Survival Analysis by Python 生存分析及Python实现

最近学习了Andrew Lo大神的《Econometric Models of Limit-Order Executions》(Journal of Financial Economics,2002),该论文借助Survival Analysis对限价单成交时长进行了建模,借此机会,学习了Survival Analysis的相关内容,记录如下。

总体上看,相比于论文中的分布假设+AFT模型,随着近些年ML的兴起,出现了很多基于ML的Survival Analysis研究。

Survival Analysis介绍

是什么?可以用来做什么?优势是什么?

Survival Analysis是一种统计分析方法,最早由医学研究人员开发使用,用于研究在不同治疗策略下患者的预期寿命,故得此名。

从本质上看,Survival Analysis研究的是在某一特定事件发生前的预期时长(expected duration),所以上面的例子实际上就是研究在death这个事件发生前的预期时长。因此,伴随着对事件的不同定义,Survival Analysis可以用于不同领域。例如,将event定义为客户流失,Survival Analysis可用于对客户留存时长的分析和预测。在Andrew Lo的论文中,event被定义为限价单成交了,于是就可以使用Survival Analysis分析限价单的成交时长。

从以上的内容看,主要目标是预测预期时长,即一个回归问题,那为何要单独提出Survival Analysis这一方法呢?原因是部分数据只能被部分观察到,即出现了censor的现象,例如在研究某种治疗策略的存活时间场景下,某患者在有数据观察的10年里都依然存活或者某患者在10年后退出了研究(观测时长<实际存活时长)。此时,无论是将该患者的存活时间简单截取为10年,还是删去该样本点都是不合适的,都会导致数据被低估。这情况被称为right-censored(实际上还会出现left-censored和interval-censored)。针对包含censor的数据,Survival Analysis中进行了处理,因此特别适用这些场景。在限价单成交时长的场景下,主要是由于有撤单的存在,如果删去这部分撤单的样本,会导致成交时长被低估。

数学定义

Survival Analysis中主要包括S(t)、F(t)、f(t)和h(t)这四个函数。

我们用一个非负、连续随机变量T表示我们的目标,即某一事件发生前的预期时长。例如,客户从订阅到流失的时长、限价单从下单到成交的时长。

T的累积密度函数即CDF用F(t)表示,概率密度函数即PDF用f(t)表示。

事件在t之前发生的概率用F(t)表示,于是有

F

(

t

)

=

P

(

T

<

t

)

=

∫

0

t

f

(

x

)

d

x

F(t) = P(T<t) = \int_0^t f(x)dx

F(t)=P(T<t)=∫0tf(x)dx

存活函数用S(t)表示,即事件在t时刻还没有发生的概率,那么显然有

S

(

t

)

=

P

(

T

≥

t

)

=

1

−

F

(

t

)

=

∫

t

∞

f

(

x

)

d

x

S

(

0

)

=

1

S

(

x

)

>

=

S

(

y

)

∀

x

≤

y

S(t)=P(T\geq t)=1-F(t)=\int_t^{\infty} f(x)dx \\ S(0)=1 \\ S(x) >= S(y) \quad \forall x\leq y

S(t)=P(T≥t)=1−F(t)=∫t∞f(x)dxS(0)=1S(x)>=S(y)∀x≤y

除了以上两个函数之外,一般还关心在t时刻事件还没有发生的条件下,事件瞬间发生概率的函数。该函数一般用h(t)表示,被称为hazard function或instantaneous failure rate。从定义上看,首先分母上是一个条件概率(在t时刻事件还没有发生的条件下),分子上强调瞬间发生,是S(t)曲线的斜率,数学上的表示如下所示

h

(

t

)

=

lim

d

t

→

0

S

(

t

)

−

S

(

t

+

d

t

)

d

t

∗

S

(

t

)

=

f

(

t

)

S

(

t

)

h(t)=\lim_{dt \to 0}\frac{S(t)-S(t+dt)}{dt*S(t)} = \frac{f(t)}{S(t)}

h(t)=dt→0limdt∗S(t)S(t)−S(t+dt)=S(t)f(t)

