【数据】【自动化交易】Python编写策略模拟股票交易

这节我就用上节提到的pyalgotrade来编写回测策略程序,模拟股票交易。本篇文章里用的是SMA均线策略。

数据

数据我使用的是 大恒科技(600288.SH) 2010年到2016年的day级数据,我将其变换成了pyalgotrade教程的格式:

Adj. Close,Adj. High,Adj. Low,Adj. Open,Adj. Volume,Close,Date,Ex-Dividend,High,Low,Open,Split Ratio,Volume

0,13.53,13.45,12.65,12.62,51597046.82,11.16,2010-01-04,572108102.0,11.37,10.62,10.76,1.0,51597044.0

1,13.64,13.72,12.91,12.92,48822968.82,11.27,2010-01-05,549279336.0,11.64,10.86,11.06,1.0,48822966.0

2,13.38,13.56,13.05,13.07,41360141.82,11.01,2010-01-06,461521697.0,11.48,11.02,11.21,1.0,41360139.0

... ...

简单交易程序

简单的策略程序:

# -*-coding:utf-8-*-

from __future__ import print_function

from pyalgotrade import strategy

from pyalgotrade.barfeed import quandlfeed

from pyalgotrade.technical import ma

class MyStrategy(strategy.BacktestingStrategy):

def __init__(self, feed, instrument, smaPeriod):

super(MyStrategy, self).__init__(feed, 1000)

self.__position = None

self.__instrument = instrument

# We'll use adjusted close values instead of regular close values.

self.setUseAdjustedValues(True)

self.__sma = ma.SMA(feed[instrument].getPriceDataSeries(), smaPeriod)

#---- BUY ----

def onEnterOk(self, position):

execInfo = position.getEntryOrder().getExecutionInfo()

#self.info("BUY at $%.2f" % (execInfo.getPrice()))

self.info("在价格 ¥%.2f 时买入" % (execInfo.getPrice()));

#---- NO BUY ----

def onEnterCanceled(self, position):

self.__position = None

#---- SELL ----

def onExitOk(self, position):

execInfo = position.getExitOrder().getExecutionInfo()

#self.info("SELL at $%.2f" % (execInfo.getPrice()))

self.info("在价格 ¥%.2f 时抛出" % (execInfo.getPrice()));

self.__position = None

#---- NO SELL ----

def onExitCanceled(self, position):

# If the exit was canceled, re-submit it.

self.__position.exitMarket()

def onBars(self, bars):

# Wait for enough bars to be available to calculate a SMA.

if self.__sma[-1] is None:

return

bar = bars[self.__instrument]

# If a position was not opened, check if we should enter a long position.

if self.__position is None:

if bar.getPrice() > self.__sma[-1]:

# Enter a buy market order for 10 shares. The order is good till canceled.

self.__position = self.enterLong(self.__instrument, 10, True)

# Check if we have to exit the position.

elif bar.getPrice() < self.__sma[-1] and not self.__position.exitActive():

self.__position.exitMarket()

def run_strategy(smaPeriod):

# Load the bar feed from the CSV file

feed = quandlfeed.Feed()

feed.addBarsFromCSV("orcl", "600288SH.csv")

# Evaluate the strategy with the feed.

myStrategy = MyStrategy(feed, "orcl", smaPeriod)

myStrategy.run()

#print("Final portfolio value: $%.2f" % myStrategy.getBroker().getEquity())

print("最终盈亏情况: ¥ %.2f" % myStrategy.getBroker().getEquity())

run_strategy(15);

输出结果:

... ...

2016-06-22 00:00:00 strategy [INFO] 在价格 ¥14.62 时抛出

2016-06-23 00:00:00 strategy [INFO] 在价格 ¥14.94 时买入

2016-06-27 00:00:00 strategy [INFO] 在价格 ¥14.68 时抛出

2016-06-28 00:00:00 strategy [INFO] 在价格 ¥14.95 时买入

2016-07-19 00:00:00 strategy [INFO] 在价格 ¥15.35 时抛出

2016-07-20 00:00:00 strategy [INFO] 在价格 ¥15.34 时买入

2016-07-28 00:00:00 strategy [INFO] 在价格 ¥15.12 时抛出

2016-08-11 00:00:00 strategy [INFO] 在价格 ¥15.88 时买入

2016-08-26 00:00:00 strategy [INFO] 在价格 ¥15.58 时抛出

最终盈亏情况: ¥ 925.78

策略和绘制曲线程序:

