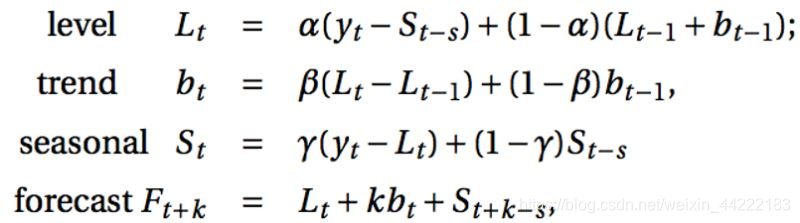

公式:

# import needed packages

#-----------------------

import math

import numpy as np

import pandas as pd

from sklearn import linear_model

from scipy.optimize import fmin_l_bfgs_b

# bring in the passenger data from HW4 to test the function against R output

#---------------------------------------------------------------------------

tsA=[12.7, 14.2, 9.6, 9.2, 10.3, 9.3, 7.8, 7.7, 7.4, 6.9, 6.7, 6.9, 6.6]

# define main function [holtWinters] to generate retrospective smoothing/predictions

#-----------------------------------------------------------------------------------

def holtWinters(ts, p, sp, ahead, mtype, alpha = None, beta = None, gamma = None):

'''HoltWinters retrospective smoothing & future period prediction algorithm

both the additive and multiplicative methods are implemented and the (alpha, beta, gamma)

parameters have to be either all user chosen or all optimized via one-step-ahead prediction MSD

initial (a, b, s) parameter values are calculated with a fixed-period seasonal decomposition and a

simple linear regression to estimate the initial level (B0) and initial trend (B1) values

@params:

- ts[list]: time series of data to model

- p[int]: period of the time series (for the calculation of seasonal effects)

- sp[int]: number of starting periods to use when calculating initial parameter values

- ahead[int]: number of future periods for which predictions will be generated

- mtype[string]: which method to use for smoothing/forecasts ['additive'/'multiplicative']

- alpha[float]: user-specified level forgetting factor (one-step MSD optimized if None)

- beta[float]: user-specified slope forgetting factor (one-step MSD optimized if None)

- gamma[float]: user-specified season forgetting factor (one-step MSD optimized if None)

@return:

- alpha[float]: chosen/optimal level forgetting factor used in calculations

- beta[float]: chosen/optimal trend forgetting factor used in calculations

- gamma[float]: chosen/optimal season forgetting factor used in calculations

- MSD[float]: chosen/optimal Mean Square Deviation with respect to one-step-ahead predictions

- params[tuple]: final (a, b, s) parameter values used for the prediction of future observations

- smoothed[list]: smoothed values (level + trend + seasonal) for the original time series

- predicted[list]: predicted values for the next @ahead periods of the time series

sample calls:

results = holtWinters(ts, 12, 4, 24, 'additive')

results = holtWinters(ts, 12, 4, 24, 'multiplicative', alpha = 0.1, beta = 0.2, gamma = 0.3)'''

a, b, s = _initValues(mtype, ts, p, sp)

if alpha == None or beta == None or gamma == None:

ituning = [0.1, 0.1, 0.1]

ibounds = [(0,1), (0,1), (0,1)]

optimized = fmin_l_bfgs_b(_MSD, ituning, args = (mtype, ts, p, a, b, s[:]), bounds = ibounds, approx_grad = True)

alpha, beta, gamma = optimized[0]

MSD, params, smoothed = _expSmooth(mtype, ts, p, a, b, s[:], alpha, beta, gamma)

predicted = _predictValues(mtype, p, ahead, params)

return {'alpha': alpha, 'beta': beta, 'gamma': gamma, 'MSD': MSD, 'params': params, 'smoothed': smoothed, 'predicted': predicted}

def _initValues(mtype, ts, p, sp):

'''subroutine to calculate initial parameter values (a, b, s) based on a fixed number of starting periods'''

initSeries = pd.Series(ts[:p*sp])

if mtype == 'additive':