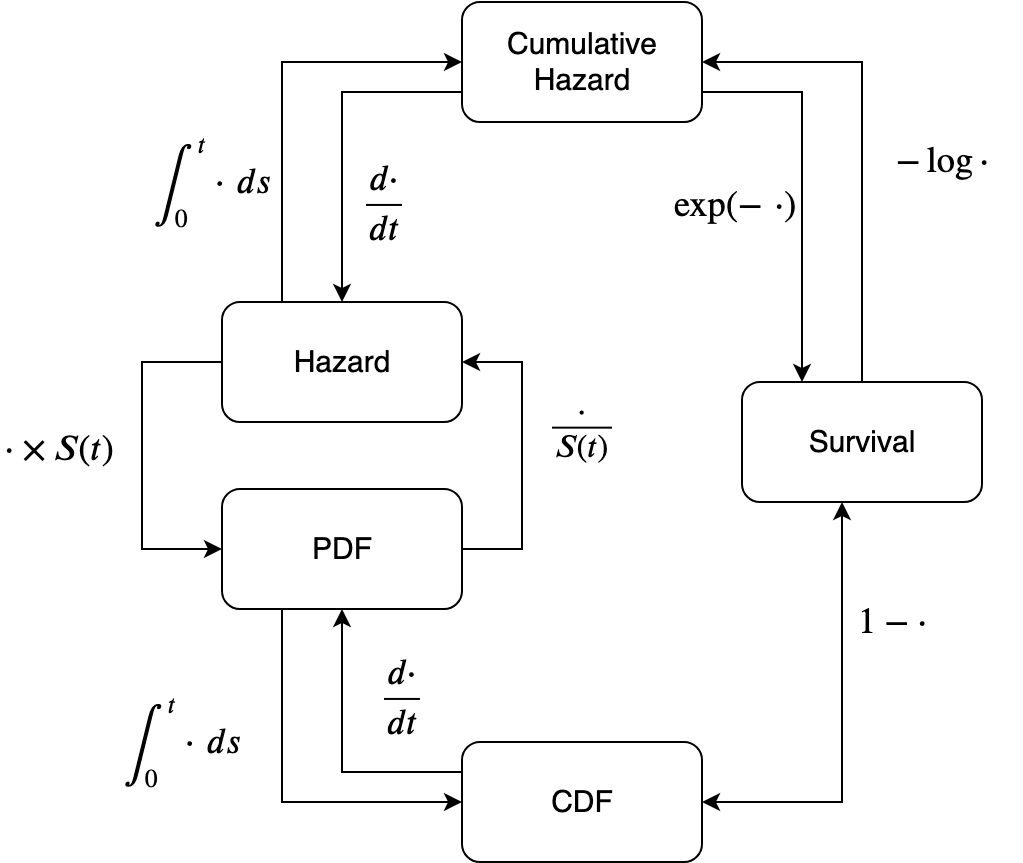

lifelines文档中的图总结了几个函数之间的关系(还包括了h(t)的CDF)

从上面的式子中可以看出,S(t)、F(t)、f(t)和h(t)这四个函数之间存在着联系。知道其中一个函数,便能够推出其他函数。下文将借助于这些函数,介绍预测T的相关模型。

统计检验与模型比较

对统计结果进行检验或者比较模型的优劣,有如下方法。

log-rank检验

用于检验两个或多个population的duration之间是否存在统计差异。

在lifelines中的接口有logrank_test()、pairwise_logrank_test()和multivariate_logrank_test(),前两个接口分别用于检验两个或多个population的duration之间是否存在差异,最后一个接口用于检验是否所有的population的duration存在差异。

Survival differences at a point in time

相比于整个曲线上population的差异,有时候我们更关注某个时间点上population的差异,例如医学上不同治疗策略的5年存活期。

在lifelines中的接口有survival_difference_at_fixed_point_in_time_test。

Restricted mean survival times (RMST)

