《A Practical Guide To Quantitative Finance Interviews》,被称为量化绿皮书,是经典的量化求职刷题书籍之一,包含以下七章:

Chapter 1 General Principles 通用技巧

Chapter 2 Brain Teasers 脑筋急转弯

Chapter 3 Calculus and Linear Algebra 微积分与线性代数

Chapter 4 Probability Theory 概率论

Chapter 5 Stochastic Process and Stochastic Calculus 随机过程与随机微积分

Chapter 6 Finance 金融

Chapter 7 Algorithms and Numerical Methods 算法与数值方法

目录

文章目录

6.2 The Greeks 希腊字母

Delta: Δ = ∂ f ∂ S \Delta=\frac{\partial f}{\partial S} Δ=∂S∂f

Gamma: Γ = ∂ 2 f ∂ S 2 \Gamma=\frac{\partial^2 f}{\partial S^2} Γ=∂S2∂2f

Theta: Θ = ∂ f ∂ t \Theta=\frac{\partial f}{\partial t} Θ=∂t∂f

Vega: v = ∂ f ∂ σ v=\frac{\partial f}{\partial \sigma} v=∂σ∂f

Rho: ρ = ∂ f ∂ r \rho=\frac{\partial f}{\partial r} ρ=∂r∂f

6.2.1 Delta: Δ = ∂ f ∂ S \Delta=\frac{\partial f}{\partial S} Δ=∂S∂f

对于具有股息收益率 y y y的欧式看涨期权: Δ = e − y τ N ( d 1 ) \Delta=e^{-y\tau}N(d_1) Δ=e−yτN(d1)

对于具有股息收益率 y y y的欧式看跌期权: Δ = − e − y τ [ 1 − N ( d 1 ) ] \Delta=-e^{-y\tau}[1-N(d_1)] Δ=−e−yτ[1−N(d1)]

A. 非派息股票的欧式看涨期权的delta是多少?如何推导?

A. What is the delta of a European call option on a non-dividend paying stock? How do you derive the delta?

答案: Δ = N ( d 1 ) \Delta=N(d_1) Δ=N(d1)

c = S N ( d 1 ) − K e − r τ N ( d 2 ) , d 1 = l n ( S / K ) + ( r + σ 2 / 2 ) τ σ τ , d 2 = d 1 − σ τ c=S N(d_1) - Ke^{-r\tau} N(d_2),d_1=\frac{ln(S/K)+(r+\sigma^2/2)\tau}{\sigma\sqrt{\tau}},d_2=d_1-\sigma\sqrt{\tau} c=SN(d1)−Ke−rτN(d2),d1=στln(S/K)+(r+σ2/2)τ,d2=d1−στ

∂ c ∂ S = N ( d 1 ) + S × ∂ ∂ S N ( d 1 ) − K e − r τ × ∂ ∂ S N ( d 2 ) \frac{\partial c}{\partial S}=N(d_1)+S\times\frac{\partial}{\partial S}N(d_1)-Ke^{-r\tau}\times\frac{\partial}{\partial S}N(d_2) ∂S∂c=N(d1)+S×∂S∂N(d1)−Ke−rτ×∂S∂N(d2)

- ∂ ∂ S N ( d 1 ) = N ′ ( d 1 ) ∂ ∂ S d 1 = 1 2 π e − d 1 2 / 2 × 1 S σ τ = 1 S σ 2 π τ e − d 1 2 / 2 \frac{\partial}{\partial S}N(d_1)=N'(d_1)\frac{\partial}{\partial S}d_1=\frac{1}{\sqrt{2\pi}}e^{-d_1^2/2}\times\frac{1}{S\sigma\sqrt{\tau}}=\frac{1}{S\sigma\sqrt{2\pi\tau}}e^{-d_1^2/2} ∂S∂N(d1)=N′(d1)∂S∂d1=2π1e−d12/2×Sστ1=Sσ2πτ1e−d12/2

- ∂ ∂ S N ( d 2 ) = N ′ ( d 2 ) ∂ ∂ S d 2 = 1 2 π e − d 2 2 / 2 × 1 S σ τ = 1 S σ 2 π τ e − ( d 1 − σ τ ) 2 / 2 = 1 S σ 2 π τ e − d 1 2 / 2 e σ τ d 1 e − σ 2 τ / 2 \frac{\partial}{\partial S}N(d_2)=N'(d_2)\frac{\partial}{\partial S}d_2=\frac{1}{\sqrt{2\pi}}e^{-d_2^2/2}\times\frac{1}{S\sigma\sqrt{\tau}}=\frac{1}{S\sigma\sqrt{2\pi\tau}}e^{-(d_1-\sigma\sqrt{\tau})^2/2}=\frac{1}{S\sigma\sqrt{2\pi\tau}}e^{-d_1^2/2}e^{\sigma\sqrt{\tau}d_1}e^{-\sigma^2\tau/2} ∂S∂N(d2)=N′(d2)∂S∂d2=2π1e−d22/2×Sστ1=Sσ2πτ1e−(d1−στ)2/2=Sσ2πτ1e−d12/2eστd1e−σ2τ/2

- d 1 = l n ( S / K ) + ( r + σ 2 / 2 ) τ σ τ ⇒ σ τ d 1 − σ 2 τ / 2 = ln ( S / K ) + r τ d_1=\frac{ln(S/K)+(r+\sigma^2/2)\tau}{\sigma\sqrt{\tau}}\Rightarrow \sigma\sqrt{\tau}d_1-\sigma^2\tau/2=\ln(S/K)+r\tau d1=στln(S/K)+(r+σ2/2)τ⇒στd1−σ2τ/2=ln(S/K)+rτ