# print(p)

rawSeason = initSeries - initSeries.rolling(window = p, min_periods = p, center = True).mean()

initSeason = [np.nanmean(rawSeason[i::p]) for i in range(p)]

initSeason = pd.Series(initSeason) - np.mean(initSeason)

deSeasoned = [initSeries[v] - initSeason[v % p] for v in range(len(initSeries))]

else:

rawSeason = initSeries / initSeries.rolling(window = p, min_periods = p, center = True).mean()

initSeason = [np.nanmean(rawSeason[i::p]) for i in range(p)]

initSeason = pd.Series(initSeason) / math.pow(np.prod(np.array(initSeason)), 1/p)

deSeasoned = [initSeries[v] / initSeason[v % p] for v in range(len(initSeries))]

lm = linear_model.LinearRegression()

lm.fit(pd.DataFrame({'time': [t+1 for t in range(len(initSeries))]}), pd.Series(deSeasoned))

return float(lm.intercept_), float(lm.coef_), list(initSeason)

def _MSD(tuning, *args):

'''subroutine to pass to BFGS optimization to determine the optimal (alpha, beta, gamma) values'''

predicted = []

mtype = args[0]

ts, p = args[1:3]

Lt1, Tt1 = args[3:5]

St1 = args[5][:]

alpha, beta, gamma = tuning[:]

for t in range(len(ts)):

if mtype == 'additive':

Lt = alpha * (ts[t] - St1[t % p]) + (1 - alpha) * (Lt1 + Tt1)

Tt = beta * (Lt - Lt1) + (1 - beta) * (Tt1)

St = gamma * (ts[t] - Lt) + (1 - gamma) * (St1[t % p])

predicted.append(Lt1 + Tt1 + St1[t % p])

else:

Lt = alpha * (ts[t] / St1[t % p]) + (1 - alpha) * (Lt1 + Tt1)

Tt = beta * (Lt - Lt1) + (1 - beta) * (Tt1)

St = gamma * (ts[t] / Lt) + (1 - gamma) * (St1[t % p])

predicted.append((Lt1 + Tt1) * St1[t % p])

Lt1, Tt1, St1[t % p] = Lt, Tt, St

return sum([(ts[t] - predicted[t])**2 for t in range(len(predicted))])/len(predicted)

def _expSmooth(mtype, ts, p, a, b, s, alpha, beta, gamma):

'''subroutine to calculate the retrospective smoothed values and final parameter values for prediction'''

smoothed = []

Lt1, Tt1, St1 = a, b, s[:]

for t in range(len(ts)):

if mtype == 'additive':

Lt = alpha * (ts[t] - St1[t % p]) + (1 - alpha) * (Lt1 + Tt1)

Tt = beta * (Lt - Lt1) + (1 - beta) * (Tt1)

St = gamma * (ts[t] - Lt) + (1 - gamma) * (St1[t % p])

smoothed.append(Lt1 + Tt1 + St1[t % p])

else:

Lt = alpha * (ts[t] / St1[t % p]) + (1 - alpha) * (Lt1 + Tt1)

Tt = beta * (Lt - Lt1) + (1 - beta) * (Tt1)

St = gamma * (ts[t] / Lt) + (1 - gamma) * (St1[t % p])

smoothed.append((Lt1 + Tt1) * St1[t % p])

Lt1, Tt1, St1[t % p] = Lt, Tt, St

MSD = sum([(ts[t] - smoothed[t])**2 for t in range(len(smoothed))])/len(smoothed)

return MSD, (Lt1, Tt1, St1), smoothed

def _predictValues(mtype, p, ahead, params):

'''subroutine to generate predicted values @ahead periods into the future'''

Lt, Tt, St = params

if mtype == 'additive':

return [Lt + (t+1)*Tt + St[t % p] for t in range(ahead)]

else:

return [(Lt + (t+1)*Tt) * St[t % p] for t in range(ahead)]

# print out the results to check against R output

#------------------------------------------------

results = holtWinters(tsA, 4, 4, 5, mtype = 'additive')

# # results = holtWinters(tsA, 12, 4, 24, mtype = 'multiplicative')

print("TUNING: ", results['alpha'], results['beta'], results['gamma'], results['MSD'])

# # print('----')

print("FINAL PARAMETERS: ", results['params'])

print("PREDICTED VALUES: ", results['predicted'])

1万+

1万+

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言