通过比较曲线下的面积,也可以对两个S(t)曲线之间的差异进行评价。注意的是,主要指定t,因为S(t)曲线的尾部往往差异较大。

R

M

S

T

(

t

)

=

∫

0

t

S

(

r

)

d

r

RMST(t)=\int_0^tS(r)dr

RMST(t)=∫0tS(r)dr

在lifelines中的接口有restricted_mean_survival_time。

QQ图

QQ图通过绘制两个概率分布的分位数来进行比较(QQ plot compares the quantiles of our data against the quantiles of the desired distribution),如果比较的两个分布相似,QQ图上的点大约在y=x线上,如果分布是线性相关的,QQ图上的点大约在一条线上,但不一定是在y=x线上。

以判断我们的数据是否符合正态分布为例,首先计算不同分位数和数据的对应值(our quantile),之后计算这些分位数所对应的正态分布中的值(theoretical quantile),之后将theoretical quantile与our quantile一一组合成(x,y)进行画图。显然,如果我们的数据也满足正态分布,(x,y)会落在y=x的直线上。

percent our_quantile theoretical_quantile

0 0.1 -7.011928 -1.281552

1 0.2 -2.963050 -0.841621

2 0.3 -2.659901 -0.524401

3 0.4 -1.975097 -0.253347

4 0.5 -0.848635 0.000000

5 0.6 -0.050281 0.253347

6 0.7 0.124233 0.524401

7 0.8 0.964039 0.841621

8 0.9 2.484332 1.281552

在lifelines中的接口有qq_plot。

QQ图的相关知识可以参与这个链接https://medium.com/towards-data-science/what-in-the-world-are-qq-plots-20d0e41dece1

Log-likelihood

通过在out-of-sample data上的log-likelihood对模型预测效果进行评价。

在lifelines中的接口score返回了the average evaluation of the out-of-sample log-likelihood。

AIC指标 Akaike information criterion

定义一个AIC指标如下,其中k为模型中的参数个数、ll为maximum log-likelihood。因此,模型AIC越低越优。

A

I

C

(

m

o

d

e

l

)

=

−

2

l

l

+

2

k

AIC(model)=-2ll+2k

AIC(model)=−2ll+2k

在lifelines中的每个模型都有AIC_属性,在Cox中则使用AIC_partial_ 。

Concordance Index 简称为c-index

类似于AUC,用来评价预测时间排序的准确性。数值从0到1,0.5表示随机,一般在0.55到0.75。

在lifelines中,可以在score中指定scoring_method=“concordance_index”,也可以通过模型的concordance_index_属性输出。

实验数据

为了下面的实验,随机生成了如下的一份数据,下列数据读取作为df。

orderIndex表示委托订单编号;

orderBSFlag、orderQty分别表示买卖方向、委托数量;

time-to-first-fill表示从下单到初次成交的时间;(即T)

event_observed表示事件是否被观测到;(1表示观测到了即成交了,0表示未观测到)

| OrderIndex | OrderBSFlag | OrderQty | time-to-first-fill | event_observed |

|---|---|---|---|---|

| 1 | 1 | 100 | 1 | 1 |

| 2 | 2 | 200 | 3 | 1 |

| 3 | 1 | 200 | 5 | 1 |

| 4 | 2 | 100 | 7 | 1 |

| 5 | 1 | 200 | 9 | 1 |

| 6 | 2 | 100 | 2 | 0 |

| 7 | 1 | 200 | 4 | 0 |

| 8 | 2 | 100 | 6 | 0 |

| 9 | 1 | 200 | 8 | 0 |

| 10 | 2 | 100 | 10 | 0 |

单变量模型 univariate models

使用Kaplan-Meier估计S(t)【非参数方法】

Kaplan-Meier Estimate的数学表达式如下所示,其中

d

i

d_i

di表示在

t

i

t_i

ti时刻发生的事件数,

n

i

n_i

ni表示在

t

i

t_i

ti时刻前处于危险中的受试者数量。

S

^

(

t

)

