机器学习项目实战之信用卡欺诈检测

1、项目介绍

原始数据为银行的个人交易记录,每一条信息代表一次交易,原始数据已经进行了类似PCA的处理,现在已经把特征数据提取好了,检测的目的是通过数据找出那些交易存在潜在的欺诈行为。

2、观察数据

即使是拿到处理好的数据也不要着急建立模型,否则会事倍功半,一定要先观察数据。此处分别用到了Numpy-科学计算库、Pandas-数据分析处理库以及Matplotlib-可视化库,具体的功能相信大家都很熟悉了,这里不再过多的介绍,直接开始正文吧!

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

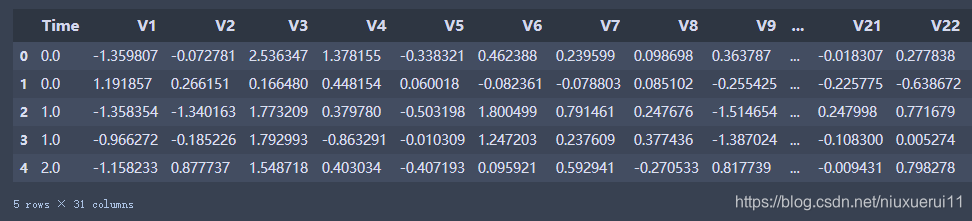

data = pd.read_csv('creditcard.csv')

data.head()

从数据的前五行中可以看出数据已经经过降维处理,这样的数据有好处也有坏处,好处就是我们不需要对数据再进行预处理,坏处就是数据具体代表的含义就不是很清楚了,这个案列中我们不再追究V1,V2….分别代表什么含义。

其中Amount的浮动范围很大,因此在稍后的过程中要进行归一化处理,Class代表分类标签,如果Class为0,代表这条交易是正常的交易,如果Class为1,代表这条交易确实存在欺诈行为。下面以柱状图的形式来对标签分类情况进行观察。

#分别计算不同的属性有多少个

count_Class = pd.value_counts(data['Class'],sort=True).sort_index()

#用柱状图的形式绘画出

count_Class.plot(kind = 'bar')

plt.title("Found class histogram")

plt.xlabel("Class")

plt.ylabel("Frequency")

从图中可以看出标签为0的很多,而标签为1的却很少,说明样本的分布情况是非常不均衡的,所以在构建分类器的时候要特别注意一个误区,即使将结果全部预测为0也会出现很好的分类结果,这是在下文中需要着重考虑的一点。

3、数据处理

3.1. 标准化操作

首先对Amount的值进行标准化处理,从机器学习库Scikit-Learn引入标准化函数即可。

from sklearn.preprocessing import StandardScaler

#StandardScaler作用:去均值和方差归一化。且是针对每一个特征维度来做的,而不是针对样本。

data['normAmount'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1, 1))

#删除Time和Amount所在的列

data = data.drop(['Time','Amount'],axis=1)

data.head()

3.2. 使用下采样解决样本数据不均衡

要解决样本分布不均衡的问题,可以采用Undersample(下采样,即使样本数据变的一样少)和Oversample(过采样,即使样本数据变的一样多)。

下面代码采用下采样,即在class=0的标签中随机选取跟class=1一样多的样本数。

#取出所有属性,不包含class的这一列

X = data.ix[:, data.columns != 'Class']

#取出class这一列

y = data.ix[:, data.columns == 'Class']

#计算出class==1(存在欺诈行为)元素有多少个

number_records_fraud = len(data[data.Class == 1])

#取出class==1的行索引

fraud_indices = np.array(data[data.Class == 1].index)

#取出class==0的行索引

normal_indices = data[data.Class == 0].index

#随机选择和1这个属性样本个数相同的0样本

random_normal_indices = np.random.choice(normal_indices, number_records_fraud, replace = False)

#转换成numpy的格式

random_normal_indices = np.array(random_normal_indices)

#将class=0和1的样本的索引拼接在一起

under_sample_indices = np.concatenate([fraud_indices,random_normal_indices])

#下采样的数据集

under_sample_data = data.iloc[under_sample_indices,:]

#下采样数据集的数据

X_undersample = under_sample_data.ix[:, under_sample_data.columns != 'Class']

#下采样数据集的label

y_undersample = under_sample_data.ix[:, under_sample_data.columns == 'Class']

#打印Class == 0的样本数目

print("Percentage of normal transactions: ", len(under_sample_data[under_sample_data.Class == 0])/len(under_sample_data))

#打印Class == 0的样本数目

print("Percentage of fraud transactions: ", len(under_sample_data[under_sample_data.Class == 1])/len(under_sample_data))

#打印下采样の1总数量

print("Total number of transactions in resampled data: ", len(under_sample_data))

输出结果:

4、训练数据

4.1 用下采样化分池训练集和测试集

疑问? 为什么进行了下采样,还要把原始数据进行切分呢?

