FTRL(Follow The Regularized Leader)学习总结

摘要:

1.算法概述

2.算法要点与推导

3.算法特性及优缺点

4.注意事项

5.实现和具体例子

6.适用场合

内容:

1.算法概述

FTRL是一种适用于处理超大规模数据的,含大量稀疏特征的在线学习的常见优化算法,方便实用,而且效果很好,常用于更新在线的CTR预估模型;

FTRL算法兼顾了FOBOS和RDA两种算法的优势,既能同FOBOS保证比较高的精度,又能在损失一定精度的情况下产生更好的稀疏性。

FTRL在处理带非光滑正则项(如L1正则)的凸优化问题上表现非常出色,不仅可以通过L1正则控制模型的稀疏度,而且收敛速度快;

参考:[笔记]FTRL与Online Optimization

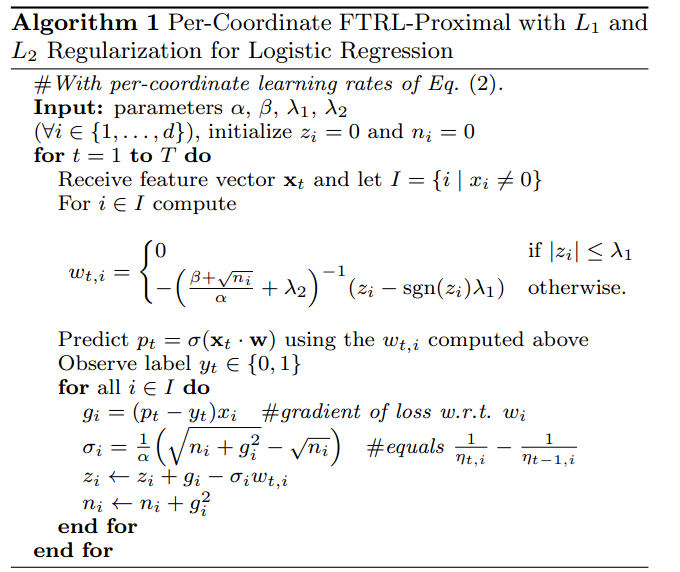

2.算法要点与推导

3.算法特性及优缺点

FTRL-Proximal工程实现上的tricks:

1.saving memory

方案1)Poisson Inclusion:对某一维度特征所来的训练样本,以p的概率接受并更新模型。

方案2)Bloom Filter Inclusion:用bloom filter从概率上做某一特征出现k次才更新。

2.浮点数重新编码

1)特征权重不需要用32bit或64bit的浮点数存储,存储浪费空间

2)16bit encoding,但是要注意处理rounding技术对regret带来的影响(注:python可以尝试用numpy.float16格式)

3.训练若干相似model

1)对同一份训练数据序列,同时训练多个相似的model

2)这些model有各自独享的一些feature,也有一些共享的feature

3)出发点:有的特征维度可以是各个模型独享的,而有的各个模型共享的特征,可以用同样的数据训练。

4.Single Value Structure

1)多个model公用一个feature存储(例如放到cbase或redis中),各个model都更新这个共有的feature结构

2)对于某一个model,对于他所训练的特征向量的某一维,直接计算一个迭代结果并与旧值做一个平均

5.使用正负样本的数目来计算梯度的和(所有的model具有同样的N和P)

6.subsampling Training Data

1)在实际中,CTR远小于50%,所以正样本更加有价值。通过对训练数据集进行subsampling,可以大大减小训练数据集的大小

2)正样本全部采(至少有一个广告被点击的query数据),负样本使用一个比例r采样(完全没有广告被点击的query数据)。但是直接在这种采样上进行训练,会导致比较大的biased prediction

3)解决办法:训练的时候,对样本再乘一个权重。权重直接乘到loss上面,从而梯度也会乘以这个权重。

算法特点:

- 在线学习,实时性高;

- 可以处理大规模稀疏数据;

- 有大规模模型参数训练能力;

- 根据不同的特征特征学习率。

实现和具体例子:

FTRL处理“Springleaf Marketing Response”数据

适用场合:点击率模型

代码:

from datetime import datetime

from csv import DictReader

from math import exp, log, sqrt

from random import random

import pickle

# TL; DR, the main training process starts on line: 250,

# you may want to start reading the code from there

##############################################################################

# parameters #################################################################

##############################################################################

# A, paths

train='../input/train.csv'

test='../input/test.csv'#'vali_100.tsv'

submission = 'ftrl1sub.csv' # path of to be outputted submission file

# B, model

alpha = .005 # learning rate

beta = 1. # smoothing parameter for adaptive learning rate

L1 = 0. # L1 regularization, larger value means more regularized

L2 = 1. # L2 regularization, larger value means more regularized

# C, feature/hash trick

D = 2 ** 24 # number of weights to use

interaction = False # whether to enable poly2 feature interactions

# D, training/validation

epoch = 1 # learn training data for N passes

holdafter = 9 # data after date N (exclusive) are used as validation

holdout = None # use every N training instance for holdout validation

##############################################################################

# class, function, generator definitions #####################################

##############################################################################

class ftrl_proximal(object):

''' Our main algorithm: Follow the regularized leader - proximal

In short,

this is an adaptive-learning-rate sparse logistic-regression with

efficient L1-L2-regularization

Reference:

http://www.eecs.tufts.edu/~dsculley/papers/ad-click-prediction.pdf

'''

def __init__(self, alpha, beta, L1, L2, D, interaction):

# parameters

self.alpha = alpha

self.beta = beta

self.L1 = L1

self.L2 = L2

# feature related parameters

self.D = D

self.interaction = interaction

# model

# n: squared sum of past gradients

# z: weights

# w: lazy weights

self.n = [0.] * D

self.z = [random() for k in range(D)]#[0.] * D

self.w = {}

def _indices(self, x):

''' A helper generator that yields the indices in x

The purpose of this generator is to make the following

code a bit cleaner when doing feature interaction.