=

∏

t

i

≤

t

n

i

−

d

i

n

i

\hat S(t)= \prod_{t_i\leq t}\frac{n_i-d_i}{n_i}

S^(t)=ti≤t∏nini−di

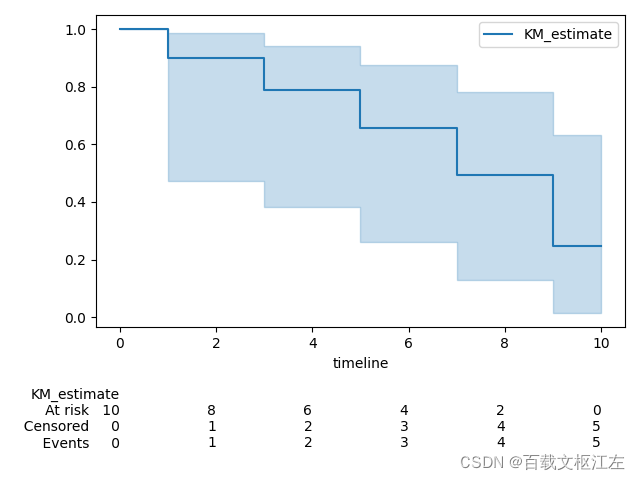

估计S(t)

在实验数据上,S(t)的分布如下所示。

import pandas as pd

from lifelines import KaplanMeierFitter

import matplotlib.pyplot as plt

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

kmf = KaplanMeierFitter()

kmf.fit(durations=df["time-to-first-fill"], event_observed=df["event_observed"])

kmf.plot_survival_function(at_risk_counts=True)

print(pd.DataFrame(kmf.survival_function_))

plt.show()

# KM_estimate

# timeline

# 0.0 1.000000

# 1.0 0.900000

# 2.0 0.900000

# 3.0 0.787500

# 4.0 0.787500

# 5.0 0.656250

# 6.0 0.656250

# 7.0 0.492188

# 8.0 0.492188

# 9.0 0.246094

# 10.0 0.246094

S(1)为0.9的原因是,显然

d

i

d_i

di为1,根据

n

i

n_i

ni的定义计算的是<1分钟的数量,因此为10,所以为(10-1)/10=0.9。

S(3)为0.7875的原因是,显然

d

i

d_i

di为1,根据

n

i

n_i

ni的定义计算的是<3分钟的数量,因此为8,所以为0.9*(8-1)/8=0.7875。

如果使用scikit-survival,则代码如下

import pandas as pd

import matplotlib.pyplot as plt

from sksurv.nonparametric import kaplan_meier_estimator

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

df["event_observed"] = df["event_observed"].astype(bool)

time, survival_prob = kaplan_meier_estimator(df["event_observed"], df["time-to-first-fill"])

plt.step(time, survival_prob, where="post")

plt.show()

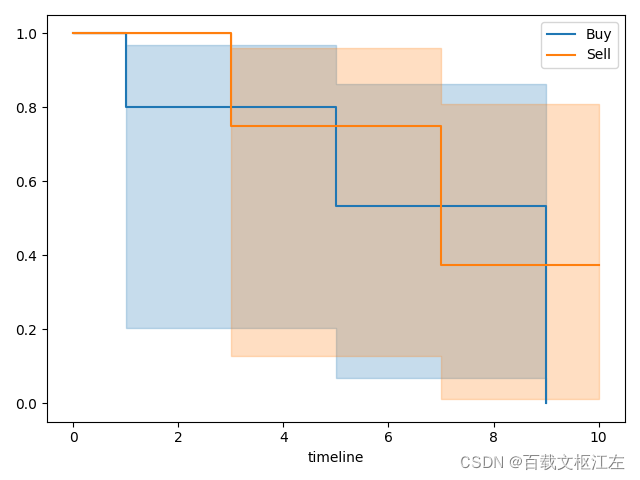

估计不同类别上的S(t)