这是因为 对数据集的训练是通过下采样的训练集,对数据的测试的是通过原始的数据集的测试集,下采样的测试集可能没有原始部分当中的一些特征,不能充分进行测试。

#用下采样方法分池训练集和测试集

from sklearn.model_selection import train_test_split

#所有数据集

X_train,X_test,y_train,y_test = train_test_split(X,y,test_size=0.3,random_state=0)

print("Number transactions train dataset:",len(X_train))

print("Number transacations test dataset:", len(X_test))

print("total transacations dataset:" ,len(X_train) + len(X_test))

#下采样数据集

X_train_undersample,X_test_undersample,y_train_undersample,y_test_undersample = train_test_split(X_undersample,y_undersample,random_state=0)

print("")

print("Number transacations train dataset:", X_train_undersample)

print("Number transacations test dataset:", X_test_undersample)

print("total transacations dataset:", len(X_train_undersample) + len(X_test_undersample))

输出结果:

4.2 使用逻辑回归模型构建分类器,通过k折交叉验证寻找最优惩罚参数

由于本文数据的特殊性,模型的评估的方法十分钟重要,通常采用的评价指标有准确率、召回率和F值(F-Measure)等。本文采用recall(召回率)作为评估标准。

具体举个例子介绍:假设我们在医院中有1000个病人,其中990个为正样本(正常),10个为负样本(癌症),我们的目的是找出其中的10个负样本,假如我们的模型将多有的1000个病人都预测为正样本,虽然精度有99%,但是并没有找到我们所要的10个负样本,所以这个模型是没用的,因为一个癌症病人都找不出来。而recall是对于想找的东西,找到了多少个,而不是所有样本的精度。

在构造权重参数的时候,为了防止过拟合的现象发生,要引入正则化惩罚项,使这些权重参数处于比较平滑的趋势,具体参数选择在代码中会给出解释。

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import KFold,cross_val_score

from sklearn.metrics import confusion_matrix,recall_score,classification_report

def printing_Kfold_scores(x_train_data,y_train_data):

#k折交叉验证

fold = KFold(n_splits=5,shuffle=False)

#不同的惩罚参数C的参数集,因为不知道哪一种惩罚参数的力度好,通过验证集结果来选择

c_param_range = [0.01,0.1,1,10,100]

#创建一个5行两列的空的DataFrame框,用于存放数据

results_table = pd.DataFrame(index = range(len(c_param_range),2), columns = ['C_parameter','Mean recall score'])

#将'C_parameter'列设置为惩罚参数集中的值

results_table['C_parameter'] = c_param_range

#k折操作将会给出两个列表:train_indices = indices[0], test_indices = indices[1]

j = 0

for c_param in c_param_range:

print('-------------------------------------------')

print('C parameter: ', c_param)

print('-------------------------------------------')

print('')

recall_accs = []

#enumerate() 函数用于将一个可遍历的数据对象(如列表、元组或字符串)组合为一个索引序列,同时列出数据和数据下标,一般用在 for 循环当中。

for iteration,indices in enumerate(fold.split(x_train_data)):

#把c_param_range代入到逻辑回归模型中,并使用了l1正则化

lr = LogisticRegression(C = c_param,penalty = 'l1',solver='liblinear')

#使用indices[0]的数据进行拟合曲线,使用indices[1]的数据进行误差测试

lr.fit(x_train_data.iloc[indices[0],:],y_train_data.iloc[indices[0],:].values.ravel())

#在indices[1]数据上预测值

y_pred_undersample = lr.predict(x_train_data.iloc[indices[1],:].values)

#根据不同的c_parameter计算召回率

recall_acc = recall_score(y_train_data.iloc[indices[1],:].values,y_pred_undersample)

recall_accs .append(recall_acc)

print('Iteration ', iteration,': recall score = ', recall_acc)

#求出我们想要的召回平均值

results_table.loc[j,'Mean recall score'] = np.mean(recall_accs)

j += 1

print('')

print('Mean recall score ', np.mean(recall_accs))

print('')

best_c = results_table.loc[results_table['Mean recall score'].values.argmax()]['C_parameter']

