机器学习实战–信用卡欺诈检测项目

学校大三校企合作的课程设计项目

一、任务基础

拿到的信用卡数据集是由欧洲人于2013年9月使用信用卡进行交易的数据。此数据集显示两天内发生的交易,其中284807笔交易中有492笔被盗刷。特征’Class’是响应变量,如果发生被盗刷,则取值1,否则为0。

项目的目的是完成数据集中正常交易数据和异常交易数据的分类,并对测试数据进行预测。

数据集链接:https://pan.baidu.com/s/1Gt7F9pszGNX_pm_75YSO8w

提取码:9tp6

二、数据分析与挖掘处理

导入一些库后,先读取数据再查看分析数据

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

plt.rcParams['font.sans-serif']=['SimHei']

plt.rcParams['axes.unicode_minus']=False

data = pd.read_csv('creditcard.csv')

count_classes = pd.value_counts(data['Class'], sort=True).sort_index()

count_classes.plot(kind='bar',fc = 'r')

plt.title("class 类别统计")

plt.xlabel("Class")

plt.ylabel("个数")

print(count_classes)

x = 0,1

for x, count_classes in zip(x, count_classes):

plt.text(x, count_classes , '%.2f' % count_classes, ha='center', va='bottom')

因为Amount这列的数据浮动太大,在做机器学习的过程中,需要保证特征值差异不能过大,于是我对Amount进行标准化数据。

# 预处理 标准化数据

from sklearn.preprocessing import StandardScaler

data['normAmount'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1, 1))

data = data.drop(['Time', 'Amount'], axis=1)

data.head()

特征V1,V2,… V28是使用PCA降维获得的特征数据,没有用PCA转换的唯一特征是“Class”和“Amount”。特征’Time’包含数据集中每个刷卡时间和第一次刷卡时间之间经过的秒数,对于此次项目用处不大所以去掉。

对于数据不平衡有两种方法处理:下采样和过采样。

下采样:一组数据,比如我们这个项目的数据,它的y-label(要预测的)中,0的数据多,1的数据少,我们把多的数据通过随机取到和少的一样多。

过采样:比如我们这个项目的数据,对1的数据进行生成数列,让生成的数据与0的数据一样多。通常有SMOTE算法实现。

我们这里用下采样试试效果。

#导入使用标准化的包

from sklearn.preprocessing import StandardScaler

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

data = pd.read_csv('creditcard.csv')

#reshape(行,列),指定列数,那么行数可以用-1替代,计算机会帮我们又多少行,反之亦然。

# -1 正整数通配符, 它代表任何整数。

reshape = data["Amount"].values.reshape(-1, 1)

# print(reshape)

# print(type(reshape))

#把数据按标准正太分布的方式转换均值为0,方差为1的数据

data['normAmount'] = StandardScaler().fit_transform(reshape)

#drop() 删除数据

#参数1,要删除的特征列

#参数2 ,axis,指定删除行还是列, 0 代表行, 1 代表列

data = data.drop(['Time', 'Amount'], axis=1)

# print(data.head(8))

#x拿到非Class的特征数据

#y拿到Class的特征数据

X = data.loc[:, data.columns != "Class"]

Y = data.loc[:, data.columns == "Class"]

# 计算少数类别的样本有多少

number_records_fraud = len(data[data.Class == 1])

#求出少数类别样本对应的索引值。

fraud_indices = np.array(data[data.Class == 1].index)

#求出多数类别样本对应的索引值

normal_indices = np.array(data[data.Class == 0].index)

# print(number_records_fraud)

# print(fraud_indices)

# print(normal_indices)

#从多数类别的样本索引normal_indices中随机筛选number_records_fraud个

#参数1 a 样本集

#参数2 选择多少

#参数3 replace 是否替换原来的数据

random_normal_indices = np.random.choice(normal_indices,

size=number_records_fraud,

replace=False)

# print(len(random_normal_indices)) #492

#把random_normal_indices 和 fraud_indices混合起来作为后面undersampled的学习样本

#a_tuple 元组, 要整合的所有的数据

# 参数2 axis 整合的方向,

under_sample_indices = np.concatenate((random_normal_indices, fraud_indices),

axis=0)

# print(len(under_sample_indices)) #984

#iloc根据索引得到数据。

under_sample_data = data.iloc[under_sample_indices, :]

# print(under_sample_data.head(8))

# print(len(under_sample_data)) #984

#用X_undersampled从undersample样本数据中拿到非Class特征

X_undersampled = under_sample_data.iloc[:,data.columns != "Class"]

# print(X_undersampled.head())

# 用Y_undersampled从undersample样本中拿到class特性

Y_undersampled = under_sample_data.iloc[:, data.columns == "Class"]

# 汇总

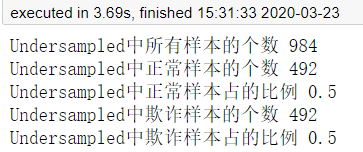

print("Undersampled中所有样本的个数", len(under_sample_data))

print("Undersampled中正常样本的个数", len(random_normal_indices))

print("Undersampled中正常样本占的比例", len(random_normal_indices)/len(under_sample_data))

print("Undersampled中欺诈样本的个数",len(fraud_indices))

print("Undersampled中欺诈样本占的比例",len(fraud_indices)/len(under_sample_data))

