超级会员免费看

超级会员免费看

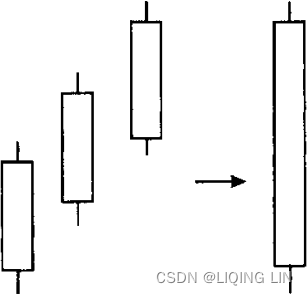

Three White Soldiers

The Three White Soldiers pattern reduces to a very bullish long white candle line. This breakdown is in full support of the pattern, which makes confirmation unnecessary.

The Three White Soldiers pattern reduces to a very bullish long white candle line. This breakdown is in full support of the pattern, which makes confirmation unnecessary.

Behavior and Rank

- Theoretical: Bullish reversal.

- Actual bull market: Bullish reversal 82% of the time (ranking 3).

- Actual bear market: Bullish reversal 84% of the time (ranking 3).

- Frequency: 67th out of 103.

- Overall performance

订阅专栏 解锁全文

订阅专栏 解锁全文

2503

2503

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言