除此之外,我们还可以引入一个变量,研究S(t)在不同变量上的表现,例如可以研究在买卖不同方向上的time-to-first-fill是否存在差异。

import pandas as pd

from lifelines import KaplanMeierFitter

import matplotlib.pyplot as plt

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

kmf = KaplanMeierFitter()

buy_side_index = (df["OrderBSFlag"] == 1)

kmf.fit(durations=df.loc[buy_side_index, "time-to-first-fill"], event_observed=df.loc[buy_side_index, "event_observed"], label="Buy")

kmf.plot_survival_function()

kmf.fit(durations=df.loc[~buy_side_index, "time-to-first-fill"], event_observed=df.loc[~buy_side_index, "event_observed"], label="Sell")

kmf.plot_survival_function()

plt.show()

log-rank检验

对上面不同买卖方向的time-to-first-fill之间是否存在差异进行检验。

import pandas as pd

from lifelines.statistics import logrank_test

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

buy_side_index = (df["OrderBSFlag"] == 1)

results = logrank_test(df.loc[buy_side_index, "time-to-first-fill"],

df.loc[~buy_side_index, "time-to-first-fill"],

event_observed_A=df.loc[buy_side_index, "event_observed"],

event_observed_B=df.loc[~buy_side_index, "event_observed"])

results.print_summary()

print(results.p_value) # 0.6547208460185768

print(results.test_statistic) # 0.2

检验结果显示p值为0.65,显然无法拒绝原假设,即实验数据中的买卖方向之间不存在差异,与从图中的观察一致。

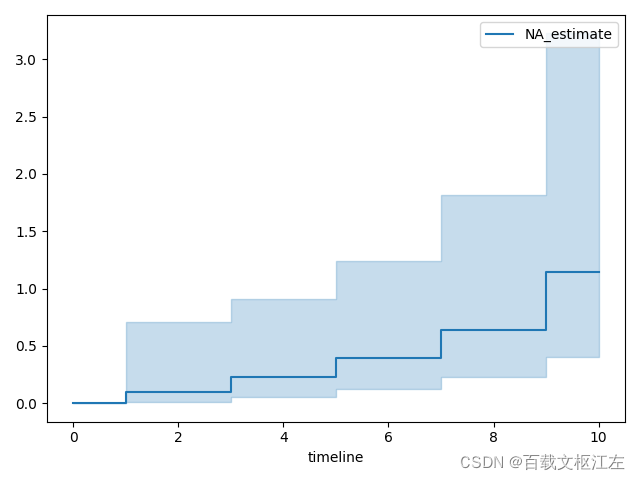

使用Nelson-Aalen估计H(t) 【非参数方法】

除了估计生存函数S(t)之外,我们还可以对hazard function即h(t),例如使用下面的公式估计h(t)的CDF即H(t)。

H

^

(

t

)

=

∑

t

i

≤

t

d

i

n

i

\hat H(t)=\sum_{t_i\leq t}\frac{d_i}{n_i}

H^(t)=ti≤t∑nidi

和KM估计中相同,

d

i

d_i

di表示在

t

i

t_i

ti时刻发生的事件数,

n

i

n_i

ni表示在

t

i

t_i

ti时刻前处于危险中的受试者数量。

from lifelines import NelsonAalenFitter

import pandas as pd

import matplotlib.pyplot as plt

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

naf = NelsonAalenFitter()

naf.fit(df["time-to-first-fill"], event_observed=df["event_observed"])

naf.plot_cumulative_hazard()

plt.show()

参数方法:Weibull、Exponential,、Log-Logistic、Log-Normal、Splines、Generalized-Gamma模型

相比于K-M和N-A中的非参数方法,我们也可以假定S(t)、H(t)所属的分布,然后用数据求出分布中的参数。

以Weibull为例,需要求解的参数是

λ

\lambda

λ和

ρ

\rho

ρ

S

(

t

)

