文章目录

梯度提升综述

梯度提升树的同义叫法:

- GBDT,Gradient Boosting Decision Tree,梯度提升决策树

- GBRT,Gradient Boosting Regression Tree,梯度回归树

- MART,Multiple Additive Regression Tree,多重累加回归树

GBDT是一种迭代的决策树算法,由多棵回归决策树组成,将所有决策树的输出累加作为最终输出.即

f

m

(

x

)

=

f

m

−

1

(

x

)

+

T

(

x

;

Θ

m

)

f_m(\bm x)=f_{m-1}(\bm x)+T(\bm x; \Theta_m)

fm(x)=fm−1(x)+T(x;Θm)

对于回归问题,若采用平方误差损失,则

L

(

y

,

f

m

−

1

(

x

i

)

+

T

(

x

i

;

Θ

m

)

)

=

[

y

−

f

m

−

1

(

x

)

−

T

(

x

;

Θ

m

)

]

2

=

[

r

−

T

(

x

;

Θ

m

)

]

2

L(y, f_{m-1}(\bm x_i)+T(\bm x_i;\Theta_m)) =[y-f_{m-1}(\bm x)-T(\bm x; \Theta_m)]^2 = [r-T(\bm x; \Theta_m)]^2

L(y,fm−1(xi)+T(xi;Θm))=[y−fm−1(x)−T(x;Θm)]2=[r−T(x;Θm)]2

其中

r

=

y

−

f

m

−

1

(

x

)

r=y-f_{m-1}(\bm x)

r=y−fm−1(x)是当前模型在训练集上的残差(实际值-预测值),每轮基模型的学习实际是在拟合当前模型的残差。

GBDT算法使用 负梯度近似残差,基模型的学习问题转变为拟合当前总体损失负梯度,使得各损失函数可用。Sklearn的GBDT实现,回归问题可选用MSE、MAE、Huber等损失,分类问题可选用Deviance(二分类对应于logistic、多分类对应于softmax)、Exponential损失。

GBDT优缺点:

- 采用决策树作为基模型,不需要特征标准化,数值缩放不影响分裂点,而且树形模型不通过梯度下降求解;

- 模型解释力强;

- 适用于不同的损失函数;

- 计算密集型,不能并行计算;

- 无法处理高纬稀疏特征的数据,如词袋特征的文本数据;

GBDT for Regression and Binary Classification

算法实现步骤:

-

初始化,将使损失函数极小的常数值作为初始值(MSE损失初值为均值):

H 0 ( x ) = arg min c E D [ L ( y , c ) ] = arg min c ∑ i w i L ( y i , c ) H_0(\boldsymbol x)=\arg\min_{c}\Bbb E_{\mathcal D}[L(y, c)]=\arg\min_c\sum_iw_iL(y_i,c) H0(x)=argcminED[L(y,c)]=argcmini∑wiL(yi,c) -

t t t,从1至T遍历:

-

将当前总体损失函数的负梯度作为本轮基模型拟合值:

g t = − [ ∂ L ( y , H ( x ) ) ∂ H ( x ) ] H ( x ) = H t − 1 ( x ) g_t=-\left[\dfrac{\partial L(y,H(\boldsymbol x))}{\partial H(\boldsymbol x)}\right]_{H(\boldsymbol x)=H_{t-1}(\boldsymbol x)} gt=−[∂H(x)∂L(y,H(x))]H(x)=Ht−1(x)回归任务一般使用MSE损失,分类任务一般使用Deviance损失(二分类和多分类对应于logistic和softmax).

-

使用CART决策树拟合 g t g_t gt,分类/回归任务均可使用MSE损失,对应结点输出均值:

h t ( x ) = arg min h E D [ ( g t − h ( x ) ) 2 ] = ∑ j = 1 J y ‾ j I ( x ∈ R j ) h_t(\boldsymbol x)=\arg\min_h\Bbb E_{\mathcal D}[(g_t-h(\boldsymbol x))^2] =\sum_{j=1}^J\overline y_j\Bbb I(\boldsymbol x\in R_j) ht(x)=arghminED[(gt−h(x))2]=j=1∑JyjI(x∈Rj) -

搜索最优步长 α t \alpha_t αt(sklearn使用固定值learning_rate),组合基模型

H t ( x ) = H t − 1 ( x ) + α t h t ( x ) , α t = arg min α E D [ L ( y , H t − 1 ( x ) + α h t ( x ) ) ] , H_t(\boldsymbol x)=H_{t-1}(\boldsymbol x)+\alpha_th_t(\boldsymbol x),\quad\alpha_t=\arg\min_{\alpha}\Bbb E_{\mathcal D}[L(y,H_{t-1}(\boldsymbol x)+\alpha h_t(\boldsymbol x))], Ht(x)=Ht−1(x)+αtht(x),αt=argαminED[L(y,Ht−1(x)+αht(x))],

-

-

迭代结束,最终模型为:

H ( x ) = H 0 ( x ) + ∑ t = 1 T α t h t ( x ) H(\boldsymbol x)=H_0(\boldsymbol x)+\sum_{t=1}^T\alpha_th_t(\boldsymbol x) H(x)=H0(x)+t=1∑Tαtht(x)

GBDT for K-class Classification

算法实现步骤:

-

初始化,各目标函数值初值为0, f k 0 ( x ) = 0 f_{k0}(\boldsymbol x)=0 fk0(x)=0;

-

t t t,从1至T遍历:

-

k k k,从1至K遍历:

