从金融时间序列的角度,以 沪深 300的收益作为研究标的,使用GARCH等衍生模型进行探讨和对比,并尝试对价格和波动率进行一定的拟合和预测。

金融时间序列(二)

作者:邱吉尔

1. 输入库包

In [1]:

from scipy import stats

import statsmodels.api as sm

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

plt.style.use('seaborn')

import arch2. 取出数据

In [2]:

HS300_close=get_price(['000300.SH'], '20151125', '20190125', '1d', ['close'], True, None,is_panel=1)['close']

HS300_close.columns=['HS300_close']

HS300_close['return']=HS300_close['HS300_close'].pct_change()

HS300_close.dropna(inplace=True)

datetime=pd.to_datetime(HS300_close.index)

fig,ax=plt.subplots(figsize=(20,8))

rect1=ax.plot(datetime,HS300_close['return'],color='IndianRed')

ax.set_ylabel('HS300 Return',size=15)

ax=ax.twinx()

rect2=ax.plot(datetime,HS300_close['HS300_close'])

ax.set_ylabel('HS300 Close',size=15)

plt.title('HS300',size=25)Out[2]:

<matplotlib.text.Text at 0x7fca33a75f60>

3. GARCH 模型

对于一个对数收益率序列rt,令:

如果at满足以下式子:

则称at服从GARCH模型,其中,{ϵt} 是均值为0,方差为1的独立同分布随机变量序列.

1. 数据集分类,GARCH模型拟合

In [142]:

train_GARCH =HS300_close['return'][:-30]

test_GARCH = HS300_close['return'][-30:]

am_GARCH = arch.arch_model(train_GARCH, mean='AR', lags=14, vol='GARCH')

res_GARCH = am_GARCH.fit()Iteration: 1, Func. Count: 20, Neg. LLF: -2322.719676744772

Iteration: 2, Func. Count: 48, Neg. LLF: -2324.118636827964

Iteration: 3, Func. Count: 78, Neg. LLF: -2323.6843401398555

Iteration: 4, Func. Count: 108, Neg. LLF: -2324.1246848237706

Iteration: 5, Func. Count: 133, Neg. LLF: -2324.1264594013755

Iteration: 6, Func. Count: 163, Neg. LLF: -2316.849320551835

Iteration: 7, Func. Count: 193, Neg. LLF: -2328.0083395660868

Iteration: 8, Func. Count: 223, Neg. LLF: -2327.4637810024988

Iteration: 9, Func. Count: 251, Neg. LLF: -2328.0231532432426

Iteration: 10, Func. Count: 281, Neg. LLF: -2325.763855473391

Iteration: 11, Func. Count: 311, Neg. LLF: -2328.0188277867

Iteration: 12, Func. Count: 338, Neg. LLF: -2328.024075604725

Positive directional derivative for linesearch (Exit mode 8)

Current function value: -2328.024084172148

Iterations: 16

Function evaluations: 338

Gradient evaluations: 12

/opt/conda/lib/python3.5/site-packages/arch/univariate/base.py:517: ConvergenceWarning: The optimizer returned code 8. The message is: Positive directional derivative for linesearch See scipy.optimize.fmin_slsqp for code meaning. ConvergenceWarning)

In [15]:

res_GARCH.summary()Out[15]:

| Dep. Variable: | return | R-squared: | 0.071 |

|---|---|---|---|

| Mean Model: | AR | Adj. R-squared: | 0.053 |

| Vol Model: | GARCH | Log-Likelihood: | 2328.02 |

| Distribution: | Normal | AIC: | -4620.05 |

| Method: | Maximum Likelihood | BIC: | -4537.35 |

| No. Observations: | 731 | ||

| Date: | Tue, Feb 12 2019 | Df Residuals: | 713 |

| Time: | 10:13:35 | Df Model: | 18 |

| coef | std err | t | P>|t| | 95.0% Conf. Int. | |

|---|---|---|---|---|---|

| Const | 4.3118e-04 | 3.001e-04 | 1.437 | 0.151 | [-1.570e-04,1.019e-03] |

| return[1] | -0.0426 | 3.569e-02 | -1.193 | 0.233 | [ -0.113,2.737e-02] |

| return[2] | 0.0299 | 3.594e-02 | 0.832 | 0.406 | [-4.054e-02, 0.100] |

| return[3] | 0.0652 | 4.003e-02 | 1.628 | 0.103 | [-1.327e-02, 0.144] |

| return[4] | -0.0582 | 3.710e-02 | -1.568 | 0.117 | [ -0.131,1.454e-02] |

| return[5] | -0.0575 | 3.989e-02 | -1.441 | 0.150 | [ -0.136,2.072e-02] |

| return[6] | -0.0528 | 3.239e-02 | -1.631 | 0.103 | [ -0.116,1.066e-02] |

| return[7] | 0.0393 | 3.921e-02 | 1.002 | 0.316 | [-3.756e-02, 0.116] |

| return[8] | -0.0306 | 3.370e-02 | -0.908 | 0.364 | [-9.665e-02,3.545e-02] |

| return[9] | 0.0874 | 3.520e-02 | 2.484 | 1.298e-02 | [1.845e-02, 0.156] |

| return[10] | -7.3447e-03 | 3.654e-02 | -0.201 | 0.841 | [-7.897e-02,6.428e-02] |

| return[11] | 0.0228 | 3.433e-02 | 0.664 | 0.507 | [-4.448e-02,9.008e-02] |

| return[12] | -0.0516 | 3.641e-02 | -1.418 | 0.156 | [ -0.123,1.972e-02] |

| return[13] | 0.0646 | 3.598e-02 | 1.796 | 7.250e-02 | [-5.901e-03, 0.135] |

| return[14] | -0.1405 | 3.224e-02 | -4.356 | 1.323e-05 | [ -0.204,-7.727e-02] |

| coef | std err | t | P>|t| | 95.0% Conf. Int. | |

|---|---|---|---|---|---|

| omega | 2.6238e-06 | 4.121e-12 | 6.367e+05 | 0.000 | [2.624e-06,2.624e-06] |

| alpha[1] | 0.0500 | 1.510e-02 | 3.312 | 9.261e-04 | [2.042e-02,7.960e-02] |

| beta[1] | 0.9300 | 1.063e-02 | 87.477 | 0.000 | [ 0.909, 0.951] |

In [16]:

res_GARCH.paramsOut[16]:

Const 0.000431 return[1] -0.042592 return[2] 0.029893 return[3] 0.065190 return[4] -0.058172 return[5] -0.057475 return[6] -0.052824 return[7] 0.039286 return[8] -0.030600 return[9] 0.087443 return[10] -0.007345 return[11] 0.022798 return[12] -0.051641 return[13] 0.064623 return[14] -0.140464 omega 0.000003 alpha[1] 0.050010 beta[1] 0.930000 Name: params, dtype: float64

2. GARCH模型预测

前面ARCH模型,我们用来预测了收益率,然而直接预测收益率准确度并不是很高,因此很多时候我们主要用来预测波动率.

In [22]:

resid=res_GARCH.resid[-14:] #取出过去14天的残差at

params=np.array(res_GARCH.params[1:15]) #取出均值方程所有系数

w_params=params[::-1] #倒转系数方向

w_params.dot(resid[-14:])

for i in range(30):

resid_new=test_GARCH.iloc[i]-(res_GARCH.params[0]+w_params.dot(resid[-14:]))

resid=np.append(resid,resid_new)

resid_final=resid[-30:]

resid_final_square=resid_final**2

resid_final_squareOut[22]:

array([1.31265182e-04, 4.24223468e-04, 2.34277150e-05, 8.61572516e-05,

7.61609044e-05, 9.93121008e-05, 6.07929980e-05, 9.97465719e-08,

3.17377608e-05, 1.50034013e-04, 7.63315088e-06, 1.93504633e-05,

1.31637564e-04, 1.60983709e-05, 6.62189736e-04, 2.51275329e-05,

1.20477057e-05, 3.81599502e-05, 3.29924979e-06, 6.78092403e-05,

8.81824346e-05, 3.51298854e-04, 1.00565226e-06, 6.70353037e-05,

2.03613211e-04, 6.43136485e-05, 1.87956839e-04, 1.15415026e-05,

4.33123654e-05, 1.57135491e-04])

