简介

PCA是一种属降维方法,将众多具有一定相关性的变量重组为一组新的相互无关的综合变量,可以用作降维或评价(建议不用,因为新综合变量很难解释)。此方法在实际运用中有一个难点,就是选择主成分后,需要注意主成分实际含义的解释(难点)。

PCA步骤

1、原始数据标准化处理

2、计算样本相关系数矩阵

3、计算相关系数矩阵的特征值以及相应的特征向量

4、选择主成分并写出表达式

根据贡献率选出主成分

5、计算主成分得分:样本数据*主成分特征向量

6、进一步分析

实现代码

% Read data from a file (e.g. excel) and place it in a matrix.

A=xlsread('Coporation_evaluation.xlsx', 'B2:I16');

% Transfer orginal data to standard data

a=size(A,1); % Get the row number of A

b=size(A,2); % Get the column number of A

for i=1:b

SA(:,i)=(A(:,i)-mean(A(:,i)))/std(A(:,i)); % Matrix normalization

end

% Calculate correlation matrix of A.

CM=corrcoef(SA);

% Calculate eigenvectors and eigenvalues of correlation matrix.

[V, D]=eig(CM);

% Get the eigenvalue sequence according to descending and the corrosponding

% attribution rates and accumulation rates.

for j=1:b

DS(j,1)=D(b+1-j, b+1-j);

end

for i=1:b

DS(i,2)=DS(i,1)/sum(DS(:,1)); % 贡献率

DS(i,3)=sum(DS(1:i,1))/sum(DS(:,1)); % 累计贡献率

end

% Calculate the numvber of principal components.

T=0.9; % set the threshold value for evaluating information preservation level.

for K=1:b

if DS(K,3)>=T

Com_num=K;

break;

end

end

% Get the eigenvectors of the Com_num principal components

for j=1:Com_num

PV(:,j)=V(:,b+1-j); % 与之前倒序排列的特征值相匹配,故需要倒序

end

% Calculate the new socres of the orginal items

new_score=SA*PV;

for i=1:a

total_score(i,2)=sum(new_score(i,:));

total_score(i,1)=i;

end

new_score_s=sortrows(total_score,-2);

% Displays result reports

disp('特征值及贡献率:')

DS

disp('阀值T对应的主成分数与特征向量:')

Com_num

PV

disp('主成分分数:')

new_score

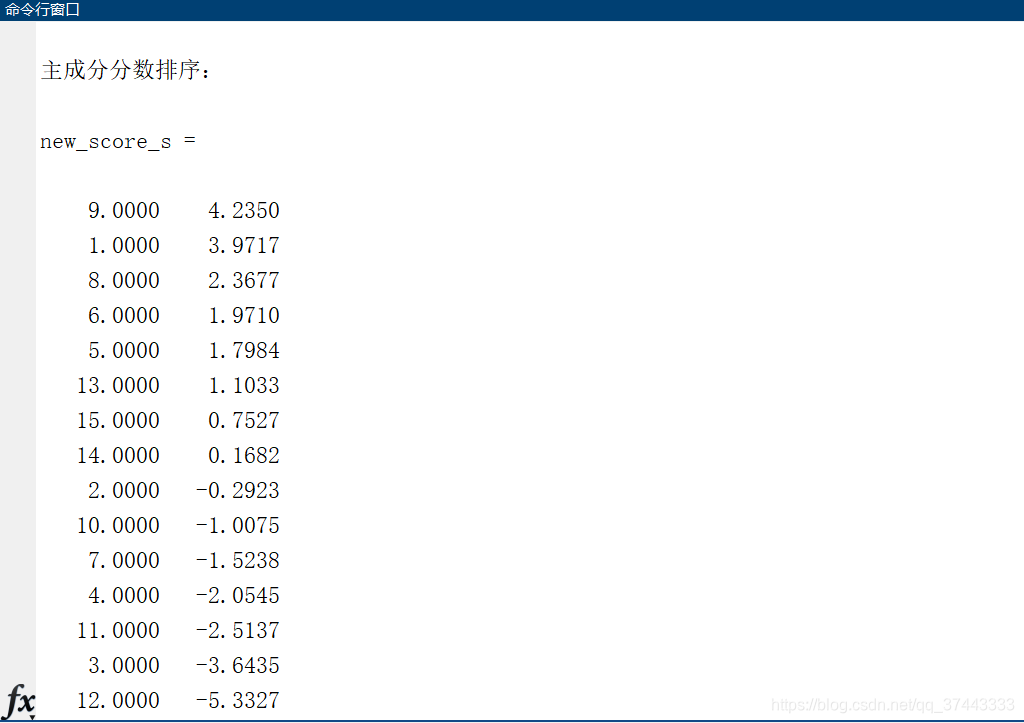

disp('主成分分数排序:')

new_score_s

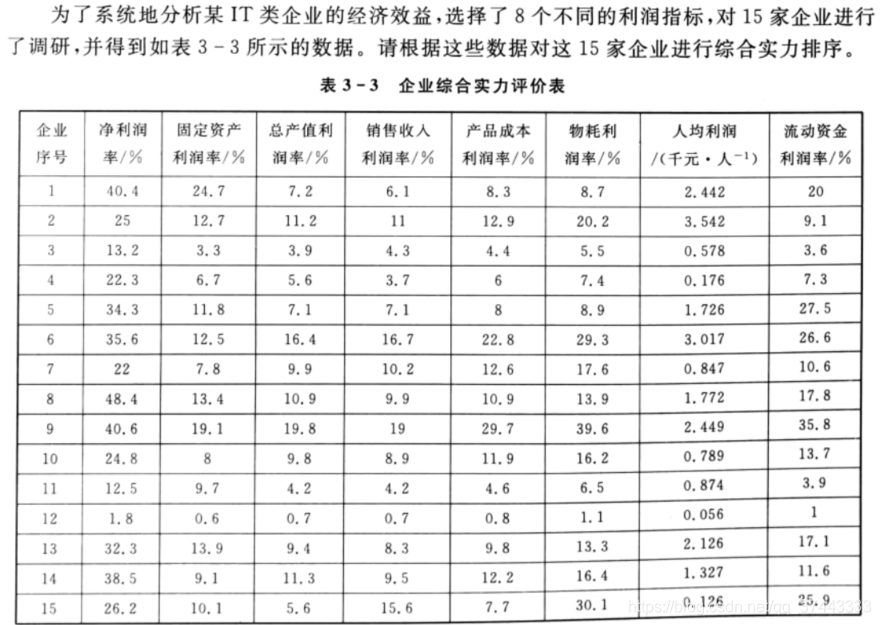

易知第9家综合实力最强,第12家综合实力最弱

2237

2237

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言