#最后选择最好的 C parameter

print('*********************************************************************************')

print('Best model to choose from cross validation is with C parameter = ', best_c)

print('*********************************************************************************')

return best_c

best_c = printing_Kfold_scores(X_train_undersample,y_train_undersample)

输出结果:

C parameter: 0.01

Iteration 0 : recall score = 0.9625

Iteration 1 : recall score = 0.9012345679012346

Iteration 2 : recall score = 0.9682539682539683

Iteration 3 : recall score = 0.9743589743589743

Iteration 4 : recall score = 0.971830985915493

Mean recall score 0.9556356992859341

C parameter: 0.1

Iteration 0 : recall score = 0.9

Iteration 1 : recall score = 0.8271604938271605

Iteration 2 : recall score = 0.9206349206349206

Iteration 3 : recall score = 0.9487179487179487

Iteration 4 : recall score = 0.9154929577464789

Mean recall score 0.9024012641853018

C parameter: 1

Iteration 0 : recall score = 0.8875

Iteration 1 : recall score = 0.8518518518518519

Iteration 2 : recall score = 0.9365079365079365

Iteration 3 : recall score = 0.9358974358974359

Iteration 4 : recall score = 0.9154929577464789

Mean recall score 0.9054500364007406

C parameter: 10

Iteration 0 : recall score = 0.9

Iteration 1 : recall score = 0.8518518518518519

Iteration 2 : recall score = 0.9523809523809523

Iteration 3 : recall score = 0.9358974358974359

Iteration 4 : recall score = 0.9154929577464789

Mean recall score 0.9111246395753438

C parameter: 100

Iteration 0 : recall score = 0.9

Iteration 1 : recall score = 0.8518518518518519

Iteration 2 : recall score = 0.9523809523809523

Iteration 3 : recall score = 0.9358974358974359

Iteration 4 : recall score = 0.9154929577464789

Mean recall score 0.9111246395753438

Best model to choose from cross validation is with C parameter = 0.01

从输出结果中可以看出最佳的惩罚参数C为0.01

4.3 定义绘制混淆矩阵

def plot_confusion_matrix(cm, classes,title='Confusion matrix',cmap=plt.cm.Blues):

#cm为数据,interpolation='nearest'使用最近邻插值,cmap颜色图谱(colormap), 默认绘制为RGB(A)颜色空间

plt.imshow(cm,interpolation='nearest',cmap=cmap)

plt.title(title)

plt.colorbar()

tick_marks = np.arange(len(classes))

#xticks(刻度下标,刻度标签)

plt.xticks(tick_marks, classes, rotation=0)

plt.yticks(tick_marks, classes)

#text()命令可以在任意的位置添加文字

thresh = cm.max() / 2.

for i, j in itertools.product(range(cm.shape[0]), range(cm.shape[1])):

plt.text(j, i, cm[i, j],

horizontalalignment="center",

color="white" if cm[i, j] > thresh else "black")

#自动紧凑布局

plt.tight_layout()

plt.ylabel('True label')

plt.xlabel('Predicted label')

plt.show()

4.4 使用下采样数据训练,使用下采样数据测试

import itertools

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample = lr.predict(X_test_undersample.values)

#计算混淆矩阵

cnf_matrix = confusion_matrix(y_test_undersample,y_pred_undersample)

#输出精度为小数点后两位

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

#画出非标准化的混淆矩阵

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,classes=class_names,title='Confusion matrix')

plt.show()

输出结果:

4.5 使用下采样数据训练,使用原始数据测试

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred = lr.predict(X_test.values)

#计算混淆矩阵

cnf_matrix = confusion_matrix(y_test,y_pred)

#输出精度为小数点后两位

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

#画出非标准化的混淆矩阵

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,classes=class_names,title='Confusion matrix')

plt.show()

输出结果:

**小结:**虽然recall值可达到91.8%,但是其中有8581个数据本来不存在欺诈行为,却检测成了欺诈行为,这还是一个挺头疼的问题。

如果大家对结果表示怀疑,想着如果用原始数据来训练是否会有更好地效果呢?那么我们不妨用原始数据训练一次试试,代码前面已经写了,只需调用即可。

best_c = printing_Kfold_scores(X_train,y_train)

输出结果:

