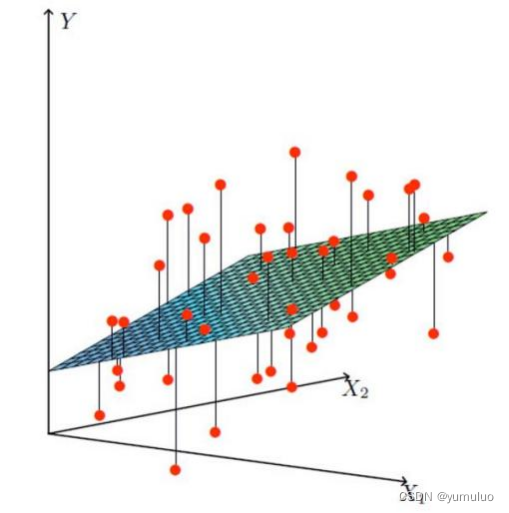

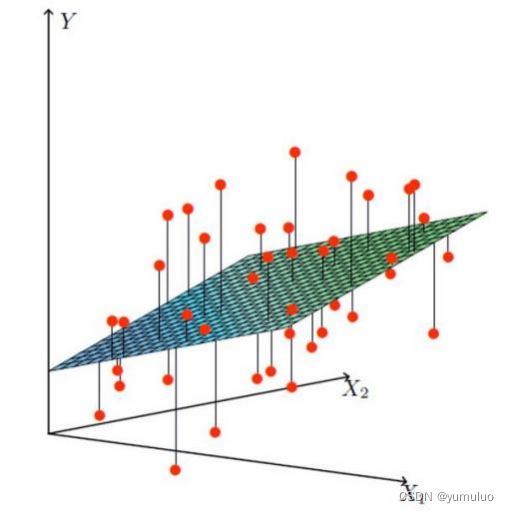

(一)通俗解释:

①X1,X2就是我们的两个特征(年龄,工资)

Y是银行最终会借给我们多少钱

②找到最合适的一条线(想象一个高维)来,最好的拟合我们的数据点

(二) 数学来了:

1.假设θ1是年龄的参数,θ2是工资的参数

2.拟合的平面:(θ0是偏置顶)

3.整合:

(三)误差:

1.真实值和预测值之间肯定是要存在差异的

(用 来表示该误差)

2.对于每个样本

(四)误差:

1.预测值与误差:

2.由于误差服从高斯分布:

3.合并二式:

附上代码:

import numpy as np

from utils.features import prepare_for_training

class LinearRegression:

def __init__(self,data,labels,polynomial_degree = 0,sinusoid_degree = 0,normalize_data=True):

"""

1.对数据进行预处理操作

2.先得到所有的特征个数

3.初始化参数矩阵

"""

(data_processed,

features_mean,

features_deviation) = prepare_for_training(data, polynomial_degree, sinusoid_degree,normalize_data=True)

self.data = data_processed

self.labels = labels

self.features_mean = features_mean

self.features_deviation = features_deviation

self.polynomial_degree = polynomial_degree

self.sinusoid_degree = sinusoid_degree

self.normalize_data = normalize_data

num_features = self.data.shape[1]

self.theta = np.zeros((num_features,1))

def train(self,alpha,num_iterations = 500):

"""

训练模块,执行梯度下降

"""

cost_history = self.gradient_descent(alpha,num_iterations)

return self.theta,cost_history

def gradient_descent(self,alpha,num_iterations):

"""

实际迭代模块,会迭代num_iterations次

"""

cost_history = []

for _ in range(num_iterations):

self.gradient_step(alpha)

cost_history.append(self.cost_function(self.data,self.labels))

return cost_history

def gradient_step(self,alpha):

"""

梯度下降参数更新计算方法,注意是矩阵运算

"""

num_examples = self.data.shape[0]

prediction = LinearRegression.hypothesis(self.data,self.theta)

delta = prediction - self.labels

theta = self.theta

theta = theta - alpha*(1/num_examples)*(np.dot(delta.T,self.data)).T

self.theta = theta

def cost_function(self,data,labels):

"""

损失计算方法

"""

num_examples = data.shape[0]

delta = LinearRegression.hypothesis(self.data,self.theta) - labels

cost = (1/2)*np.dot(delta.T,delta)/num_examples

return cost[0][0]

@staticmethod

def hypothesis(data,theta):

predictions = np.dot(data,theta)

return predictions

def get_cost(self,data,labels):

data_processed = prepare_for_training(data,

self.polynomial_degree,

self.sinusoid_degree,

self.normalize_data

)[0]

return self.cost_function(data_processed,labels)

def predict(self,data):

"""

用训练的参数模型,与预测得到回归值结果

"""

data_processed = prepare_for_training(data,

self.polynomial_degree,

self.sinusoid_degree,

self.normalize_data

)[0]

predictions = LinearRegression.hypothesis(data_processed,self.theta)

return predictions

1715

1715

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言