文章目录

评分卡模型

- scorecardpy库

github地址:https://github.com/ShichenXie/scorecardpy

一、数据预处理

import scorecardpy as sc

import pandas as pd

import numpy as np

scorecardpy自带数据

dat = sc.germancredit()

查看数据行列

dat.shape

(1000, 21)

数据是由1000行,21列数据组成

查看数据内容,用sample()比head()可以看更多的数据

dat.sample(5)

| status.of.existing.checking.account | duration.in.month | credit.history | purpose | credit.amount | savings.account.and.bonds | present.employment.since | installment.rate.in.percentage.of.disposable.income | personal.status.and.sex | other.debtors.or.guarantors | ... | property | age.in.years | other.installment.plans | housing | number.of.existing.credits.at.this.bank | job | number.of.people.being.liable.to.provide.maintenance.for | telephone | foreign.worker | creditability | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 547 | no checking account | 24 | existing credits paid back duly till now | radio/television | 1552 | ... < 100 DM | 4 <= ... < 7 years | 3 | male : single | none | ... | car or other, not in attribute Savings account... | 32 | bank | own | 1 | skilled employee / official | 2 | none | yes | good |

| 617 | ... < 0 DM | 6 | critical account/ other credits existing (not ... | car (new) | 3676 | ... < 100 DM | 1 <= ... < 4 years | 1 | male : single | none | ... | real estate | 37 | none | rent | 3 | skilled employee / official | 2 | none | yes | good |

| 186 | 0 <= ... < 200 DM | 9 | all credits at this bank paid back duly | car (used) | 5129 | ... < 100 DM | ... >= 7 years | 2 | female : divorced/separated/married | none | ... | unknown / no property | 74 | bank | for free | 1 | management/ self-employed/ highly qualified em... | 2 | yes, registered under the customers name | yes | bad |

| 776 | no checking account | 36 | critical account/ other credits existing (not ... | car (new) | 3535 | ... < 100 DM | 4 <= ... < 7 years | 4 | male : single | none | ... | car or other, not in attribute Savings account... | 37 | none | own | 2 | skilled employee / official | 1 | yes, registered under the customers name | yes | good |

| 243 | no checking account | 12 | critical account/ other credits existing (not ... | business | 1185 | ... < 100 DM | 1 <= ... < 4 years | 3 | female : divorced/separated/married | none | ... | real estate | 27 | none | own | 2 | skilled employee / official | 1 | none | yes | good |

5 rows × 21 columns

可以发现有none出现,代表的是缺失,可以用np.nan替换,方便统计每一个变量的缺失占比情况dat = dat.replace('none',np.nan)

统计每个变量的缺失占比情况

(dat.isnull().sum()/dat.shape[0]).map(lambda x:"{:.2%}".format(x))

status.of.existing.checking.account 0.00%

duration.in.month 0.00%

credit.history 0.00%

purpose 0.00%

credit.amount 0.00%

savings.account.and.bonds 0.00%

present.employment.since 0.00%

installment.rate.in.percentage.of.disposable.income 0.00%

personal.status.and.sex 0.00%

other.debtors.or.guarantors 90.70%

present.residence.since 0.00%

property 0.00%

age.in.years 0.00%

other.installment.plans 81.40%

housing 0.00%

number.of.existing.credits.at.this.bank 0.00%

job 0.00%

number.of.people.being.liable.to.provide.maintenance.for 0.00%

telephone 59.60%

foreign.worker 0.00%

creditability 0.00%

dtype: object

other.debtors.or.guarantors(担保人)这一列数据的缺失占比超过90%,可以删除。

other.installment.plans(分期付款计划)这一列缺失占比也较高,只有两个分类,也可以删除。

dat["other.installment.plans"].value_counts()

bank 139

stores 47

Name: other.installment.plans, dtype: int64

telephone(电话)对建模没有太大意义,就像姓名,对建模没有太大影响。但是电话是否填写应该被考虑进去,这里先不讨论。

dat = dat.drop(columns=["other.debtors.or.guarantors","other.installment.plans","telephone"])

查看数据的信息

dat.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1000 entries, 0 to 999

Data columns (total 18 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 status.of.existing.checking.account 1000 non-null category

1 duration.in.month 1000 non-null int64

2 credit.history 1000 non-null category

3 purpose 1000 non-null object

4 credit.amount 1000 non-null int64

5 savings.account.and.bonds 1000 non-null category

6 present.employment.since 1000 non-null category

7 installment.rate.in.percentage.of.disposable.income 1000 non-null int64

8 personal.status.and.sex 1000 non-null category

9 present.residence.since 1000 non-null int64

10 property 1000 non-null category

11 age.in.years 1000 non-null int64

12 housing 1000 non-null category

13 number.of.existing.credits.at.this.bank 1000 non-null int64

14 job 1000 non-null category

15 number.of.people.being.liable.to.provide.maintenance.for 1000 non-null int64

16 foreign.worker 1000 non-null category

17 creditability 1000 non-null object

dtypes: category(9), int64(7), object(2)

memory usage: 80.8+ KB

可以看出数据是由int64,category,object类型的数据组成,category类型的数据在pandas中很特殊,建议转为object类型数据。

查看每个变量有多少分类

# 顺便把category类型的数据转为object

for c in dat.columns:

if str(dat[c].dtype) == "category":

dat[c] = dat[c].astype(str)

print(c,":",len(dat[c].unique()))