=

e

x

p

(

−

(

t

λ

)

ρ

)

H

(

t

)

=

(

t

λ

)

ρ

S(t)=exp(-(\frac{t}{\lambda})^\rho) \\ H(t)=(\frac{t}{\lambda})^{\rho}

S(t)=exp(−(λt)ρ)H(t)=(λt)ρ

from lifelines import WeibullFitter

import pandas as pd

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

wf = WeibullFitter().fit(df["time-to-first-fill"], event_observed=df["event_observed"])

wf.print_summary()

# <lifelines.WeibullFitter:"Weibull_estimate", fitted with 10 total observations, 5 right-censored observations>

# number of observations = 10

# number of events observed = 5

# log-likelihood = -16.27

# hypothesis = lambda_ != 1, rho_ != 1

#

# ---

# coef se(coef) coef lower 95% coef upper 95% z p -log2(p)

# lambda_ 9.10 2.59 4.03 14.17 3.13 <0.005 9.16

# rho_ 1.66 0.63 0.42 2.89 1.04 0.30 1.75

# ---

# AIC = 36.54

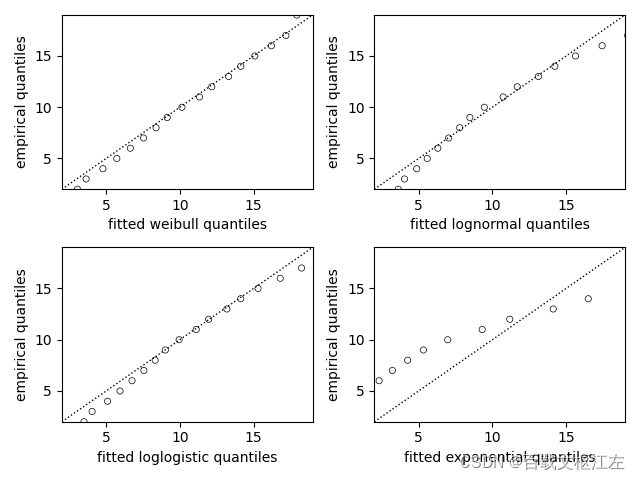

使用QQ图、Log-likehood、AIC选择模型

from lifelines import *

from lifelines.plotting import qq_plot

import pandas as pd

import matplotlib.pyplot as plt

import random

ls = [[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]]

ls = [[lss[3] + random.randint(1, 10), lss[4]] for lss in ls for _ in range(100)]

df = pd.DataFrame(ls, columns=["time-to-first-fill", "event_observed"])

fig, axes = plt.subplots(2, 2)

axes = axes.reshape(4, )

for i, model in enumerate([WeibullFitter(), LogNormalFitter(), LogLogisticFitter(), ExponentialFitter()]):

model.fit(df["time-to-first-fill"], event_observed=df["event_observed"])

print(model, model.log_likelihood_, model.AIC_)

qq_plot(model, ax=axes[i])

plt.show()

# <lifelines.WeibullFitter:"Weibull_estimate", fitted with 1000 total observations, 500 right-censored observations> -1816.1656841614129 3636.3313683228257

# <lifelines.LogNormalFitter:"LogNormal_estimate", fitted with 1000 total observations, 500 right-censored observations> -1851.521385280591 3707.042770561182

# <lifelines.LogLogisticFitter:"LogLogistic_estimate", fitted with 1000 total observations, 500 right-censored observations> -1830.8689894251984 3665.7379788503968

# <lifelines.ExponentialFitter:"Exponential_estimate", fitted with 1000 total observations, 500 right-censored observations> -2042.4664595062745 4086.932919012549

从指标上看,weibull模型更符合随机生成的数据。

生存回归模型

如果想在对S(t)建模时引入一些特征,例如限价单成交时长预测中的下单量特征,就需要使用生存回归模型。类似地,由于censor现象的存在,直接使用回归模型不合适,所以需要使用这里的生存回归模型。