我们可以看到下采样后1和0的数据数量比例一样都是0.5。

下面对数据进行切分,用来训练和测试,这里用sklearn库模型的train_test_split,顺便把没有经过下采样的原始数据也切分。

#----------------------UnderSample数据进行划分------------------------------

from sklearn.model_selection import train_test_split

#参数1 所要划分的样本的特征集

#参数2 所要划分的样本的结果集

#参数3 test_size 测试集占所有样本的比例

#参数4 random_state 划分结果是否随机

# 0 每次划分的结果都不同

# 1 每次划分的结果都相同

#返回值1 特征的训练集 +验证集

#返回值2 特征的测试集

#返回值3 结果的测试集 + 验证集

#返回值4 结果的测试集

X_train_undersample,X_test_undersamples,Y_train_undersample,Y_test_undersample=train_test_split(X_undersampled,Y_undersampled,test_size=0.3,random_state=0)

# print(X_train_undersample)

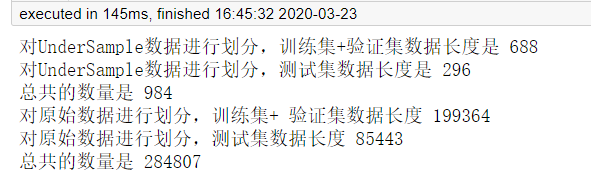

print("对UnderSample数据进行划分,训练集+验证集数据长度是 {}".format(len(Y_train_undersample))) #688

print("对UnderSample数据进行划分,测试集数据长度是 {}".format(len(Y_test_undersample))) #296

print("总共的数量是", len(Y_test_undersample) + len(Y_train_undersample))

#----------------对原始数据进行划分------------------

X_train, X_test, Y_train, Y_test = train_test_split(X, Y, test_size=0.3, random_state=0)

print('对原始数据进行划分,训练集+ 验证集数据长度',len(Y_train))

print('对原始数据进行划分,测试集数据长度',len(Y_test))

print('总共的数量是', len(Y_train) + len(Y_test))

三、选模型进行训练和预测

一般二分类项目都会先用逻辑斯特回归试试水,这里也不例外,不过我用了交叉验证找出LR的最佳参数,这里用recall召回率(查全率)评价。

from sklearn.linear_model import LogisticRegression # 使用逻辑斯特回归模型

from sklearn.model_selection import KFold, cross_val_score # fold:折叠 KFold 表示切分成几分数据进行交叉验证

from sklearn.metrics import confusion_matrix, recall_score, classification_report

def printing_Kfold_scores(x_train_data,y_train_data):

fold = KFold(5,shuffle=False)

c_param_range = [0.01,0.1,1,10,100]

result_table = pd.DataFrame(index=range(len(c_param_range),2),columns=['C_parameter','Mean recall score'])

result_table['C_parameter'] = c_param_range

j=0 # 循环找到最好的惩罚力度

for c_param in c_param_range:

print('-------------------------------------------')

print('C parameter:',c_param)

print('-------------------------------------------')

print('')

recall_accs = []

for iteration,indices in enumerate(fold.split(x_train_data)):

# 使用特定的C参数调用逻辑回归模型

# 参数 solver=’liblinear’ 消除警告

# 出现警告:模型未能收敛 ,请增加收敛次数

# 增加参数 max_iter 默认1000

lr = LogisticRegression(C = c_param, penalty='l1', solver='liblinear',max_iter=10000)

lr.fit(x_train_data.iloc[indices[0],:],y_train_data.iloc[indices[0],:].values.ravel())

y_pred_undersample = lr.predict(x_train_data.iloc[indices[1],:].values)

recall_acc = recall_score(y_train_data.iloc[indices[1],:].values,y_pred_undersample)

recall_accs.append(recall_acc)

print('Iteration ',iteration,': recall score = ',recall_acc)

result_table.loc[j,'Mean recall score'] = np.mean(recall_accs)

j += 1

print('')

print('Mean recall score ',np.mean(recall_accs))

print('')

best_c = result_table.loc[result_table['Mean recall score'].astype('float64').idxmax()]['C_parameter']

print('*********************************************************************************')

print('Best model to choose from cross validation is with C parameter',best_c)

print('*********************************************************************************')

return best_c

best_c = printing_Kfold_scores(X_train_undersample,Y_train_undersample)

from sklearn.metrics import classification_report

lr = LogisticRegression(C = best_c, penalty='l1', solver='liblinear',max_iter=10000)

lr.fit(X_train_undersample, Y_train_undersample)

lr_y_pred = lr.predict(X_test_undersamples)

# 输出逻辑斯特在测试集上的分类准确性,以及更加详细的精确率、召回率、F1指标。

print('The accuracy of lr classifier is', lr.score(X_test_undersamples, Y_test_undersample))

print(classification_report(lr_y_pred, Y_test_undersample))

下面我用没有进行下采样的原始数据也用相同模型训练看看准确率。

#原始数据

lr.fit(X_train, Y_train)

lr_y_pred = lr.predict(X_test)

# 输出逻辑斯特在测试集上的分类准确性,以及更加详细的精确率、召回率、F1指标。

print('The accuracy of lr classifier is', lr.score(X_test, Y_test))

print(classification_report(lr_y_pred, Y_test))

结果发现原始数据准确率更高,简单分析发现应该是采用的下采样数据集,数据利用率太低,但是实战的话数据不平衡对刚开始的建模结果不是很好。

四、总结

这次项目对我帮助较多的是:① 数据不平衡处理 ② 交叉验证取最佳参数

对项目我也再参考了网上其他人的做法,发现挺多不错的文章。其中“|旧市拾荒|”的博客我学到挺多,也发现授课老师也是参考ta的文章教。

这是他的文章链接:https://www.cnblogs.com/xiaoyh/p/11194053.html

4033

4033

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言