status.of.existing.checking.account : 4

duration.in.month : 33

credit.history : 5

purpose : 10

credit.amount : 921

savings.account.and.bonds : 5

present.employment.since : 5

installment.rate.in.percentage.of.disposable.income : 4

personal.status.and.sex : 3

present.residence.since : 4

property : 4

age.in.years : 53

housing : 3

number.of.existing.credits.at.this.bank : 4

job : 4

number.of.people.being.liable.to.provide.maintenance.for : 2

foreign.worker : 2

creditability : 2

可以看到credit.amount(金额)有921个不同的类别,age.in.years(年龄)有53个类别。

类别较多的需要合并区间,类别少的视情况而定。

描述性统计

查看每一个变量的均值,最大,最小,分位数

dat.describe()

| duration.in.month | credit.amount | installment.rate.in.percentage.of.disposable.income | present.residence.since | age.in.years | number.of.existing.credits.at.this.bank | number.of.people.being.liable.to.provide.maintenance.for | |

|---|---|---|---|---|---|---|---|

| count | 1000.000000 | 1000.000000 | 1000.000000 | 1000.000000 | 1000.000000 | 1000.000000 | 1000.000000 |

| mean | 20.903000 | 3271.258000 | 2.973000 | 2.845000 | 35.546000 | 1.407000 | 1.155000 |

| std | 12.058814 | 2822.736876 | 1.118715 | 1.103718 | 11.375469 | 0.577654 | 0.362086 |

| min | 4.000000 | 250.000000 | 1.000000 | 1.000000 | 19.000000 | 1.000000 | 1.000000 |

| 25% | 12.000000 | 1365.500000 | 2.000000 | 2.000000 | 27.000000 | 1.000000 | 1.000000 |

| 50% | 18.000000 | 2319.500000 | 3.000000 | 3.000000 | 33.000000 | 1.000000 | 1.000000 |

| 75% | 24.000000 | 3972.250000 | 4.000000 | 4.000000 | 42.000000 | 2.000000 | 1.000000 |

| max | 72.000000 | 18424.000000 | 4.000000 | 4.000000 | 75.000000 | 4.000000 | 2.000000 |

数据之间的相关性

dat.corr()

| duration.in.month | credit.amount | installment.rate.in.percentage.of.disposable.income | present.residence.since | age.in.years | number.of.existing.credits.at.this.bank | number.of.people.being.liable.to.provide.maintenance.for | |

|---|---|---|---|---|---|---|---|

| duration.in.month | 1.000000 | 0.624984 | 0.074749 | 0.034067 | -0.036136 | -0.011284 | -0.023834 |

| credit.amount | 0.624984 | 1.000000 | -0.271316 | 0.028926 | 0.032716 | 0.020795 | 0.017142 |

| installment.rate.in.percentage.of.disposable.income | 0.074749 | -0.271316 | 1.000000 | 0.049302 | 0.058266 | 0.021669 | -0.071207 |

| present.residence.since | 0.034067 | 0.028926 | 0.049302 | 1.000000 | 0.266419 | 0.089625 | 0.042643 |

| age.in.years | -0.036136 | 0.032716 | 0.058266 | 0.266419 | 1.000000 | 0.149254 | 0.118201 |

| number.of.existing.credits.at.this.bank | -0.011284 | 0.020795 | 0.021669 | 0.089625 | 0.149254 | 1.000000 | 0.109667 |

| number.of.people.being.liable.to.provide.maintenance.for | -0.023834 | 0.017142 | -0.071207 | 0.042643 | 0.118201 | 0.109667 | 1.000000 |

二、数据筛选

参考文章:https://zhuanlan.zhihu.com/p/80134853

评分卡建模常用WOE、IV来筛选变量,通常选择IV值>0.02的变量。IV值越大,变量对y的预测能力较强,就越应该进入模型中。

WOE:(Weight of Evidence)中文“证据权重”,某个变量的区间对y的影响程度。

-

计算方法:

W O E i = l n ( R 0 i R 0 T ) − l n ( R 1 i R 1 T ) WOE_i=ln(\frac{R_{0i}}{R_{0T}})-ln(\frac{R_{1i}}{R_{1T}}) WOEi=ln(R0TR0i)−ln(R1TR1i)

R 0 i :变量的第 i 个区间, y = 0 的个数。 R 0 T : y = 0 的个数。 R 1 i :变量的第 i 个区间, y = 1 的个数。 R 1 T : y = 1 的个数。 R_{0i}:变量的第i个区间,y=0的个数。\\ R_{0T}:y=0的个数。 \\ R_{1i}:变量的第i个区间,y=1的个数。\\ R_{1T}:y=1的个数。 R0i:变量的第i个区间,y=0的个数。R0T:y=0的个数。R1i:变量的第i个区间,y=1的个数。R1T:y=1的个数。 -

举例说明:

将age.in.years划分为[-inf,26.0),[26.0,35.0),[35.0,40.0),[40.0,inf)四个区间,统计各个区间y=0(good),y=1(bad)的数量,计算WOE。

比如计算age.in.year在[26,35)区间的WOE:

W O E i = l n ( R 0 i R 0 T ) − l n ( R 1 i R 1 T ) = l n ( 246 700 ) − l n ( 112 300 ) = − 0.060465 WOE_i=ln(\frac{R_{0i}}{R_{0T}})-ln(\frac{R_{1i}}{R_{1T}})=ln(\frac{246}{700})-ln(\frac{112}{300})=-0.060465 WOEi=ln(R0TR0i)−ln(R1TR1i)=ln(700246)−ln(300112)=−0.060465

同理可以计算出其他区间对应的WOE值。

IV:(Information Value)中文“信息价值”,变量所含信息的价值。

- 计算方法:

I V = ∑ i = 1 n ( R 0 i R 0 T − R 1 i R 1 T ) ∗ W O E i IV=\sum_{i=1}^n(\frac{R_{0i}}{R_{0T}}-\frac{R_{1i}}{R_{1T}})*WOE_i IV=i=1∑n(R0TR0i−R1TR1i)∗WOEi - 举例说明:

I V = ∑ i = 1 n ( R 0 i R 0 T − R 1 i R 1 T ) ∗ W O E i = ( 110 700 − 80 300 ) ∗ 0.528844 + ( 246 700 − 112 300 ) ∗ 0.060465 + ( 123 700 − 30 300 ) ∗ − 0.563689 + ( 221 700 − 78 300 ) ∗ − 0.194156 = 0.112742 IV=\sum_{i=1}^n(\frac{R_{0i}}{R_{0T}}-\frac{R_{1i}}{R_{1T}})*WOE_i\\ =(\frac{110}{700}-\frac{80}{300})*0.528844\\ +(\frac{246}{700}-\frac{112}{300})*0.060465\\ +(\frac{123}{700}-\frac{30}{300})*-0.563689\\ +(\frac{221}{700}-\frac{78}{300})*-0.194156\\ =0.112742 IV=i=1∑n(R0TR0i−R1TR1i)∗WOEi=(700110−30080)∗0.528844+(700246−300112)∗0.060465+(700123−30030)∗−0.563689+(700221−30078)∗−0.194156=0.112742

公式看似复杂,其实仔细想想,用到的知识也不是很难。另外,这些程序scorecardpy中已经实现,只需要调用传参即可。

用scorecardpy计算的age.in.years的WOE:

# bins_adj_df[bins_adj_df.variable=="age.in.years"]

| level_1 | variable | bin | count | count_distr | good | bad | badprob | woe | bin_iv | total_iv | breaks | is_special_values | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 4 | 0 | age.in.years | [-inf,26.0) | 190 | 0.190 | 110 | 80 | 0.421053 | 0.528844 | 0.057921 | 0.112742 | 26.0 | False |

| 5 | 1 | age.in.years | [26.0,35.0) | 358 | 0.358 | 246 | 112 | 0.312849 | 0.060465 | 0.001324 | 0.112742 | 35.0 | False |

| 6 | 2 | age.in.years | [35.0,40.0) | 153 | 0.153 | 123 | 30 | 0.196078 | -0.563689 | 0.042679 | 0.112742 | 40.0 | False |

| 7 | 3 | age.in.years | [40.0,inf) | 299 | 0.299 | 221 | 78 | 0.260870 | -0.194156 | 0.010817 | 0.112742 | inf | False |

sc.var_filter()

- dt:数据

- y:y变量名

- iv_limit:0.02

- missing_limit:0.95

- identical_limit:0.95

- positive:坏样本的标签

- dt:DataFrame数据

- var_rm:强制删除变量的名称

- var_kp:强制保留变量的名称

- return_rm_reason:是否返回每个变量被删除的原因

dt_s = sc.var_filter(dat,y="creditability",iv_limit=0.02)

dat.shape

(1000, 18)

dt_s.shape

(1000, 13)

可以看出,用var_filter()方法,将变量从18个筛选到13个变量。

划分数据

sc.split_df(dt, y=None, ratio=0.7, seed=186)

train,test = sc.split_df(dt=dt_s,y="creditability").values()

训练数据y的统计:

train.creditability.value_counts()

0 490

1 210

Name: creditability, dtype: int64

测试数据y的统计:

test.creditability.value_counts()

0 210

1 90

Name: creditability, dtype: int64

三、 变量分箱

常用的分箱:卡方分箱,决策树分箱… ,这里简单介绍一下卡方分箱。

为什么要分箱?

分箱之后,变量的轻微波动,不影响模型的稳定。比如:收入这一变量,10000和11000对y的影响可能是一样的,将其归为一类是一个不错的选择。

分箱要求?

- 变量的类别在5到7类最好

- 有序,单调,平衡

卡方分箱:

参考文章:https://zhuanlan.zhihu.com/p/115267395

- 卡方分箱的思想,衡量预测值与观察值的差异,究竟有多大的概率是由随机因素引起的。

- 卡方值计算:

χ 2 = ∑ i = 1 n ∑ c = 1 m ( A i c − E i c ) 2 E i c \chi^2=\sum_{i=1}^n\sum_{c=1}^m\frac{(A_{ic}-E_{ic})^2}{E_{ic}} χ2=i=1∑nc=1∑mEic(Aic−Eic)2

n :划分的区间总数。 m : y 的类别,一般为 2 个。 A i c :实际样本在每个区间统计的数量。 n:划分的区间总数。\\ m:y的类别,一般为2个。 \\ A_{ic}:实际样本在每个区间统计的数量。 n:划分的区间总数。m:y的类别,一般为2个。Aic:实际样本在每个区间统计的数量。

E i c :期望样本在每个区间的数量, E i c = T i ∗ T c T , T i :第 i 个分组的总数, T c :第 c 个类别的总数, T :总样本数。 E_{ic}:期望样本在每个区间的数量,E_{ic}=\frac{T_i*T_c}{T},T_i:第i个分组的总数,T_c:第c个类别的总数,T:总样本数。 Eic:期望样本在每个区间的数量,Eic=TTi∗Tc,Ti:第i个分组的总数,Tc:第c个类别的总数,T:总样本数。

- 步骤:(数值型数据)

- 将数据去重并排序,得到A1,A2,A3等分组区间,统计每个区间的量。

- 计算A1与A2的卡方值,计算A2与A3的卡方值,(计算相邻区间的卡方值)

- 如果相邻的卡方值小于阈值(根据自由度和置信度计算得出的出的阈值),就合并区间为一个新的区间。

- 重复第2、3步的操作。直到达到某个条件停止计算。

- 当最小的卡方值大于阈值,停止。

- 当划分的区间到达指定的区间个数,停止。

woebin()