C parameter: 0.01

Iteration 0 : recall score = 0.4925373134328358

Iteration 1 : recall score = 0.6027397260273972

Iteration 2 : recall score = 0.6833333333333333

Iteration 3 : recall score = 0.5692307692307692

Iteration 4 : recall score = 0.45

Mean recall score 0.5595682284048672

C parameter: 0.1

Iteration 0 : recall score = 0.5671641791044776

Iteration 1 : recall score = 0.6164383561643836

Iteration 2 : recall score = 0.6833333333333333

Iteration 3 : recall score = 0.5846153846153846

Iteration 4 : recall score = 0.525

Mean recall score 0.5953102506435158

C parameter: 1

Iteration 0 : recall score = 0.5522388059701493

Iteration 1 : recall score = 0.6164383561643836

Iteration 2 : recall score = 0.7166666666666667

Iteration 3 : recall score = 0.6153846153846154

Iteration 4 : recall score = 0.5625

Mean recall score 0.612645688837163

C parameter: 10

Iteration 0 : recall score = 0.5522388059701493

Iteration 1 : recall score = 0.6164383561643836

Iteration 2 : recall score = 0.7333333333333333

Iteration 3 : recall score = 0.6153846153846154

Iteration 4 : recall score = 0.575

Mean recall score 0.6184790221704963

C parameter: 100

Iteration 0 : recall score = 0.5522388059701493

Iteration 1 : recall score = 0.6164383561643836

Iteration 2 : recall score = 0.7333333333333333

Iteration 3 : recall score = 0.6153846153846154

Iteration 4 : recall score = 0.575

Mean recall score 0.6184790221704963

Best model to choose from cross validation is with C parameter = 10.0

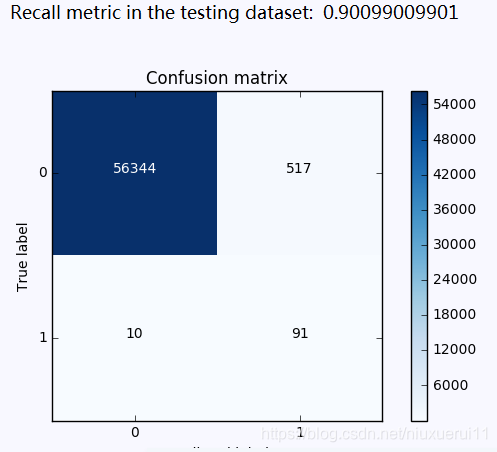

4.6 使用原始数据进行训练与测试

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(X_train,y_train.values.ravel())

y_pred = lr.predict(X_test.values)

#计算混淆矩阵

cnf_matrix = confusion_matrix(y_test,y_pred)

#输出精度为小数点后两位

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

#画出非标准化的混淆矩阵

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,classes=class_names,title='Confusion matrix')

plt.show()

输出结果:

从图中可以看出虽然对正常样本的检测效果很好,但是在欺诈样本中的检测确实很不理想,这个分类器的精度是比较高的,但是它的recall值确实比较低的。

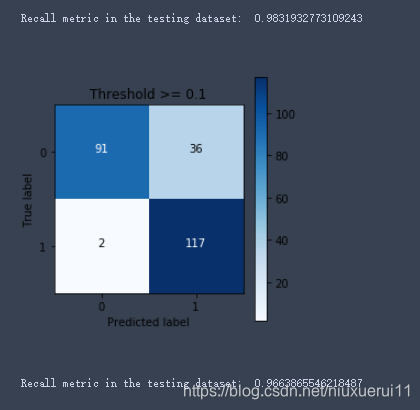

4.7 使用下采样数据训练与测试(不同的阈值对结果的影响)

一般来说逻辑回归的sigmoid函数中,一般来说阈值为0.5,但是也可以自定义不同的阈值,看其是否对最终的结果有影响。

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(X_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample_proba = lr.predict_proba(X_test_undersample.values)

thresholds = [0.1,0.2,0.3,0.4,0.5,0.6,0.7,0.8,0.9]

plt.figure(figsize=(10,10))

j = 1

for i in thresholds:

y_test_predictions_high_recall = y_pred_undersample_proba[:,1] > i

plt.subplot(3,3,j)

j += 1

#计算混淆矩阵

cnf_matrix = confusion_matrix(y_test_undersample,y_test_predictions_high_recall)

#输出精度为小数点后两位

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

#画出非标准化的混淆矩阵

class_names = [0,1]

plot_confusion_matrix(cnf_matrix,classes=class_names,title='Threshold >= %s'%i)

输出结果:

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 0.986394557823

Recall metric in the testing dataset: 0.931972789116

Recall metric in the testing dataset: 0.884353741497

Recall metric in the testing dataset: 0.836734693878

Recall metric in the testing dataset: 0.748299319728

Recall metric in the testing dataset: 0.571428571429

**小结:**从以上的实验可以看出,虽然在阈值设置较小的时候,recall值可以达到1,但是此时模型的精度却太低,此模型就有一种宁可错杀一千,也不可放过一百的感觉。。。当阈值变大时,模型的精度会逐渐上升,recall值稍稍减少,但阈值过大时,模型的精度也会适当减少,而阈值这回大大减小。

4.8使用过采样,使得两种样本数据一样多

在使用过采样之前,首先介绍下SMOTE算法,其基本原理为:

1、对于少数类中的每一个样本x,以欧式距离计算它到少数类样本集中所有样本的距离,得到其k近邻

2、根据样本不平衡比例设置一个采样比例以确定采样倍率N,对于每一个少类样本x,从其k近邻中随机选择若干个样本,假设选择的近邻为xn

3、对于每一个随机选出的近邻xn,分别与原样本按照如下的公式构建新的样本。

构造过采样的数据

import pandas as pd

from imblearn.over_sampling import SMOTE

from sklearn.ensemble import RandomForestClassifier

from sklearn.metrics import confusion_matrix

from sklearn.model_selection import train_test_split

credit_cards=pd.read_csv('creditcard.csv')

columns=credit_cards.columns

# 为了获得特征列,移除最后一列标签列

features_columns=columns.delete(len(columns)-1)

features = credit_cards[features_columns]

labels=credit_cards['Class']

features_train, features_test, labels_train, labels_test = train_test_split(features, labels, test_size=0.2, random_state=0)

oversampler = SMOTE(random_state=0)

os_features,os_labels = oversampler.fit_sample(features_train,labels_train)

print('过采样后,1的样本的个数为:',len(os_labels[os_labels==1]))

输出结果:

过采样后1的样本个数为: 227454

4.9 K折交叉验证得到最好的惩罚参数C

os_features = pd.DataFrame(os_features)

os_labels = pd.DataFrame(os_labels)

best_c = printing_Kfold_scores(os_features,os_labels)

输出结果:

C parameter: 0.01

Iteration 0 : recall score = 0.8903225806451613

Iteration 1 : recall score = 0.8947368421052632

Iteration 2 : recall score = 0.9688834790306518

Iteration 3 : recall score = 0.9578593332673855

Iteration 4 : recall score = 0.9585078203141315

Mean recall score 0.9340620110725185

C parameter: 0.1

Iteration 0 : recall score = 0.8903225806451613

Iteration 1 : recall score = 0.8947368421052632

Iteration 2 : recall score = 0.9704105344694036

Iteration 3 : recall score = 0.9597718204899924

Iteration 4 : recall score = 0.9602664292544597

Mean recall score 0.935101641392856

C parameter: 1

Iteration 0 : recall score = 0.8903225806451613

Iteration 1 : recall score = 0.8947368421052632

Iteration 2 : recall score = 0.9706318468518313

Iteration 3 : recall score = 0.9603543597014761

Iteration 4 : recall score = 0.9607060814895417

Mean recall score 0.9353503421586546

C parameter: 10

Iteration 0 : recall score = 0.8903225806451613

Iteration 1 : recall score = 0.8947368421052632

Iteration 2 : recall score = 0.9705433218988603

Iteration 3 : recall score = 0.9602994031720908

Iteration 4 : recall score = 0.9609368989129599

Mean recall score 0.9353678093468669

C parameter: 100

Iteration 0 : recall score = 0.8903225806451613

Iteration 1 : recall score = 0.8947368421052632

Iteration 2 : recall score = 0.9706982405665597

Iteration 3 : recall score = 0.9602884118662138

Iteration 4 : recall score = 0.9607830206306811

Mean recall score 0.9353658191627758

Best model to choose from cross validation is with C parameter = 10.0

4.10 逻辑回归计算混淆矩阵以及召回率

lr = LogisticRegression(C = best_c, penalty = 'l1',solver='liblinear')

lr.fit(os_features,os_labels.values.ravel())

y_pred = lr.predict(features_test.values)

# 计算混淆矩阵

cnf_matrix = confusion_matrix(labels_test,y_pred)

np.set_printoptions(precision=2)

print("Recall metric in the testing dataset: ", cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# 画出非规范化的混淆矩阵

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix

, classes=class_names

, title='Confusion matrix')

plt.show()

输出结果:

小结

虽然过采样的recall值比下采样稍小,但是它的精度却大大提高了,即减少了误杀的数量,所以在出现数据不均衡的情况下,较经常使用的是生成数据而不是减少数据,但是数据一旦多起来,运行时间也变长了。

4923

4923

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言