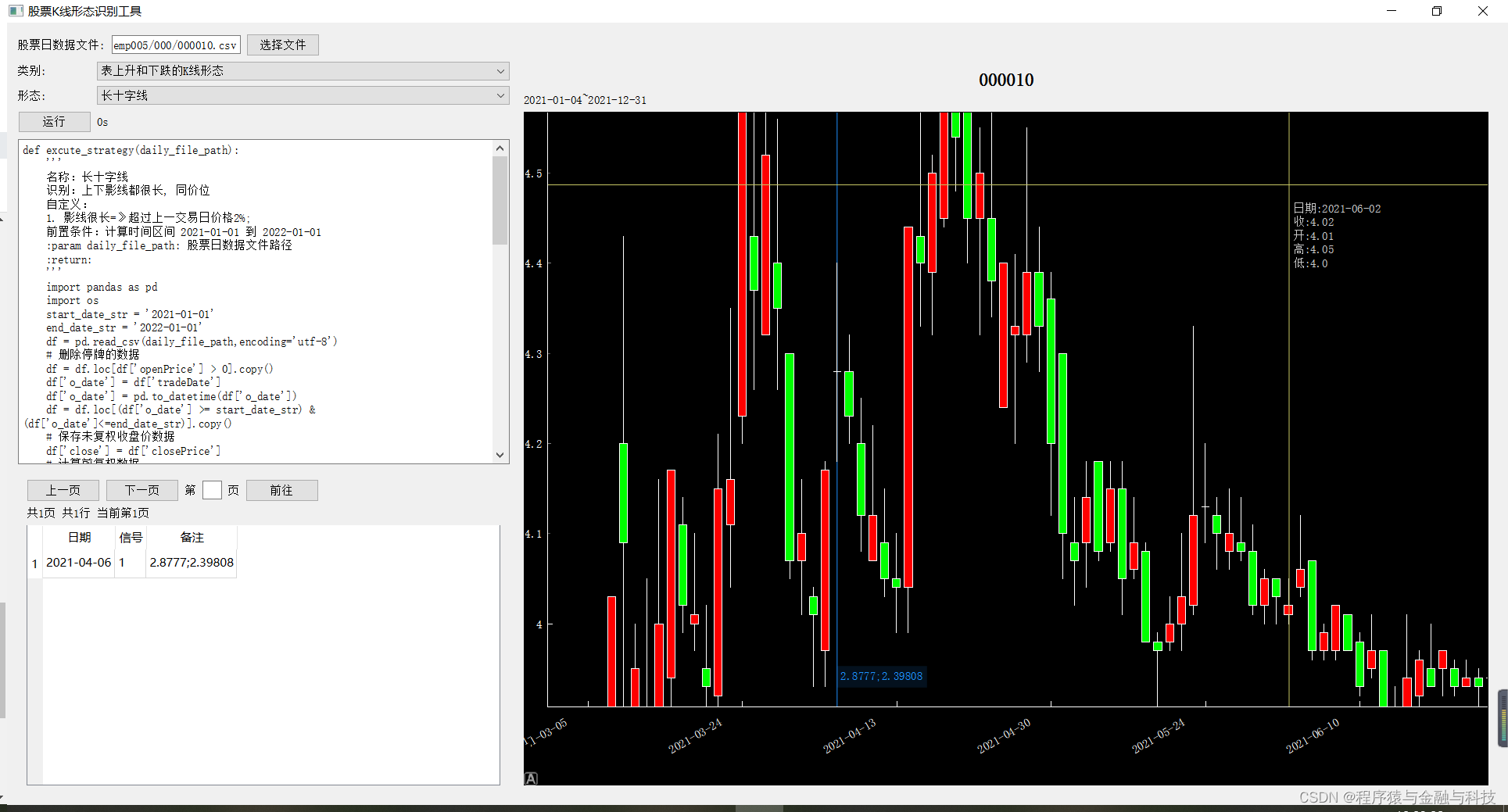

结果

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言