- scorecardpy默认使用决策树分箱,method=‘tree’

- 这里使用卡方分箱,method=‘chimerge’

- 返回的是一个字典数据,用pandas.concat()查看所有数据

bins = sc.woebin(dt_s,y="creditability",method="chimerge")

bins["installment.rate.in.percentage.of.disposable.income"]

| variable | bin | count | count_distr | good | bad | badprob | woe | bin_iv | total_iv | breaks | is_special_values | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | installment.rate.in.percentage.of.disposable.i... | [-inf,3.0) | 367 | 0.367 | 271 | 96 | 0.261580 | -0.190473 | 0.012789 | 0.019769 | 3.0 | False |

| 1 | installment.rate.in.percentage.of.disposable.i... | [3.0,inf) | 633 | 0.633 | 429 | 204 | 0.322275 | 0.103961 | 0.006980 | 0.019769 | inf | False |

bins_df = pd.concat(bins).reset_index().drop(columns="level_0")

bins_df

| level_1 | variable | bin | count | count_distr | good | bad | badprob | woe | bin_iv | total_iv | breaks | is_special_values | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | credit.amount | [-inf,1400.0) | 267 | 0.267 | 185 | 82 | 0.307116 | 0.033661 | 0.000305 | 0.171431 | 1400.0 | False |

| 1 | 1 | credit.amount | [1400.0,1800.0) | 105 | 0.105 | 87 | 18 | 0.171429 | -0.728239 | 0.046815 | 0.171431 | 1800.0 | False |

| 2 | 2 | credit.amount | [1800.0,2000.0) | 60 | 0.060 | 39 | 21 | 0.350000 | 0.228259 | 0.003261 | 0.171431 | 2000.0 | False |

| 3 | 3 | credit.amount | [2000.0,4000.0) | 322 | 0.322 | 248 | 74 | 0.229814 | -0.362066 | 0.038965 | 0.171431 | 4000.0 | False |

| 4 | 4 | credit.amount | [4000.0,inf) | 246 | 0.246 | 141 | 105 | 0.426829 | 0.552498 | 0.082085 | 0.171431 | inf | False |

| 5 | 0 | age.in.years | [-inf,26.0) | 190 | 0.190 | 110 | 80 | 0.421053 | 0.528844 | 0.057921 | 0.123935 | 26.0 | False |

| 6 | 1 | age.in.years | [26.0,35.0) | 358 | 0.358 | 246 | 112 | 0.312849 | 0.060465 | 0.001324 | 0.123935 | 35.0 | False |

| 7 | 2 | age.in.years | [35.0,37.0) | 79 | 0.079 | 67 | 12 | 0.151899 | -0.872488 | 0.048610 | 0.123935 | 37.0 | False |

| 8 | 3 | age.in.years | [37.0,inf) | 373 | 0.373 | 277 | 96 | 0.257373 | -0.212371 | 0.016080 | 0.123935 | inf | False |

| 9 | 0 | housing | own | 713 | 0.713 | 527 | 186 | 0.260870 | -0.194156 | 0.025795 | 0.082951 | own | False |

| 10 | 1 | housing | rent%,%for free | 287 | 0.287 | 173 | 114 | 0.397213 | 0.430205 | 0.057156 | 0.082951 | rent%,%for free | False |

| 11 | 0 | property | real estate | 282 | 0.282 | 222 | 60 | 0.212766 | -0.461035 | 0.054007 | 0.112634 | real estate | False |

| 12 | 1 | property | building society savings agreement/ life insur... | 564 | 0.564 | 391 | 173 | 0.306738 | 0.031882 | 0.000577 | 0.112634 | building society savings agreement/ life insur... | False |

| 13 | 2 | property | unknown / no property | 154 | 0.154 | 87 | 67 | 0.435065 | 0.586082 | 0.058050 | 0.112634 | unknown / no property | False |

| 14 | 0 | duration.in.month | [-inf,8.0) | 87 | 0.087 | 78 | 9 | 0.103448 | -1.312186 | 0.106849 | 0.282618 | 8.0 | False |

| 15 | 1 | duration.in.month | [8.0,16.0) | 344 | 0.344 | 264 | 80 | 0.232558 | -0.346625 | 0.038294 | 0.282618 | 16.0 | False |

| 16 | 2 | duration.in.month | [16.0,34.0) | 399 | 0.399 | 270 | 129 | 0.323308 | 0.108688 | 0.004813 | 0.282618 | 34.0 | False |

| 17 | 3 | duration.in.month | [34.0,44.0) | 100 | 0.100 | 58 | 42 | 0.420000 | 0.524524 | 0.029973 | 0.282618 | 44.0 | False |

| 18 | 4 | duration.in.month | [44.0,inf) | 70 | 0.070 | 30 | 40 | 0.571429 | 1.134980 | 0.102689 | 0.282618 | inf | False |

| 19 | 0 | status.of.existing.checking.account | no checking account | 394 | 0.394 | 348 | 46 | 0.116751 | -1.176263 | 0.404410 | 0.666012 | no checking account | False |

| 20 | 1 | status.of.existing.checking.account | ... >= 200 DM / salary assignments for at leas... | 63 | 0.063 | 49 | 14 | 0.222222 | -0.405465 | 0.009461 | 0.666012 | ... >= 200 DM / salary assignments for at leas... | False |

| 21 | 2 | status.of.existing.checking.account | 0 <= ... < 200 DM | 269 | 0.269 | 164 | 105 | 0.390335 | 0.401392 | 0.046447 | 0.666012 | 0 <= ... < 200 DM | False |