In [54]:

volatility=res_GARCH.conditional_volatility[-1:]

for i in range(30):

new_volatility=0.000003+0.05001*resid_final_square[i]+0.93*volatility[-1]

volatility=np.append(volatility,new_volatility)

pre_volatility=volatility[-30:]

pre_volatilityOut[54]:

array([0.01227059, 0.01143586, 0.01063952, 0.00990207, 0.00921573,

0.0085786 , 0.00798413, 0.00742825, 0.00691286, 0.00643946,

0.00599208, 0.0055766 , 0.00519582, 0.00483592, 0.00453352,

0.00422043, 0.00392861, 0.00365851, 0.00340558, 0.00317358,

0.00295884, 0.00277229, 0.00258128, 0.00240694, 0.00225164,

0.00210024, 0.00196562, 0.00183161, 0.00170856, 0.00159982])

In [55]:

test_GARCHOut[55]:

2018-12-13 0.015481 2018-12-14 -0.016704 2018-12-17 -0.001489 2018-12-18 -0.010366 2018-12-19 -0.011923 2018-12-20 -0.007670 2018-12-21 -0.012395 2018-12-24 0.002906 2018-12-25 -0.006885 2018-12-26 -0.005054 2018-12-27 -0.003840 2018-12-28 0.006737 2019-01-02 -0.013658 2019-01-03 -0.001580 2019-01-04 0.023958 2019-01-07 0.006070 2019-01-08 -0.002161 2019-01-09 0.010097 2019-01-10 -0.001881 2019-01-11 0.007190 2019-01-14 -0.008722 2019-01-15 0.019625 2019-01-16 0.000211 2019-01-17 -0.005509 2019-01-18 0.018242 2019-01-21 0.005512 2019-01-22 -0.013284 2019-01-23 -0.000720 2019-01-24 0.005644 2019-01-25 0.008132 Name: return, dtype: float64

In [93]:

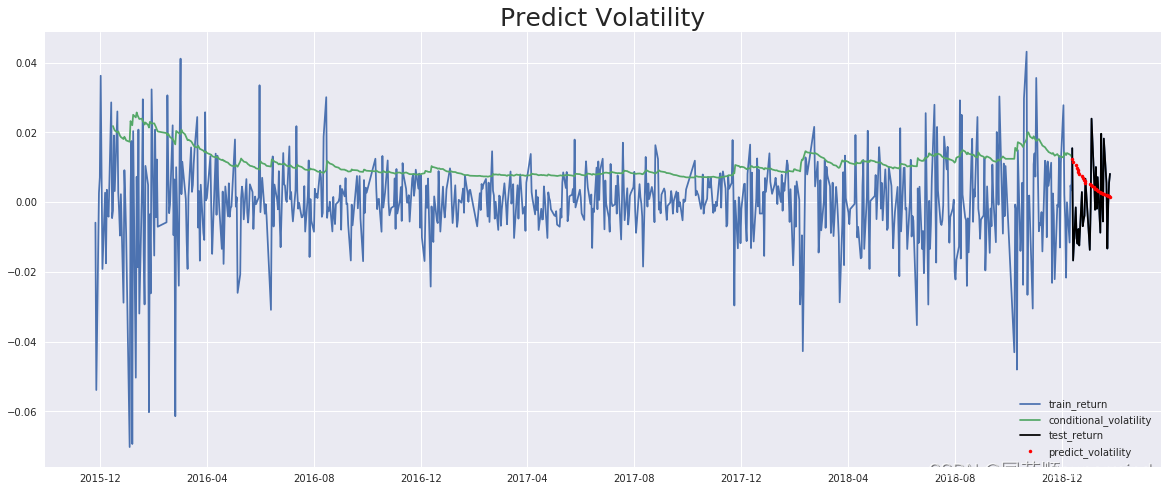

HS300_close.index=pd.to_datetime(HS300_close.index)

res_GARCH.conditional_volatility.index=pd.to_datetime(res_GARCH.conditional_volatility.index)

plt.figure(figsize=(20,8))

plt.plot(HS300_close['return'],label='train_return')

plt.plot(res_GARCH.conditional_volatility,label='conditional_volatility')

x=test_GARCH.index

plt.plot(test_GARCH,'black',label='test_return')

plt.plot(x,pre_volatility,'.r',label='predict_volatility')

plt.title('Predict Volatility',size=25)

plt.legend()Out[93]:

<matplotlib.legend.Legend at 0x7fc9cd798358>

In [ ]:

查看以上策略详细请 到 supermind量化交易官网查看:金融时间序列2--GARCH模型附源代码

7340

7340

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言