- ∂ ∂ S N ( d 2 ) = S K e r τ ∂ ∂ S N ( d 1 ) ⇒ S × ∂ ∂ S N ( d 1 ) − K e − r τ × ∂ ∂ S N ( d 2 ) = 0 \frac{\partial}{\partial S}N(d_2)=\frac{S}{K}e^{r\tau}\frac{\partial}{\partial S}N(d_1)\Rightarrow S\times\frac{\partial}{\partial S}N(d_1)-Ke^{-r\tau}\times\frac{\partial}{\partial S}N(d_2)=0 ∂S∂N(d2)=KSerτ∂S∂N(d1)⇒S×∂S∂N(d1)−Ke−rτ×∂S∂N(d2)=0

∂ c ∂ S = N ( d 1 ) \frac{\partial c}{\partial S}=N(d_1) ∂S∂c=N(d1)

B. 你估计非派息股票的平值看涨期权的delta是多少?当平值期权接近到期日时delta会发生什么??

B. What is your estimate of the delta of an at-the-money call on a stock without dividend? What will happen to delta as the at-the-money option approaches maturity date?

答案:

平值欧式看涨期权有 S = K ⇒ d 1 = ( r + σ 2 / 2 ) τ σ τ = ( r σ + σ 2 ) τ S=K\Rightarrow d_1=\frac{(r+\sigma^2/2)\tau}{\sigma\sqrt{\tau}}=(\frac{r}{\sigma}+\frac{\sigma}{2})\sqrt{\tau} S=K⇒d1=στ(r+σ2/2)τ=(σr+2σ)τ

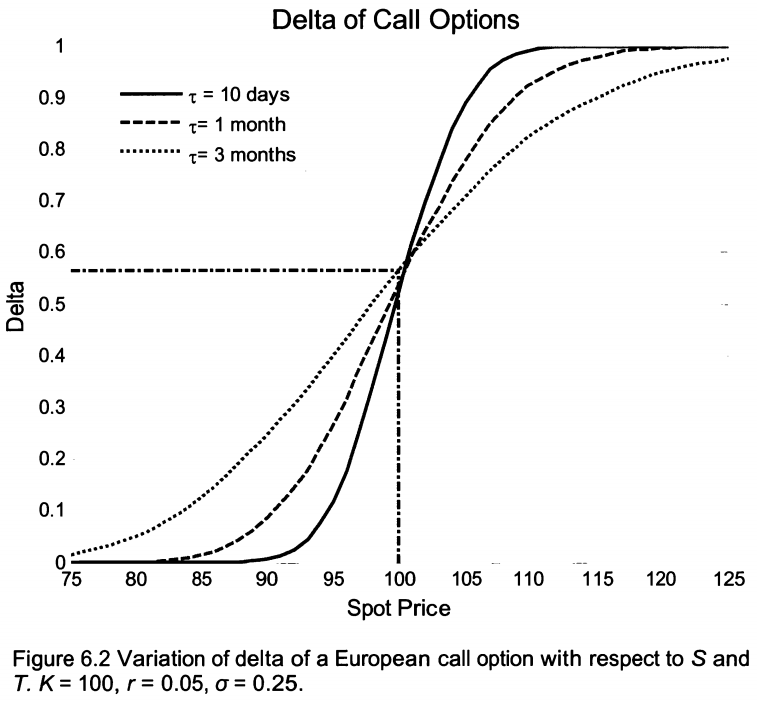

∴ Δ = N ( d 1 ) > 0.5 \therefore \Delta=N(d_1)\gt0.5 ∴Δ=N(d1)>0.5

T − t → 0 , ( r σ + σ 2 ) τ → 0 ⇒ N ( d 1 ) → N ( 0 ) = 0.5 T-t\rightarrow 0,(\frac{r}{\sigma}+\frac{\sigma}{2})\sqrt{\tau}\rightarrow 0\Rightarrow N(d_1)\rightarrow N(0)=0.5 T−t→0,(σr+2σ)τ→0⇒N(d1)→N(0)=0.5

平值欧式看涨期权 Δ > 0.5 \Delta\gt0.5 Δ>0.5,剩余时间越长, D e l t a Delta Delta越大

由图还可知,当 S S S较大时( S > > K S\gt\gt K S>>K), D e l t a → 1 Delta\rightarrow 1 Delta→1,且剩余时间越短,delta越快接近1;当 S S S较小时( S < < K S\lt\lt K S<<K), D e l t a → 0 Delta\rightarrow 0 Delta→0,且剩余时间越短,delta越快接近0。

C. 你刚刚建立了通用汽车股票的欧式看涨期权的多头头寸,并决定动态对冲该头寸,以消除通用汽车股价波动带来的风险。你将如何对冲看涨期权?如果在对冲之后,通用汽车的价格突然上涨,你将如何重新平衡你的对冲头寸?

C. You just entered a long position for a European call option on GM stock and decide to dynamically hedge the position to eliminate the risk from the fluctuation of GM stock price. How will you hedge the call option? If after your hedge, the price of GM has a sudden increase, how will you rebalance your hedging position?

答案:

d 1 = l n ( S / K ) + ( r − y + σ 2 / 2 ) τ σ τ , Δ = e − y τ N ( d 1 ) d_1 =\frac{ln(S/K)+(r-y+\sigma^2/2)\tau}{\sigma\sqrt{\tau}},\Delta=e^{-y\tau}N(d_1) d1=στln(S/K)+(r−y+σ2/2)τ,Δ=e−yτN(d1)

S ↑ ⇒ d 1 ↑ ⇒ Δ ↑ S\uparrow \Rightarrow d_1\uparrow \Rightarrow \Delta\uparrow

最低0.47元/天 解锁文章

最低0.47元/天 解锁文章

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言