| 22 | 3 | status.of.existing.checking.account | ... < 0 DM | 274 | 0.274 | 139 | 135 | 0.492701 | 0.818099 | 0.205693 | 0.666012 | ... < 0 DM | False |

| 23 | 0 | installment.rate.in.percentage.of.disposable.i... | [-inf,3.0) | 367 | 0.367 | 271 | 96 | 0.261580 | -0.190473 | 0.012789 | 0.019769 | 3.0 | False |

| 24 | 1 | installment.rate.in.percentage.of.disposable.i... | [3.0,inf) | 633 | 0.633 | 429 | 204 | 0.322275 | 0.103961 | 0.006980 | 0.019769 | inf | False |

| 25 | 0 | savings.account.and.bonds | ... >= 1000 DM%,%500 <= ... < 1000 DM%,%unknow... | 294 | 0.294 | 245 | 49 | 0.166667 | -0.762140 | 0.142266 | 0.189391 | ... >= 1000 DM%,%500 <= ... < 1000 DM%,%unknow... | False |

| 26 | 1 | savings.account.and.bonds | 100 <= ... < 500 DM%,%... < 100 DM | 706 | 0.706 | 455 | 251 | 0.355524 | 0.252453 | 0.047125 | 0.189391 | 100 <= ... < 500 DM%,%... < 100 DM | False |

| 27 | 0 | present.employment.since | 4 <= ... < 7 years%,%... >= 7 years | 427 | 0.427 | 324 | 103 | 0.241218 | -0.298717 | 0.035704 | 0.082865 | 4 <= ... < 7 years%,%... >= 7 years | False |

| 28 | 1 | present.employment.since | 1 <= ... < 4 years | 339 | 0.339 | 235 | 104 | 0.306785 | 0.032103 | 0.000352 | 0.082865 | 1 <= ... < 4 years | False |

| 29 | 2 | present.employment.since | unemployed%,%... < 1 year | 234 | 0.234 | 141 | 93 | 0.397436 | 0.431137 | 0.046809 | 0.082865 | unemployed%,%... < 1 year | False |

| 30 | 0 | personal.status.and.sex | male : single%,%male : married/widowed | 640 | 0.640 | 469 | 171 | 0.267188 | -0.161641 | 0.016164 | 0.042633 | male : single%,%male : married/widowed | False |

| 31 | 1 | personal.status.and.sex | female : divorced/separated/married | 360 | 0.360 | 231 | 129 | 0.358333 | 0.264693 | 0.026469 | 0.042633 | female : divorced/separated/married | False |

| 32 | 0 | credit.history | critical account/ other credits existing (not ... | 293 | 0.293 | 243 | 50 | 0.170648 | -0.733741 | 0.132423 | 0.291829 | critical account/ other credits existing (not ... | False |

| 33 | 1 | credit.history | delay in paying off in the past%,%existing cre... | 618 | 0.618 | 421 | 197 | 0.318770 | 0.087869 | 0.004854 | 0.291829 | delay in paying off in the past%,%existing cre... | False |

| 34 | 2 | credit.history | all credits at this bank paid back duly%,%no c... | 89 | 0.089 | 36 | 53 | 0.595506 | 1.234071 | 0.154553 | 0.291829 | all credits at this bank paid back duly%,%no c... | False |

| 35 | 0 | purpose | retraining%,%car (used)%,%radio/television | 392 | 0.392 | 312 | 80 | 0.204082 | -0.513679 | 0.091973 | 0.142092 | retraining%,%car (used)%,%radio/television | False |

| 36 | 1 | purpose | furniture/equipment%,%domestic appliances%,%bu... | 608 | 0.608 | 388 | 220 | 0.361842 | 0.279920 | 0.050119 | 0.142092 | furniture/equipment%,%domestic appliances%,%bu... | False |

woebin_plot()

- 制作变量分布图

bins["age.in.years"]

| variable | bin | count | count_distr | good | bad | badprob | woe | bin_iv | total_iv | breaks | is_special_values | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | age.in.years | [-inf,26.0) | 190 | 0.190 | 110 | 80 | 0.421053 | 0.528844 | 0.057921 | 0.123935 | 26.0 | False |

| 1 | age.in.years | [26.0,35.0) | 358 | 0.358 | 246 | 112 | 0.312849 | 0.060465 | 0.001324 | 0.123935 | 35.0 | False |

| 2 | age.in.years | [35.0,37.0) | 79 | 0.079 | 67 | 12 | 0.151899 | -0.872488 | 0.048610 | 0.123935 | 37.0 | False |

| 3 | age.in.years | [37.0,inf) | 373 | 0.373 | 277 | 96 | 0.257373 | -0.212371 | 0.016080 | 0.123935 | inf | False |

sc.woebin_plot(bins["age.in.years"])

sc.woebin_plot(bins["credit.amount"])

从变量的分布图,看出bad_prob、credit.amount这两个变量并不单调,接下来就需要调整一下区间。

分箱调整

- scorecardpy可以自定义分箱,也可以自动分箱。

- 自己手动调整比较好(根据业务,实际经验调整)

# 自动分箱

# break_adj = sc.woebin_adj(dt_s,y="creditability",bins=bins)

bins["credit.amount"]

| variable | bin | count | count_distr | good | bad | badprob | woe | bin_iv | total_iv | breaks | is_special_values | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | credit.amount | [-inf,1400.0) | 267 | 0.267 | 185 | 82 | 0.307116 | 0.033661 | 0.000305 | 0.171431 | 1400.0 | False |

| 1 | credit.amount | [1400.0,1800.0) | 105 | 0.105 | 87 | 18 | 0.171429 | -0.728239 | 0.046815 | 0.171431 | 1800.0 | False |

| 2 | credit.amount | [1800.0,2000.0) | 60 | 0.060 | 39 | 21 | 0.350000 | 0.228259 | 0.003261 | 0.171431 | 2000.0 | False |

| 3 | credit.amount | [2000.0,4000.0) | 322 | 0.322 | 248 | 74 | 0.229814 | -0.362066 | 0.038965 | 0.171431 | 4000.0 | False |

| 4 | credit.amount | [4000.0,inf) | 246 | 0.246 | 141 | 105 | 0.426829 | 0.552498 | 0.082085 | 0.171431 | inf | False |