-

将当前类别总体损失的负梯度作为本轮拟合值,若使用Deviance损失,则:

g t k = y k − exp ( f t − 1 , k ( x ) ) ∑ l = 1 K exp ( f t − 1 , l ( x ) ) g_{tk}=y_k-\frac{\exp(f_{t-1,k}(\boldsymbol x))}{\sum_{l=1}^K\exp(f_{t-1,l}(\boldsymbol x))} gtk=yk−∑l=1Kexp(ft−1,l(x))exp(ft−1,k(x)) -

拟合CART回归树:

h t k ( x ) = arg min h E D [ ( g t k − h t k ( x ) ) 2 ] h_{tk}(\boldsymbol x)=\arg\min_h\Bbb E_{\mathcal D}[(g_{tk}-h_{tk}(\boldsymbol x))^2] htk(x)=arghminED[(gtk−htk(x))2] -

根据最优步长 α t k \alpha_{tk} αtk组合基模型:

f t k ( x ) = f t − 1 , k ( x ) + α t k h t k ( x ) f_{tk}(\boldsymbol x)=f_{t-1,k}(\boldsymbol x)+\alpha_{tk}h_{tk}(\boldsymbol x) ftk(x)=ft−1,k(x)+αtkhtk(x)

-

-

-

迭代结束得K个模型,第k个模型:

f k ( x ) = ∑ t = 1 T α t k h t k ( x ) f_k(\boldsymbol x)=\sum_{t=1}^T\alpha_{tk}h_{tk}(\boldsymbol x) fk(x)=t=1∑Tαtkhtk(x)

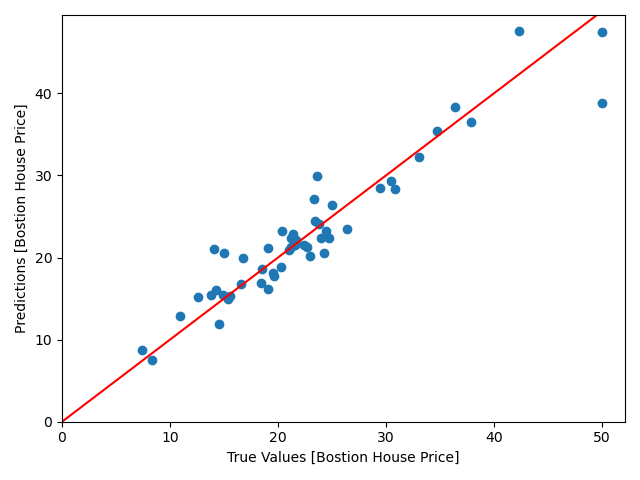

实例1:GBDT预测波士顿房价

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.datasets import load_boston

from sklearn.model_selection import train_test_split

import matplotlib.pyplot as plt

dataset = load_boston()

features = dataset.feature_names

X_train, X_test, y_train, y_test = train_test_split(

dataset.data, dataset.target, train_size=0.9, test_size=0.1, random_state=188)

gbr = GradientBoostingRegressor(

loss='ls',

learning_rate=0.1,

n_estimators=500,

max_depth=4,

min_samples_split=2,

verbose=1)

gbr.fit(X_train, y_train)

plt.scatter(y_test, gbr.predict(X_test))

plt.xlabel('True Values [Bostion House Price]')

plt.ylabel('Predictions [Bostion House Price]')

# plt.axis('equal')

# plt.axis('square')

plt.xlim([0, plt.xlim()[1]])

plt.ylim([0, plt.ylim()[1]])

plt.plot([-100, 100], [-100, 100], 'r')

plt.show()

模型预测效果图如下,离直线越近的点,拟合越好:

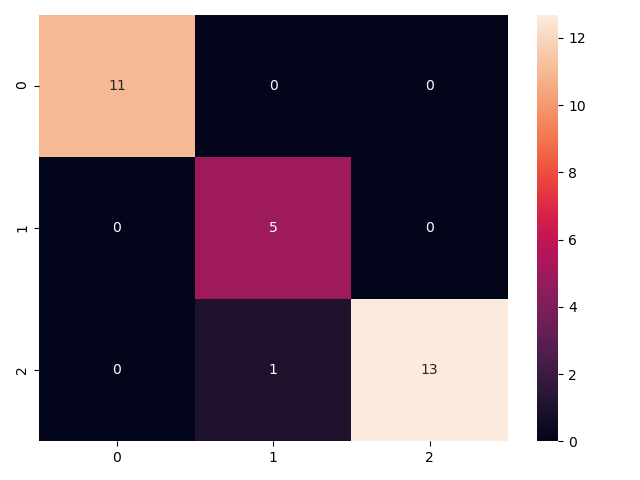

实例2:GBDT预测鸢尾花类别

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.datasets import load_iris

from sklearn.ensemble import GradientBoostingClassifier

from sklearn.metrics import classification_report, confusion_matrix

from sklearn.model_selection import train_test_split

dataset = load_iris()

features = dataset.feature_names

X_train, X_test, y_train, y_test = train_test_split(

dataset.data, dataset.target, train_size=0.8, test_size=0.2, random_state=188)

gbc = GradientBoostingClassifier(

loss='deviance',

learning_rate=0.1,

n_estimators=200,

max_depth=4,

min_samples_split=2,

verbose=1)

gbc.fit(X_train, y_train)

y_pred = gbc.predict(X_test)

report = classification_report(y_test, gbc.predict(X_test), output_dict=False)

print(report)

sns.heatmap(confusion_matrix(y_test, y_pred), annot=True, robust=True)

plt.show()

预测分类报告

precision recall f1-score support

0 1.00 1.00 1.00 11

1 0.83 1.00 0.91 5

2 1.00 0.93 0.96 14

accuracy 0.97 30

macro avg 0.94 0.98 0.96 30

weighted avg 0.97 0.97 0.97 30

预测分类混淆矩阵

1026

1026

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言