Why are principal component scores uncorrelated?

Supose A is a matrix of mean-centred data. The matrix S=cov(A) is m×m, has m distinct eigenvalues, and eigenvectors s1, s2 … sm, which are orthogonal.

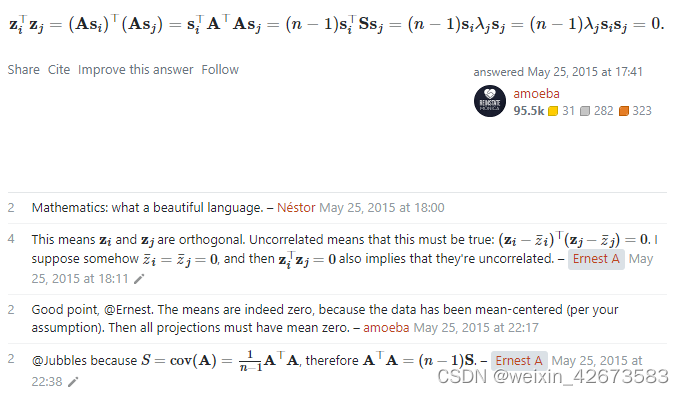

The i-th principal component (some people call them “scores”) is the vector zi=Asi. In other words, it’s a linear combination of the columns of A, where the coefficients are the components of the i-th eigenvector of S.

I don’t understand why zi and zj turn out to be uncorrelated for all i≠j. Does it follow from the fact that si and sj are orthogonal? Surely not, because I can easily find a matrix B and a pair of orthogonal vectors x,y such that Bx and By are correlated.

3万+

3万+

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言