Cox proportional hazard模型

Cox模型假设特征对h(t)有线性倍增效应,并且该效应随时间推移保持不变。

H

(

t

∣

x

)

=

e

x

p

(

x

T

β

)

∫

0

t

h

0

(

s

)

d

s

H(t|x)=exp(x^T\beta)\int_0^t h_0(s)ds

H(t∣x)=exp(xTβ)∫0th0(s)ds

相比于fully parametric models,Cox Proportional Hazards regression这种semi-parametric models的优点在于不需要知道或假设数据所属的分布

from lifelines import CoxPHFitter

import pandas as pd

import matplotlib.pyplot as plt

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

df = df.drop(columns=["OrderIndex"])

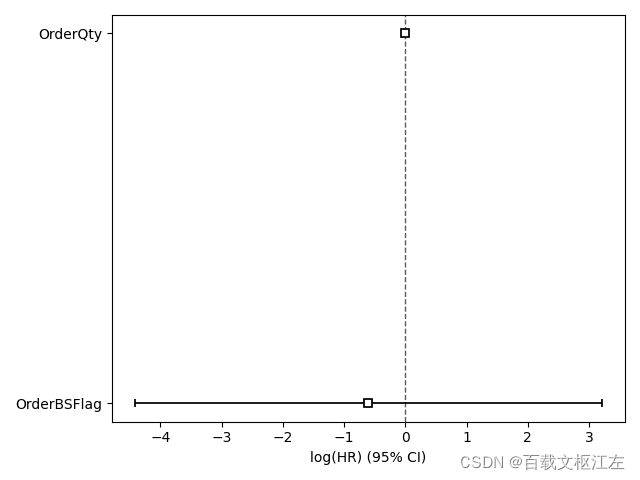

cph = CoxPHFitter()

cph.fit(df, duration_col='time-to-first-fill', event_col='event_observed')

cph.print_summary()

cph.plot()

# 测试单变量对生存曲线的影响

cph.plot_partial_effects_on_outcome(covariates='OrderBSFlag', values=[1, 2], cmap='coolwarm', plot_baseline=False)

plt.show()

# <lifelines.CoxPHFitter: fitted with 10 total observations, 5 right-censored observations>

# duration col = 'time-to-first-fill'

# event col = 'event_observed'

# baseline estimation = breslow

# number of observations = 10

# number of events observed = 5

# partial log-likelihood = -8.15

#

# ---

# coef exp(coef) se(coef) coef lower 95% coef upper 95% exp(coef) lower 95% exp(coef) upper 95%

# covariate

# OrderBSFlag -0.60 0.55 1.94 -4.41 3.21 0.01 24.66

# OrderQty -0.00 1.00 0.02 -0.04 0.04 0.96 1.04

#

# z p -log2(p)

# covariate

# OrderBSFlag -0.31 0.76 0.40

# OrderQty -0.12 0.91 0.14

# ---

# Concordance = 0.58

# Partial AIC = 20.29

# log-likelihood ratio test = 0.21 on 2 df

# -log2(p) of ll-ratio test = 0.16

Accelerated failure time模型 AFT模型

H

(

t

∣

x

)

=

(

t

e

x

p

(

x

T

β

)

)

ρ

H(t|x)=(\frac{t}{exp(x^T\beta)})^\rho

H(t∣x)=(exp(xTβ)t)ρ

lifelines中有WeibullAFTFitter接口,另外可以指定ancillary参数如为True同时对

ρ

\rho

ρ进行建模。

另外还有LogNormalAFTFitter、LogLogisticAFTFitter和 GeneralizedGammaRegressionFitter。

Aalen’s additive model

h

(

t

∣

x

)

=

b

0

(

t

)

+

b

1

(

t

)

x

1

+

.

.

.