'''

# first yield index of the bias term

yield 0

# then yield the normal indices

for index in x:

yield index

# now yield interactions (if applicable)

if self.interaction:

D = self.D

L = len(x)

x = sorted(x)

for i in xrange(L):

for j in xrange(i+1, L):

# one-hot encode interactions with hash trick

yield abs(hash(str(x[i]) + '_' + str(x[j]))) % D

def predict(self, x):

''' Get probability estimation on x

INPUT:

x: features

OUTPUT:

probability of p(y = 1 | x; w)

'''

# parameters

alpha = self.alpha

beta = self.beta

L1 = self.L1

L2 = self.L2

# model

n = self.n

z = self.z

w = {}

# wTx is the inner product of w and x

wTx = 0.

for i in self._indices(x):

sign = -1. if z[i] < 0 else 1. # get sign of z[i]

# build w on the fly using z and n, hence the name - lazy weights

# we are doing this at prediction instead of update time is because

# this allows us for not storing the complete w

if sign * z[i] <= L1:

# w[i] vanishes due to L1 regularization

w[i] = 0.

else:

# apply prediction time L1, L2 regularization to z and get w

w[i] = (sign * L1 - z[i]) / ((beta + sqrt(n[i])) / alpha + L2)

wTx += w[i]

# cache the current w for update stage

self.w = w

# bounded sigmoid function, this is the probability estimation

return 1. / (1. + exp(-max(min(wTx, 35.), -35.)))

def update(self, x, p, y):

''' Update model using x, p, y

INPUT:

x: feature, a list of indices

p: click probability prediction of our model

y: answer

MODIFIES:

self.n: increase by squared gradient

self.z: weights

'''

# parameter

alpha = self.alpha

# model

n = self.n

z = self.z

w = self.w

# gradient under logloss

g = p - y

# update z and n

for i in self._indices(x):

sigma = (sqrt(n[i] + g * g) - sqrt(n[i])) / alpha

z[i] += g - sigma * w[i]

n[i] += g * g

def logloss(p, y):

''' FUNCTION: Bounded logloss

INPUT:

p: our prediction

y: real answer

OUTPUT:

logarithmic loss of p given y

'''

p = max(min(p, 1. - 10e-15), 10e-15)

return -log(p) if y == 1. else -log(1. - p)

def data(path, D):

''' GENERATOR: Apply hash-trick to the original csv row

and for simplicity, we one-hot-encode everything

INPUT:

path: path to training or testing file

D: the max index that we can hash to

YIELDS:

ID: id of the instance, mainly useless

x: a list of hashed and one-hot-encoded 'indices'

we only need the index since all values are either 0 or 1

y: y = 1 if we have a click, else we have y = 0

'''

for t, row in enumerate(DictReader(open(path), delimiter=',')):

# process id

#print row

try:

ID=row['ID']

del row['ID']

except:

pass

# process clicks

y = 0.

target='target'#'IsClick'

if target in row:

if row[target] == '1':

y = 1.

del row[target]

# extract date

# turn hour really into hour, it was originally YYMMDDHH

# build x

x = []

for key in row:

value = row[key]

# one-hot encode everything with hash trick

index = abs(hash(key + '_' + value)) % D

x.append(index)

yield ID, x, y

##############################################################################

# start training #############################################################

##############################################################################

start = datetime.now()

# initialize ourselves a learner

learner = ftrl_proximal(alpha, beta, L1, L2, D, interaction)

# start training

for e in range(epoch):

loss = 0.

count = 0

for t, x, y in data(train, D): # data is a generator

p = learner.predict(x)

loss += logloss(p, y)

learner.update(x, p, y)

count+=1

if count%1000==0:

#print count,loss/count

print('%s\tencountered: %d\tcurrent logloss: %f' % (

datetime.now(), count, loss/count))

if count>10000: # comment this out when you run it locally.

break

count=0

loss=0

#import pickle

#pickle.dump(learner,open('ftrl3.p','w'))

print ('write result')

##############################################################################

# start testing, and build Kaggle's submission file ##########################

##############################################################################

with open(submission, 'w') as outfile:

outfile.write('ID,target\n')

for ID, x, y in data(test, D):

count+=1

p = learner.predict(x)

loss += logloss(p, y)

outfile.write('%s,%s\n' % (ID, str(p)))

if count%1000==0:

#print count,loss/count

print('%s\tencountered: %d\tcurrent logloss: %f' % (

datetime.now(), count, loss/count))

433

433

被折叠的 条评论

为什么被折叠?

被折叠的 条评论

为什么被折叠?

到【灌水乐园】发言

到【灌水乐园】发言