# 手动分箱

break_adj = {

'age.in.years':[26,35,40],

'credit.amount':[1400,1900,4000]

}

bins_adj = sc.woebin(dt_s,y="creditability",breaks_list=break_adj)

bins_adj_df = pd.concat(bins_adj).reset_index().drop(columns="level_0")

bins_adj_df[bins_adj_df.variable.isin(["age.in.years",'credit.amount'])]

| level_1 | variable | bin | count | count_distr | good | bad | badprob | woe | bin_iv | total_iv | breaks | is_special_values | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | credit.amount | [-inf,1400.0) | 267 | 0.267 | 185 | 82 | 0.307116 | 0.033661 | 0.000305 | 0.141144 | 1400.0 | False |

| 1 | 1 | credit.amount | [1400.0,1900.0) | 131 | 0.131 | 104 | 27 | 0.206107 | -0.501256 | 0.029359 | 0.141144 | 1900.0 | False |

| 2 | 2 | credit.amount | [1900.0,4000.0) | 356 | 0.356 | 270 | 86 | 0.241573 | -0.296777 | 0.029395 | 0.141144 | 4000.0 | False |

| 3 | 3 | credit.amount | [4000.0,inf) | 246 | 0.246 | 141 | 105 | 0.426829 | 0.552498 | 0.082085 | 0.141144 | inf | False |

| 4 | 0 | age.in.years | [-inf,26.0) | 190 | 0.190 | 110 | 80 | 0.421053 | 0.528844 | 0.057921 | 0.112742 | 26.0 | False |

| 5 | 1 | age.in.years | [26.0,35.0) | 358 | 0.358 | 246 | 112 | 0.312849 | 0.060465 | 0.001324 | 0.112742 | 35.0 | False |

| 6 | 2 | age.in.years | [35.0,40.0) | 153 | 0.153 | 123 | 30 | 0.196078 | -0.563689 | 0.042679 | 0.112742 | 40.0 | False |

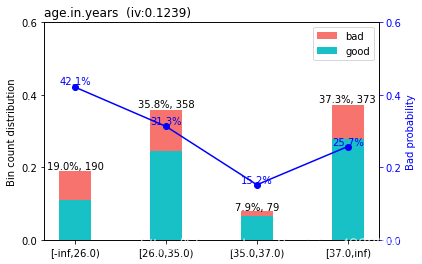

| 7 | 3 | age.in.years | [40.0,inf) | 299 | 0.299 | 221 | 78 | 0.260870 | -0.194156 | 0.010817 | 0.112742 | inf | False |

sc.woebin_plot(bins_adj["age.in.years"])

sc.woebin_plot(bins_adj['credit.amount']

四、WOE转化

将原始数据都转化为对应区间的WOE值,当然也可以不转化,但是转化之后:

- 变量内部之间可以比较

- 变量与变量之间也可以比较

- 所有变量都在同一“维度”下

train_woe = sc.woebin_ply(train,bins_adj)

test_woe = sc.woebin_ply(test,bins_adj)

train_woe.sample(5)

| creditability | credit.amount_woe | age.in.years_woe | housing_woe | property_woe | duration.in.month_woe | status.of.existing.checking.account_woe | installment.rate.in.percentage.of.disposable.income_woe | savings.account.and.bonds_woe | present.employment.since_woe | personal.status.and.sex_woe | credit.history_woe | purpose_woe | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 723 | 0 | 0.033661 | -0.194156 | -0.194156 | -0.461035 | -0.346625 | 0.614204 | 0.103961 | -0.762140 | 0.032103 | 0.264693 | 0.088319 | -0.410063 |

| 331 | 1 | -0.501256 | 0.060465 | -0.194156 | -0.461035 | 0.108688 | -1.176263 | 0.103961 | 0.139552 | 0.032103 | 0.264693 | -0.733741 | 0.279920 |

| 690 | 0 | 0.033661 | 0.528844 | -0.194156 | 0.028573 | -0.346625 | 0.614204 | -0.155466 | 0.271358 | 0.032103 | 0.264693 | -0.733741 | 0.279920 |

| 537 | 0 | -0.296777 | -0.563689 | -0.194156 | 0.028573 | 0.108688 | 0.614204 | 0.103961 | 0.271358 | -0.235566 | 0.264693 | -0.733741 | 0.279920 |

| 0 | 0 | 0.033661 | -0.194156 | -0.194156 | -0.461035 | -1.312186 | 0.614204 | 0.103961 | -0.762140 | -0.235566 | -0.165548 | -0.733741 | -0.410063 |

五、建立模型

逻辑回归,挺复杂的。

from sklearn.linear_model import LogisticRegression

y_train = train_woe.loc[:,"creditability"]

X_train = train_woe.loc[:,train_woe.columns!="creditability"]

y_test = test_woe.loc[:,"creditability"]

X_test = test_woe.loc[:,test_woe.columns!="creditability"]

lr = LogisticRegression(penalty='l1',C=0.9,solver='saga',n_jobs=-1)

lr.fit(X_train,y_train)