# -*-coding:utf-8-*-

from pyalgotrade import strategy

from pyalgotrade.technical import ma

from pyalgotrade.technical import cross

from pyalgotrade import plotter

from pyalgotrade.barfeed import quandlfeed

from pyalgotrade.stratanalyzer import returns

class SMACrossOver(strategy.BacktestingStrategy):

def __init__(self, feed, instrument, smaPeriod):

super(SMACrossOver, self).__init__(feed)

self.__instrument = instrument

self.__position = None

# We'll use adjusted close values instead of regular close values.

self.setUseAdjustedValues(True)

self.__prices = feed[instrument].getPriceDataSeries()

self.__sma = ma.SMA(self.__prices, smaPeriod)

def getSMA(self):

return self.__sma

def onEnterCanceled(self, position):

self.__position = None

def onExitOk(self, position):

self.__position = None

def onExitCanceled(self, position):

# If the exit was canceled, re-submit it.

self.__position.exitMarket()

def onBars(self, bars):

# If a position was not opened, check if we should enter a long position.

if self.__position is None:

if cross.cross_above(self.__prices, self.__sma) > 0:

shares = int(self.getBroker().getCash() * 0.9 / bars[self.__instrument].getPrice())

# Enter a buy market order. The order is good till canceled.

self.__position = self.enterLong(self.__instrument, shares, True)

# Check if we have to exit the position.

elif not self.__position.exitActive() and cross.cross_below(self.__prices, self.__sma) > 0:

self.__position.exitMarket()

# Load the bar feed from the CSV file

feed = quandlfeed.Feed()

#feed.addBarsFromCSV("orcl", "WIKI-ORCL-2000-quandl.csv")

feed.addBarsFromCSV("600288SH", "600288SH.csv")

# Evaluate the strategy with the feed's bars.

myStrategy = sma_crossover.SMACrossOver(feed, "600288SH", 20)

# Attach a returns analyzers to the strategy.

returnsAnalyzer = returns.Returns()

myStrategy.attachAnalyzer(returnsAnalyzer)

# Attach the plotter to the strategy.

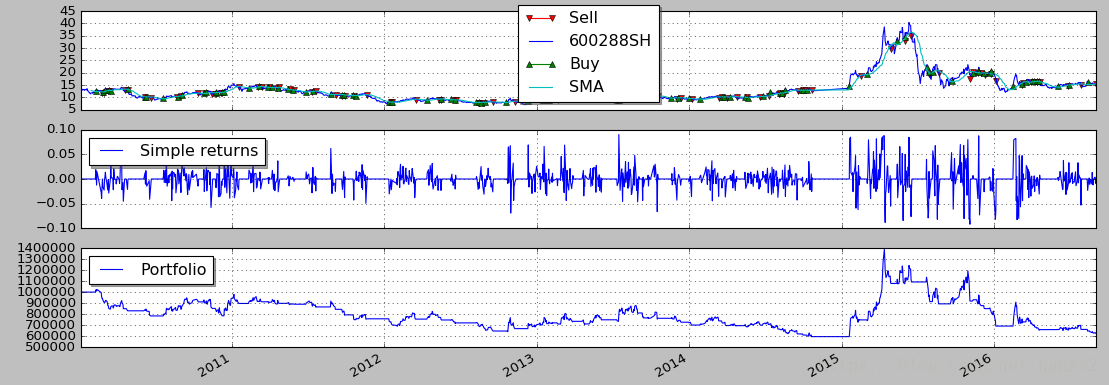

plt = plotter.StrategyPlotter(myStrategy)

# Include the SMA in the instrument's subplot to get it displayed along with the closing prices.

plt.getInstrumentSubplot("600288SH").addDataSeries("SMA", myStrategy.getSMA())

# Plot the simple returns on each bar.

plt.getOrCreateSubplot("returns").addDataSeries("Simple returns", returnsAnalyzer.getReturns())

# Run the strategy.

myStrategy.run()

myStrategy.info("Final portfolio value: $%.2f" % myStrategy.getResult())

# Plot the strategy.

plt.plot()

518

518

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言