+

b

N

(

t

)

x

N

h(t|x)=b_0(t)+b_1(t)x_1+...+b_N(t)x_N

h(t∣x)=b0(t)+b1(t)x1+...+bN(t)xN

lifelines中有AalenAdditiveFitter接口

模型保存

from lifelines.utils.sklearn_adapter import sklearn_adapter

from lifelines import CoxPHFitter

sklearn_adapter(CoxPHFitter, event_col='arrest')

from joblib import load

model = load(...)

from dill import loads, dumps

from pickle import loads, dumps

s_cph = dumps(cph)

cph_new = loads(s_cph)

cph_new.summary

s_kmf = dumps(kmf)

kmf_new = loads(s_kmf)

kmf_new.survival_function_

import pickle

with open('/path/my.pickle', 'wb') as f:

pickle.dump(cph, f) # saving my trained cph model as my.pickle

with open('/path/my.pickle', 'rb') as f:

cph_new = pickle.load(f)

cph_new.summary # should produce the same output as cph.summary

使用scikit-survival做gridsearch

相比于lifelines库,scikit-survival库提供了更多近似于scikit-learn的工具

from sksurv.linear_model import CoxPHSurvivalAnalysis

from sklearn.model_selection import GridSearchCV, KFold

import pandas as pd

pd.set_option("display.max_columns", None)

df = pd.DataFrame([[1, 1, 100, 1, 1],

[2, 2, 200, 3, 1],

[3, 1, 200, 5, 1],

[4, 2, 100, 7, 1],

[5, 1, 200, 9, 1],

[6, 2, 100, 2, 0],

[7, 1, 200, 4, 0],

[8, 2, 100, 6, 0],

[9, 1, 200, 8, 0],

[10, 2, 100, 10, 0]],

columns=["OrderIndex", "OrderBSFlag", "OrderQty", "time-to-first-fill", "event_observed"])

df["event_observed"] = df["event_observed"].astype(bool)

df = df.drop(columns=["OrderIndex"])

data_x, data_y = df[["OrderBSFlag", "OrderQty"]], df[["event_observed", "time-to-first-fill"]]

data_y = data_y.to_records(index=False)

param_grid = {'alpha': [1, 100, 1000]}

cv = KFold(n_splits=2, random_state=1, shuffle=True)

gcv = GridSearchCV(CoxPHSurvivalAnalysis(), param_grid, return_train_score=True, cv=cv)

gcv.fit(data_x, data_y)

results = pd.DataFrame(gcv.cv_results_).sort_values(by='mean_test_score', ascending=False)

results = results.loc[:, ~results.columns.str.endswith("_time")]

print(results)

# param_alpha params split0_test_score split1_test_score \

# 1 100 {'alpha': 100} 0.071429 0.5

# 2 1000 {'alpha': 1000} 0.071429 0.5

# 0 1 {'alpha': 1} 0.071429 0.0

#

# mean_test_score std_test_score rank_test_score split0_train_score \

# 1 0.285714 0.214286 1 1.0

# 2 0.285714 0.214286 1 1.0

# 0 0.035714 0.035714 3 1.0

#

# split1_train_score mean_train_score std_train_score

# 1 0.500000 0.750000 0.250000

# 2 0.500000 0.750000 0.250000

# 0 0.928571 0.964286 0.035714

基于ML的模型

随机森林

sksurv.ensemble.RandomSurvivalForest

梯度提升树 GBM

sksurv.ensemble.GradientBoostingSurvivalAnalysis sksurv.ensemble.ComponentwiseGradientBoostingSurvivalAnalysis

SVM

sksurv.svm.FastSurvivalSVM

本文的参考链接:

https://towardsdatascience.com/survival-analysis-intuition-implementation-in-python-504fde4fcf8e

https://towardsdatascience.com/hands-on-survival-analysis-with-python-270fa1e6fb41

https://lifelines.readthedocs.io/en/latest/

https://scikit-survival.readthedocs.io/en/stable/

https://square.github.io/pysurvival/

5532

5532

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言