LogisticRegression(C=0.9, n_jobs=-1, penalty='l1', solver='saga')

lr.coef_

array([[0.77881419, 0.6892819 , 0.36660545, 0.37598509, 0.59990642,

0.75916199, 1.68181704, 0.50153176, 0.23641609, 0.70438936,

0.63125597, 0.99437898]])

lr.intercept_

array([-0.82463787])

六、模型评估

逻辑回归,预测结果为接近1的概率值。

0.6表示:数据划分为标签1的概率为0.6。那么究竟多大的概率才能划为标签1呢?这就需要一个阈值。这个阈值可以根据KS的值来确定。高于阈值得划分为1标签,低于阈值得划分为0标签。

TRP与FRP:

T

R

P

=

预测为

1

,真实值为

1

的数据量

预测为

1

的总量

TRP=\frac{预测为1,真实值为1的数据量}{预测为1的总量}

TRP=预测为1的总量预测为1,真实值为1的数据量

F

R

P

=

预测为

0

,真实值为

1

的数据量

预测为

0

的总量

FRP=\frac{预测为0,真实值为1的数据量}{预测为0的总量}

FRP=预测为0的总量预测为0,真实值为1的数据量

ROC曲线绘制步骤:

- 将预测的y_score去重排序后得到一系列阈值。

- 用每一个y_score做为阈值,统计数量并计算TRP、FRP的值。

- 这样得到一组数据后,以FPR为横坐标,TPR为纵轴标绘制图像。

AUC:

- ROC曲线与横坐标轴围成的面积。

KS曲线:用来确定最好的阈值

K

S

=

m

a

x

(

T

R

P

−

F

R

P

)

KS=max(TRP-FRP)

KS=max(TRP−FRP)

- x轴为一些阈值的长度(区间序号都行),将TRP、FRP绘制在同一个坐标轴中。

train_pred = lr.predict_proba(X_train)[:,1]

test_pred = lr.predict_proba(X_test)[:,1]

train_perf = sc.perf_eva(y_train,train_pred,title="train")

test_perf = sc.perf_eva(y_test,test_pred,title="test")

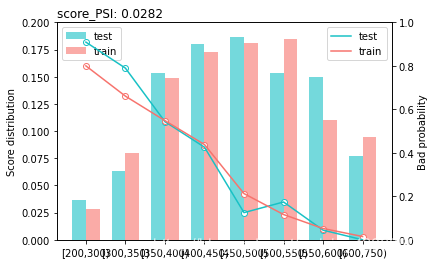

七、评分稳定性

PSI(Population Stability Index)群组稳定性指标

- 模型在训练数据得到的实际分布(A),与测试集上得到的预期分布(E)

P S I = ∑ i = 1 n ( A i − E i ) ∗ l n ( A i E i ) PSI=\sum_{i=1}^n(A_i-E_i)*ln(\frac{A_i}{E_i}) PSI=i=1∑n(Ai−Ei)∗ln(EiAi)

A i :实际分布在第 i 个区间的数量。 A_i:实际分布在第i个区间的数量。 Ai:实际分布在第i个区间的数量。

E i :预期分布在第 i 个区间的数量。 E_i:预期分布在第i个区间的数量。 Ei:预期分布在第i个区间的数量。

PSI越小,说明模型越稳定。通常PSI小于0.1,模型稳定性好。

train_score = sc.scorecard_ply(train, card, print_step=0)

test_score = sc.scorecard_ply(test, card, print_step=0)

sc.perf_psi(

score = {'train':train_score,'test':test_score},

label = {'train':y_train,'test':y_test}

)

评分映射

参考地址:https://github.com/xsj0609/data_science/tree/master/ScoreCard

逻辑回归结果:

f

(

x

)

=

β

0

+

β

1

x

1

+

β

2

x

2

+

.

.

.

+

β

n

x

n

f(x)=\beta_0+\beta_1x_1+\beta_2x_2+...+\beta_nx_n

f(x)=β0+β1x1+β2x2+...+βnxn

评分计算公式:

S

c

o

r

e

=

A

−

B

∗

l

o

g

(

p

1

−

p

)

,

p

:客户违约率

Score=A-B*log(\frac{p}{1-p}),p:客户违约率

Score=A−B∗log(1−pp),p:客户违约率

计算评分前需要先给出两个条件:

1

、给定某个违约率,对应的分数

P

0

。

s

c

o

r

e

c

a

r

d

p

y

默认

θ

0

=

1

19

,

P

0

=

600

2

、当违约率翻一番的时候,分数变化幅度

P

D

O

。

s

c

o

r

e

c

a

r

d

p

y

默认

P

D

O

=

50

1、给定某个违约率,对应的分数P_0。scorecardpy默认\theta_0=\frac{1}{19},P_0=600\\ 2、当违约率翻一番的时候,分数变化幅度PDO。scorecardpy默认PDO=50

1、给定某个违约率,对应的分数P0。scorecardpy默认θ0=191,P0=6002、当违约率翻一番的时候,分数变化幅度PDO。scorecardpy默认PDO=50

通过推导可以计算出:

B

=

P

D

O

l

o

g

(

2

)

,

A

=

P

0

+

B

∗

l

o

g

(

θ

0

)

,

l

o

g

(

p

1

−

p

)

=

f

(

x

)

B=\frac{PDO}{log(2)},A=P_0+B*log(\theta_0),log(\frac{p}{1-p})=f(x)

B=log(2)PDO,A=P0+B∗log(θ0),log(1−pp)=f(x)

举例说明:

计算基础分:

import math

B = 50/math.log(2)

A = 600+B*math.log(1/19)

basepoints=A-B*lr.intercept_[0]

print("A:",A,"B:",B,"basepoints:",basepoints)

A: 387.6036243278207 B: 72.13475204444818 basepoints: 447.0886723193208

credit.amount分数的计算过程

bins_adj_df[bins_adj_df["variable"]=="credit.amount"]

| level_1 | variable | bin | count | count_distr | good | bad | badprob | woe | bin_iv | total_iv | breaks | is_special_values | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | credit.amount | [-inf,1400.0) | 267 | 0.267 | 185 | 82 | 0.307116 | 0.033661 | 0.000305 | 0.141144 | 1400.0 | False |

| 1 | 1 | credit.amount | [1400.0,1900.0) | 131 | 0.131 | 104 | 27 | 0.206107 | -0.501256 | 0.029359 | 0.141144 | 1900.0 | False |

| 2 | 2 | credit.amount | [1900.0,4000.0) | 356 | 0.356 | 270 | 86 | 0.241573 | -0.296777 | 0.029395 | 0.141144 | 4000.0 | False |

| 3 | 3 | credit.amount | [4000.0,inf) | 246 | 0.246 | 141 | 105 | 0.426829 | 0.552498 | 0.082085 | 0.141144 | inf | False |

lr.coef_

array([[0.77881419, 0.6892819 , 0.36660545, 0.37598509, 0.59990642,

0.75916199, 1.68181704, 0.50153176, 0.23641609, 0.70438936,

0.63125597, 0.99437898]])

lr.intercept_

array([-0.82463787])

# [-inf,1400.0)区间分数,按照顺序,对应的系数为0.77881419

-B*0.77881419*0.033661

-1.8910604547516296

# [1400.0,1900.0)

-B*0.77881419*(-0.501256)

28.160345780190216

计算所有区间分数:

card = sc.scorecard(bins_adj,lr,X_train.columns)

card_df = pd.concat(card)

card_df

| variable | bin | points | ||

|---|---|---|---|---|

| basepoints | 0 | basepoints | NaN | 447.0 |

| credit.amount | 0 | credit.amount | [-inf,1400.0) | -2.0 |

| 1 | credit.amount | [1400.0,1900.0) | 28.0 | |

| 2 | credit.amount | [1900.0,4000.0) | 17.0 | |

| 3 | credit.amount | [4000.0,inf) | -31.0 | |

| age.in.years | 4 | age.in.years | [-inf,26.0) | -26.0 |

| 5 | age.in.years | [26.0,35.0) | -3.0 | |

| 6 | age.in.years | [35.0,40.0) | 28.0 | |

| 7 | age.in.years | [40.0,inf) | 10.0 | |

| housing | 8 | housing | own | 5.0 |

| 9 | housing | rent | -11.0 | |

| 10 | housing | for free | -12.0 | |

| property | 11 | property | real estate | 13.0 |

| 12 | property | building society savings agreement/ life insur... | -1.0 | |

| 13 | property | car or other, not in attribute Savings account... | -1.0 | |

| 14 | property | unknown / no property | -16.0 | |

| duration.in.month | 15 | duration.in.month | [-inf,8.0) | 57.0 |

| 16 | duration.in.month | [8.0,16.0) | 15.0 | |

| 17 | duration.in.month | [16.0,34.0) | -5.0 | |

| 18 | duration.in.month | [34.0,44.0) | -23.0 | |

| 19 | duration.in.month | [44.0,inf) | -49.0 | |

| status.of.existing.checking.account | 20 | status.of.existing.checking.account | no checking account | 64.0 |

| 21 | status.of.existing.checking.account | ... >= 200 DM / salary assignments for at leas... | 22.0 | |

| 22 | status.of.existing.checking.account | 0 <= ... < 200 DM%,%... < 0 DM | -34.0 | |

| installment.rate.in.percentage.of.disposable.income | 23 | installment.rate.in.percentage.of.disposable.i... | [-inf,2.0) | 30.0 |

| 24 | installment.rate.in.percentage.of.disposable.i... | [2.0,3.0) | 19.0 | |

| 25 | installment.rate.in.percentage.of.disposable.i... | [3.0,inf) | -13.0 | |

| savings.account.and.bonds | 26 | savings.account.and.bonds | ... >= 1000 DM%,%500 <= ... < 1000 DM%,%unknow... | 28.0 |

| 27 | savings.account.and.bonds | 100 <= ... < 500 DM | -5.0 | |

| 28 | savings.account.and.bonds | ... < 100 DM | -10.0 | |

| present.employment.since | 29 | present.employment.since | 4 <= ... < 7 years | 7.0 |

| 30 | present.employment.since | ... >= 7 years | 4.0 | |

| 31 | present.employment.since | 1 <= ... < 4 years | -1.0 | |

| 32 | present.employment.since | unemployed%,%... < 1 year | -7.0 | |

| personal.status.and.sex | 33 | personal.status.and.sex | male : single | 8.0 |

| 34 | personal.status.and.sex | male : married/widowed | 7.0 | |

| 35 | personal.status.and.sex | female : divorced/separated/married | -13.0 | |

| credit.history | 36 | credit.history | critical account/ other credits existing (not ... | 33.0 |

| 37 | credit.history | delay in paying off in the past | -4.0 | |

| 38 | credit.history | existing credits paid back duly till now | -4.0 | |

| 39 | credit.history | all credits at this bank paid back duly%,%no c... | -56.0 | |

| purpose | 40 | purpose | retraining%,%car (used) | 58.0 |

| 41 | purpose | radio/television | 29.0 | |

| 42 | purpose | furniture/equipment%,%domestic appliances%,%bu... | -20.0 |

至此,评分卡模型完成!

源码地址

链接:https://pan.baidu.com/s/1DAI1hxWPHEb6-46erjDaKg?pwd=e4sw

提取码:e4sw

5030

5030

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言